Handling bank and credit union marketing in the wake of COVID-19 will be the greatest challenge financial marketers face in their careers.

America will be looking to institutions like its banks and credit unions as buoys of stability in the days ahead. But they will also want messages that are on point and financial marketers must tread carefully.

“Tune your channels for customer listening for constant, real-time monitoring of shifts in customer sentiment and expectations,” Gartner states in a report. “Maintain proactive and reactive communication guidance to arm employees and to keep your customers informed during a period of greater need and anxiety.”

Tone will be important, but recognition of essentials will be the top concern. A special report by Aite lists key messages to get out to the public:

- Promote capabilities that can be provided digitally, such as remote capture, P2P transfers, and video chat.

- Frequent updates should be posted concerning branch closures and other service changes.

- Increase, and communicate, limits on remote capture, ATM transactions, card-based transactions, and contactless transactions.

- Accelerate broadened availability of contactless payments — which may be a longer-term project given that merchant terminals must be compatible.

- Consider waiving fees and delaying payment due dates.

- Promote personal financial management tools. Many Americans are now living in a state of flux, but they need a touchstone from which to figure out where they may be headed — someday all those Amazon and Instacart charges are going to have to be paid.

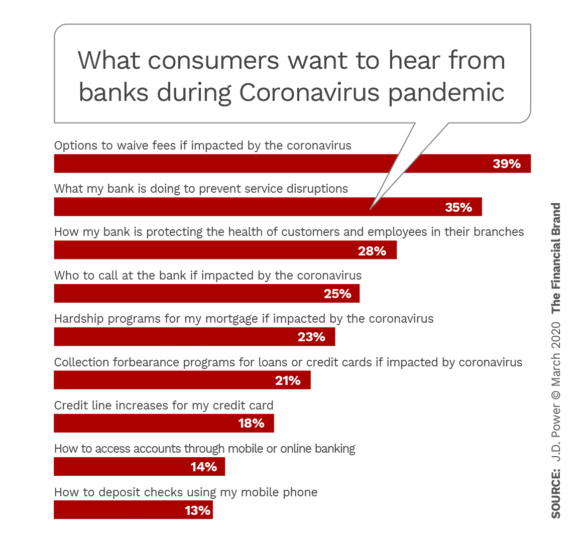

Research by J.D. Power indicates that what consumers want from banks and credit unions right now are easily found answers to very practical question, not generalities.

A good example of an approach that checks off many of the concerns in the chart above is USAA’s coronavirus update page. While it opens with a short statement by the CEO, the page quickly gets into practical matters.

Dismal Employment Picture Calls for Extra Care

Every message promoting stability will help people stay centered in an emotional time. This is a time to think out of the box, but not a time to get over-clever.

Case in point: One financial comparison shopping site referred to “panic saving” — akin to panic buying of toilet paper — being a good thing. But panic-anything should be avoided, even if it brings in deposits.

The overnight shift of many American jobs to telecommuting has caused some inconvenience and adjustment for many, but it is nothing compared to the situation being faced by many other Americans who have been furloughed or laid off. Challenger, Gray & Christmas has been tracking job cut announcements and reported in later March 2020 that more than 9,000 companies had announced cuts, layoffs, furloughs and more. While over nine out of ten of the companies making the announcements are in the entertainment and leisure field, the ripple effect will go to infinity in an interdependent society.

“The U.S. government’s partial shutdown in late 2018 and early 2019 brought to light the precarious nature of many households across income levels,” states the Aite study. “Many financial institutions responded to federal workers’ plights by waiving interest and fees, or even postponing loan payment due dates. But COVID-19 will directly and indirectly affect a population several orders of magnitude greater than the 800,000 federal workers with paycheck delays.”

Social media patterns are among the items financial marketers must watch. Ipsos has been monitoring how coronavirus disruptions have expanded across social media. Thus far much of the consumer chatter has concerned empty shelves in stores and the closure of favorite bars and restaurants. Analyzing emotions expressed on Twitter and Facebook, Ipsos reports that bar and restaurant closures are driving more sadness and anger than fear, but that empty shelves in food stores is generating a sense of alarm. Clumsy marketing could cause troubles for banks and credit unions.

