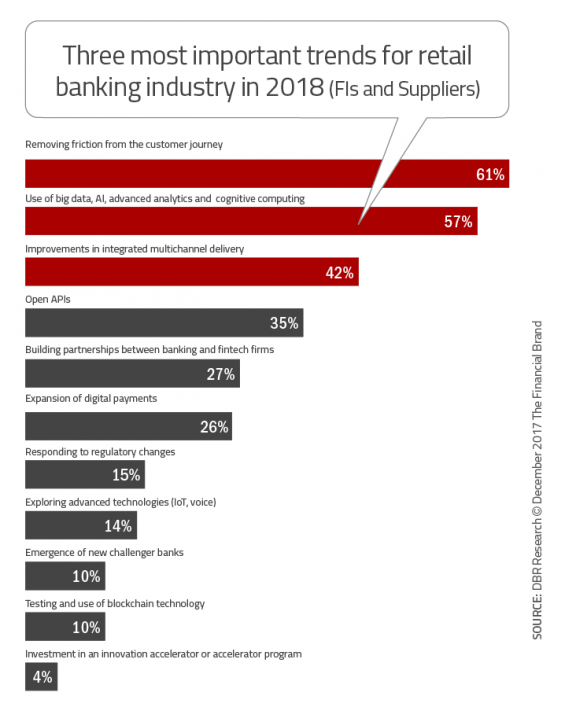

When we surveyed over 100 leaders in the global financial industry, we asked for their thoughts on the trends and predictions affecting retail banks and credit unions in the coming year. Ten major industry trends rose to the top, with three trends being paramount in the eyes of the research participants.

But getting a perspective on the future is only valuable if organizations know what action they need to take. From improving the customer journey, to building a seamless integration of channels and/or using data analytics to know more about each customer or member, the financial impact of any trend is determined by the specific action taken in the marketplace to prepare or react to industry trends.

Below are the top 10 trends identified in the Digital Banking Report entitled, 2018 Retail Banking Trends and Predictions, sponsored by Kony. The comprehensive 106-page report is available here.

1. Improve the Consumer Experience

An optimal consumer journey makes every step and touch point in the buying cycle streamlined, efficient, consistent and personalized from the consumer perspective. Financial institutions need to re-imagine their core journeys from front to back by addressing key customer pain points and identifying new opportunities to delight customers in differentiated ways. Digital channels and transforming the back office to a digital flow is at the core of improving the customer journey in the future.

Read More: Gap Between Legacy Banks & Fintech Firms Has Shrunk

Immediate Strategies:

- Create an account opening process that allows a customer or member to open an account digitally without needing to enter a branch.

- Build a real-time alert process that goes beyond post-event notifications to include recommendations for future actions.

- Redesign your mobile and online banking platforms, removing steps that create friction.

- Rethink back-office process flows and documentation from a ‘digital bank’ perspective.

2. Expand Use of Data and Analytics

Despite the vast amount of data available and the industry’s formidable resources, most banks and credit unions are still far from realizing big data’s full potential. This gap in capabilities is caused by competing priorities, the complexity of knowing what data to use and how to collect the insight as well as the lack of a coordinated vision. Going forward, the use of AI, machine learning and other advanced analytic tools will provide opportunities for greater personalization and channel optimization. Data and analytics is at the core of every trend expected in the year to come.

Immediate Strategies:

- Break down the barriers within your organization that perpetuate data silos. Only after silos are eliminated can advanced analytics be the most effective.

- Establish a data analytics function or partner with an outside organization to provide help in improving the actionability of your data.

- Replace timed marketing ‘programs’ with ongoing marketing ‘processes,’ leveraging real-time data to take advantage of immediate opportunities.

- Test the use of artificial intelligence (AI) and machine learning (ML) beyond risk and fraud analysis, including offer generation and bundling of services.

Read More: Why the ROI of AI Falls Short for Nearly Everyone

3. Support Multi-Channel Delivery

The use of advanced analytics provides an opportunity for an optichannel™ experience, where the best channel is based on the consumer’s needs and preferred channel. So, rather than offering all channels for a specific solution, big data will enable an organization to point the consumer to the channel that will provide the most personalized experience. As multichannel relates to a better experience, the consumer expects to be able to move from channel to channel without a ‘restart’ and does not expect to be ‘forced’ to use a physical channel to complete a process.

Read More: Most Financial Institutions Still Make Banking Too Difficult

Immediate Strategies:

- Allow customers and members to stop any process (such as new account opening or applications) and restart on another channel without retracing footsteps.

- Expand traditional marketing to include all digital channels including SEO, social media, influencer and content marketing, videos, SEM, retargeting, mobile banking app, etc.

- Implement a teaching platform within branches that assists visitors with the use of digital technology.

