In a survey of 560 executives from leading financial institutions across 17 markets entitled, “Retail Banking 2020: Evolution or Revolution,” PwC found that 90 percent of financial services executives agree on the priorities that are the foundation for success in 2020, yet only a fifth (20 percent) feel well-prepared to address these priorities despite the fact that nearly all (96 percent) believe that a fundamental transformation of the banking industry is inevitable.

“Growth remains elusive, costs are proving hard to contain, returns remain stubbornly low and regulation is impacting business models and economics”

— John Garvey, PwC

“Growth remains elusive, costs are proving hard to contain, returns remain stubbornly low and regulation is impacting business models and economics,” said John Garvey, U.S. banking and capital markets leader at PwC. “Simultaneously, the evolution of technology and heightened customer expectations combined with the emergence of disruptive competitors creates new pressure to deliver higher levels of service at a time when value and trust in the sector is at an all-time low. Surviving and succeeding in this environment may require a fundamental rethink in approach.”

Today’s Challenges

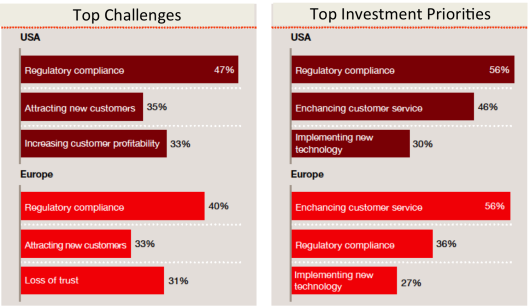

The impact of growing and changing regulations is the primary challenge for retail banks in the U.S. (47 percent) and Europe (40 percent), where banks are trying to stop seeing regulations as a burden and hoping to weave compliance into the fabric of their operations.

In the U.S., attracting new customers (35 percent) and increasing profitability (33 percent) ranked second and third respectively, aligning with the hierarchy of investment priorities (56 percent regulatory compliance, 46 percent enhancing customer service and 30 percent implementing new technology).

Nearly all respondents (97 percent) view innovation as a critical driver of growth – with companies who consider themselves innovative predicting 62 percent growth over the next five years, nearly double the market average of 35 percent and triple the 21 percent for the least innovative companies.

Despite understanding the importance, only 10% of CEOs view their organizations as innovation leaders. Further, 64% of CEOs agree that neither innovation nor operational effectiveness are dominant – and are looking to succeed at both.

PwC believes executives recognize they need to do things differently. According to the study, over 50% are planning to enhance their internal capabilities to foster innovation, and to create innovation management teams across business units. There is also a recognition that partnerships and third-party relationships may be the best way for banks to reap the benefits of innovation.

In the U.S., the primary areas mentioned for innovation were products (43 percent), customer interfaces/channels (60 percent), core platforms (50 percent) and customer need identifications (40 percent).

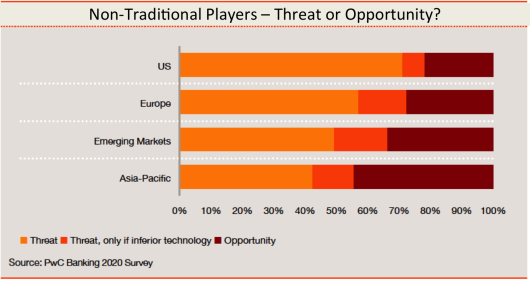

Finally, nearly three quarters (71 percent) of U.S. retail banking executives consider non-traditional competitors a threat, significantly higher than executives in Asia (42 percent), where more view them as an opportunity for partnering.

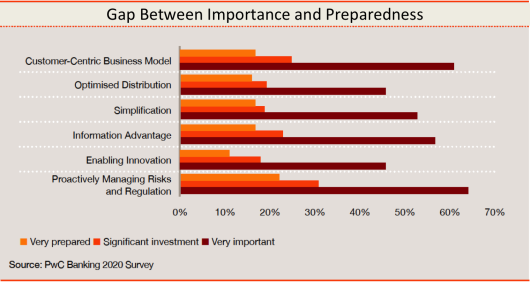

Gap Between Priorities and Preparedness

According to the research, 90 percent of the executives agree that the six key priorities for success in 2020 were:

- Developing a customer centric business model

- Optimizing distribution by evolving multichannel capabilities and reshaping the traditional branch model

- Simplifying business and operating models

- Harnessing data to deliver customer, risk management and financial advantages

- Fostering agility and innovation

- Proactively managing risk, regulation and capital

Banking executives agree that the priorities above are very important, with each of them scoring between 4.3 and 4.5 (out of 5) in the PwC survey. However, there was a striking gap between those ranking these priorities as ‘Very important’ (46%–64%) and those stating that they saw themselves as ‘Very prepared’ (11%–17%) and/or that they were making a ‘Significant investment’(18%–25%) in these areas. Technological, organizational, talent and cost constraints were viewed as the greatest obstacles to success.

According to PwC, each bank needs to develop a clear strategy to deal with the industry’s transforming landscape. They need to decide whether to lead, to follow fast, or to manage defensively, putting off change. They need to create agility and optionality, to adapt to rapid change and future uncertainty. Yet, whatever the chosen strategy, success will come from successfully executing the right balance across the six priorities identified.

“Banks universally agree that they are hindered from addressing top priorities such as innovation by financial, talent, technology and organizational constraints, said Dave Hoffman, U.S. financial services management consulting leader at PwC. “Banks should take aggressive action to overcome these constraints to enable innovation and transformation, while preserving their ability to capitalize on market opportunities and address unexpected challenges.”

Whether this is this a revolution, evolution or both is yet to be seen. Many players globally are innovating and experimenting with new products, delivery channels and analytics. The industry has historically changed very slowly – yet the pace of change is increasing rapidly.

According to PwC, the challenges in the future are clear, and but each institution’s response will be unique based on their current capabilities, markets, capital strength, aspirations, etc. The key is to leverage knowledge from the industry and from outside the industry to succeed.

The biggest challenge is that banks that fail to shift gears risk being left behind.