Banking institutions must watch for what consumers begin saying about them, says Ipsos. The firm says social media trends indicate fear plus distrust of the government — not great for an industry that relies on federal deposit insurance for part of its appeal to safety concerns. FDIC has already been working to counteract scammers who have tried to sway consumers with fake news.

Gartner’s report makes the point that the coronavirus pandemic has arrived as part of a perfect storm. Over the last decade, the report states, consumers have grown uncomfortable with the unknown in general and have been “pulling into a a kind of defensive crouch.” This has been accompanied by “a general collapse of consumer trust in government, their fellow citizens and big brands.” And now, social isolation for many brings lots of time to consider their fear of coronavirus.

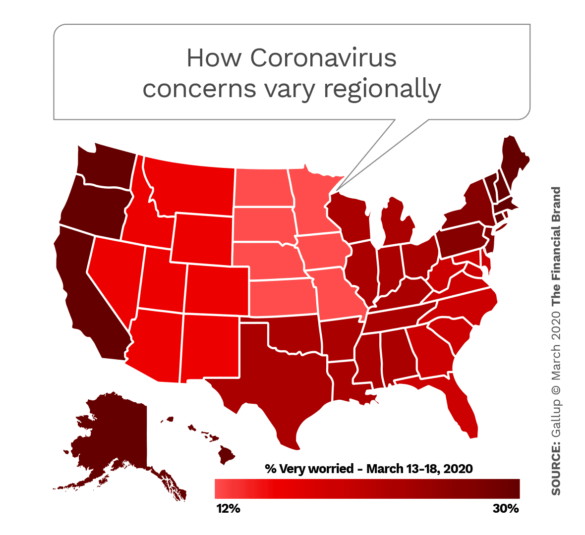

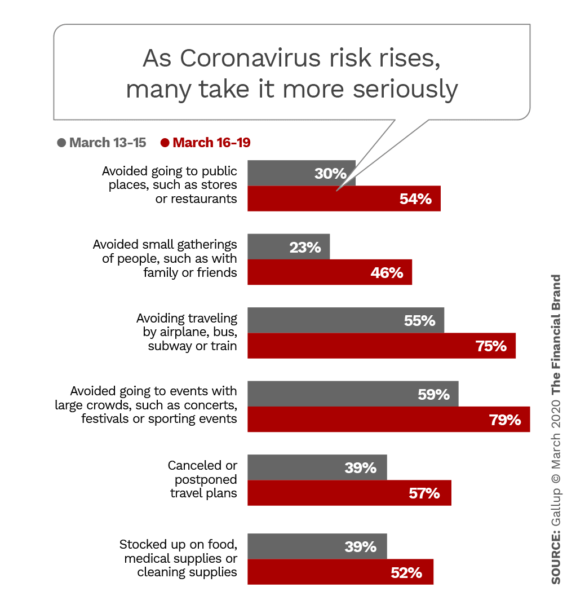

The pace of change in the coronavirus outbreak has been such that the lighter-shaded states in the Gallup map above may darken before long.

Aite suggests this is a time when financial institutions should extend a helping hand even if it will cost them in the short-term. For example, with folks hunkering down, there will be more “card not present transactions.” (These include internet and telephone charges to cards.)

“Adjust card not present detection strategies in the same manner you would around the holidays,” the Aite report says. “Plan to see an overall bump in activity, and reduce your declines. You’ll absorb a bit more fraud, but you’ll also keep more good customers happy.”

Such a shift is not something to market per se, because it would be like putting a “kick me” sign on the institution. But the right content messaging could help.

“Customers will be heavily engaging in card not present transactions, so this could be an opportunity to educate and engage customers with capabilities such as two-way text and card controls that not only help them better manage their risk but also ensure better long-term security,” the report advises.