4. Embrace Open Banking

With the formal introduction of PSD2 in Europe and greater recognition of the power of open banking, the use of open APIs remains a top priority. The use of open APIs provides the opportunity for combinations of products and services beyond traditional banking. If executed well, traditional financial services organizations can be at the center of a consumer’s daily life. Otherwise, a traditional banking organization may be relegated to be simply a provider of services for other firms.

Immediate Strategies:

- Review existing data privacy mandates and potential changes, determining the risk/benefit appetite for new marketplace opportunities.

- Explore data-sharing possibility with fintech and non-financial services firms to be prepared for imminent changes.

- Build an API strategy for both third-party data access and potential service offerings outside traditional banking ecosystem.

Read More: Open Banking Provides Potential For Revenue Goldmine

5. Build Fintech Partnerships

Continuing a trend that emerged in 2016, legacy organizations will continue to leverage the advantages of scale, stability, trust, experience in navigating regulations and the access to significant capital as they look for viable fintech partners. Conversely, fintech firms will leverage their agility, innovation culture and technological expertise that legacy organizations seek, with the resultant partnerships benefiting the end consumer. With the expansion of data, analytics and open banking, the evidence of new banking + fintech partnerships will expand greatly.

Immediate Strategies:

- Foster a top-down culture of innovation, testing and understanding the digital consumer.

- Investigate partnerships and/or collaboration with fintech firms for products and processes not currently possible within the banking organization.

- Replace all or a portion of legacy systems, integrating new technologies while embracing an agile IT culture. This action step has been put on the back burner for years which is hurting many organizations.

- Consider having an online lender power the organization’s online loan application, to using an online lender’s credit model to better underwrite and service bank loan applications.

![]()

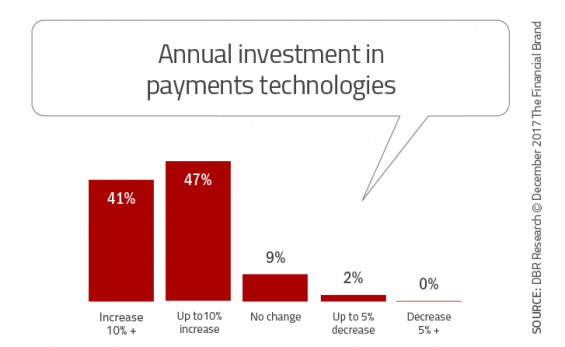

6. Upgrade Digital Payment Capabilities

The use of mobile payments continues to be less than expected, illustrating the challenges in changing consumer behavior when merchants and issuers can’t deliver a strong value proposition. While mobile payments at the POS level may continue to lag, P2P transactions will continue to skyrocket as new entrants like Zelle and current players like Venmo and Square continue to gain momentum.

Immediate Strategies:

- Build a payments onboarding and ongoing communications process for the sign-up and usage of digital payments products. The most effective channels for this expansion of relationship is email and SMS texts.

- Develop a mobile wallet and P2P payments strategy. P2P payment products are the new ‘must have’ service that digital consumers demand of their financial institution.

- Proactively address consumer concern around privacy and security. This includes both communications as well as new functionality such as biometric authentication.

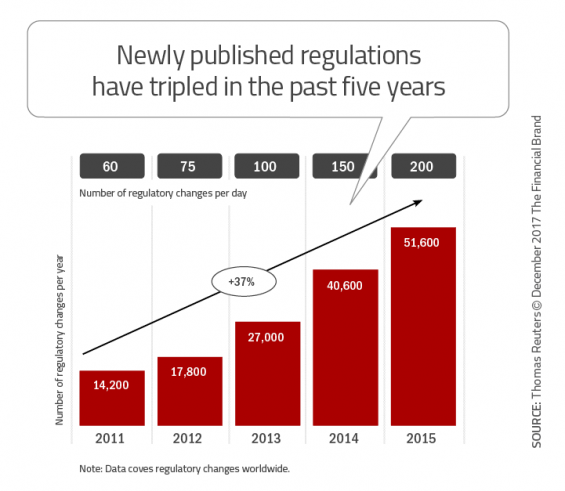

7. Manage Compliance and Regulations

The financial services regulatory environment continues to be highly uncertain and often has conflicting regulations. In addition to causing a huge increase in the costs of compliance, they have also impacted many organizations’ business models. In the near future, it is expected that governmental agencies will continue to greatly lag consumer demands, but that both traditional and fintech organizations will move forward with a ‘beg for forgiveness’, rather than ‘asking for permission’ mentality.

Immediate Strategies:

- Simplify internal and external processes and procedures. Use AI, digital technology, robotics, etc. to automate monotonous processes, freeing your team to focus on strategy and tasks that demand human intellect and judgment.

- Establish a program of internal training and guidance on compliance obligations, strategies and responses. Informing staff of all issues regarding compliance is the optimal first line of defense.