Don’t Be Tone Deaf: Listen to What People Are Saying

Gartner advises marketers to watch for shifts among those they serve. “They will experience a desire to feel secure and will have greater expectations of brands to offer care and protection at exactly the time when your company will be most challenged to meet those needs,” the report states.

Mere platitudes won’t impress people in that state of mind, Gartner warns. They want something more tangible.

“Carefully weigh safeguarding your short-term interests in the midst of an epidemic-propelled business slowdown versus the value to sustain and nurture longer-term customer relationships,” the report states. “Be mindful of where you will and will not be able to satisfy customer expectations in a period when their sensitivities are heightened.”

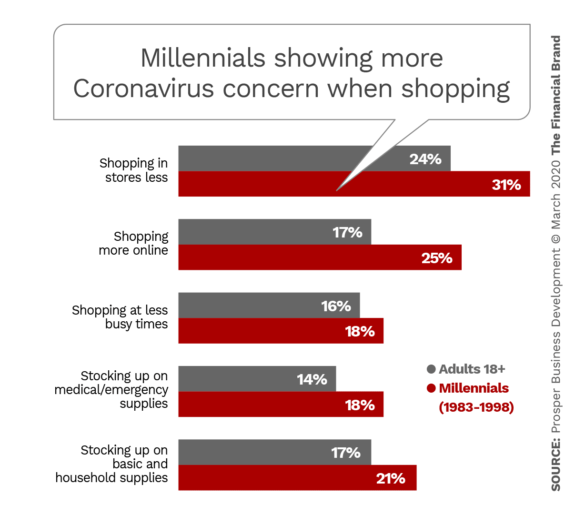

There are generational differences, such as the extra-cautious trend seen among Millennials in the chart below, based on research by Prosper Business Development. To the degree that a bank or credit union is still segmenting its marketing and to the degree it has been using social media influencers to reach younger consumers, it can bear this in mind.

Faith Adams, Senior Analyst at Forrester, suggests in a blog that this isn’t the time for surveys, even though people may seem like a captive audience at home. Pay closer attention to what consumers are saying in emails, calls and other direct communications, as well as on social media, she advises.

Read More:

- Raising Deposits Amid Coronavirus Rate-Slashing and Stock Volatility

- Banking Without Branches a Matter of Life and Death

- Work At Home Disruption Creates Once-In-A-Lifetime Opportunity

Beware of Quickly Shifting Attitudes to Avoid Flat Notes

Financial institutions will have to be careful what they choose to communicate, how they communicate it, and how quickly they can change their messaging if the need arises.

“Optics” will be very fluid depending on the news of the day for some time. Aite makes the point that already the “tone” involved in various banking channels and payment systems can be a two-edged sword.

Consider ATMs and making cash available on demand. Some consumers have been withdrawing extra currency to have it on hand, the report notes. On the other hand, “financial institutions should also consider the risk of ‘infected’ ATMs or cash, particularly if used currency is loaded into cartridges.” While some cities had banned requirements that consumers make only cashless purchases, prior to the arrival of coronavirus, since the outbreak some stores have specifically been requesting that consumers not use cash.

The debate over this has continued on social media, with some anti-cashless commenters complaining that cashless advocates are exploiting the health crisis.

Yet to not make cash readily available may not suit certain consumers either, where they are dealing with merchants, landlords or others who will not or cannot accept payment cards or mobile wallets. One New York City suburb apartment dweller complained that she had to search for an open ATM with cash in order to pay rent.

The Aite report suggests that coronavirus worries will lead many institutions to promote digital channels such as mobile wallets for using debit and credit cards without the risk of manual contact. However, before pushing digital solutions, institutions should be clear that what they are promoting is doable. We tried this and found the reality is that many retailers are still not able to accept payments from mobile wallets, and the wallet setup experience is not always flawless.

That’s another role for financial marketers today. People need guidance to take advantage of contactless commerce. Give it to them.