- Develop an updated and standardized know your customer (KYC) processes for customer onboarding. Embed this process in all bank systems, applying technology across the entire customer life cycle.

8. Explore Advanced Technologies

As quickly as past technologies have become the norm, a new wave of emerging technologies will combine digital technologies and the power of data to set new standards. These ‘essential eight’ technologies include:

- The Internet of Things (IoT)

- Artificial Intelligence (AI)

- Robotics

- 3-D Printing

- Augmented Reality

- Virtual Reality

- Drones

- Blockchain

Obviously, the prioritization and investment in each of these technologies will vary based on the industry, business model and strategic goals of each organization. For instance, while the marketplace as a whole does not foresee investing much in blockchain technology, the financial services industry ranks this as a higher priority.

Tremendous momentum also surrounds the potential of using voice-first digital assistants in the banking industry. This will be exciting to watch as more firms allow consumers to perform basic transactions on their Alexa, Siri, Google Home or Apple Pod device.

Immediate Strategies:

- Develop a rigorous approach to emerging technology that includes a formal framework of listening to those on the bleeding edge, learning the true impact of these technologies, sharing results from pilot projects, and quickly scaling by implementing them throughout the enterprise.

- Build an IoT plan starting with devices such as wearables and home devices that will impact consumers more and more over the next three to five years.

- Engage with outside organizations to implement a branded voice-first strategy. While the beginning point will most likely be the support of voice devices (Alexa, Siri, Google Home), expanded usage options need to be considered.

9. Compete With New Challengers

The term “challenger bank” is widely used to describe a banking organization, started from the ground up and built without relying on another banking firm for back office support. While very common in the UK, this breed of bank has not yet emerged in the US due to regulatory confusion. With the advent of PSD2 and open banking, we expect most of the challenger bank activity to be in Europe, with the impact of larger tech firms (Google, Amazon, Facebook, Apple, Tencent and Alibaba) becoming much more of a threat to traditional banking models.

Immediate Strategies:

- Consider a niche strategy (or strategies) that can leverage internal insights and scale that is not possible with most fintech organizations. Remember that the ‘customer experience’ is the differentiator that many challenger banks are competing on.

- Develop a buy/collaborate strategy that can help diffuse the challenger bank advantage. Many banking organizations are partnering with innovative players to combine competitive advantages.

- Downsize bricks and mortar footprint to allow for improved internal economies and to focus more resources on digital capabilities.

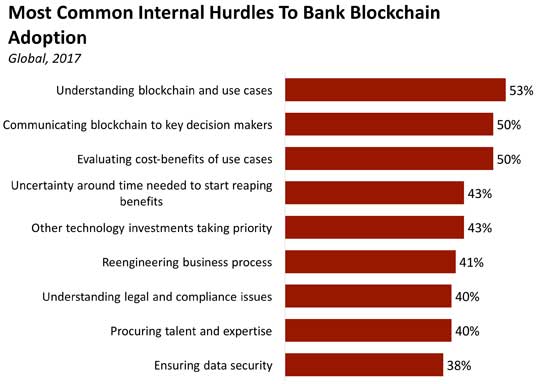

10. Test Blockchain Capabilities

While bitcoin and other cryptocurrencies took the headlines in 2017 and 2018, the greater impact over time may be the potential for blockchain use in banking. From providing the platform for movement of data and financial records, to the ability to become the foundation for identity management, banks of all sizes will be testing the capabilities of blockchain to save money, reduce risk and even generate revenues.

While early adopters are moving into blockchain production, most of the industry remains in a planning and experimental phase. Yet, the stakes of blockchain are too high for financial services firms to take a wait-and-see approach.

Immediate Strategies:

- Focus blockchain projects that will be materially beneficial to today’s business, such as helping with aging infrastructure issues that will provide cost savings through efficiency.

- Run blockchain trials internally, placing a priority on conducting them through engagements with outside organizations.

- Determine how blockchain fits into your 2020 roadmap and ensure that your projects have a clear trajectory that can take them from lab into the real world. Avoid the massive hype and false promises.

Preparing for the Future of Banking

Consumer needs and behaviors are pushing financial organizations to rethink their strategies. Consumers expect banks and credit unions to offer more than simple transaction processing, and instead become financial and even technology advisors.

Despite the lack of overwhelming trust in financial institutions, most consumers believe banks and credit unions are secure, and this is a strategic advantage that should not be minimized or taken for granted. While most consumers do not consider bank branches to be an irrelevant delivery channel, they expect them to be more efficient through digital technology that will improve the customer experience.

Consumers expect new innovations that will serve them in a more personalized and efficient manner, and also want a dynamic blend of digital and human service. Contactless payments, P2P and digital wallets are already a trend that will continue. Biometrics will also play a more important role in the future.