The pace of change in banking is already startling. Financial institutions are working overtime to leverage digital transformation for increased efficiencies, improved experiences and revised business models. But what do banking leaders from around the world believe will happen by 2025 … only three short years from now?

To answer questions around the speed of digital banking transformation, the Digital Banking Report asked over 400 financial institution executives to provide their projections as to what will happen in next three years. Our global research included not only banks and credit unions, but other financial services providers including fintech firms, third-party solution providers, as well as advisors and consultants to the banking industry.

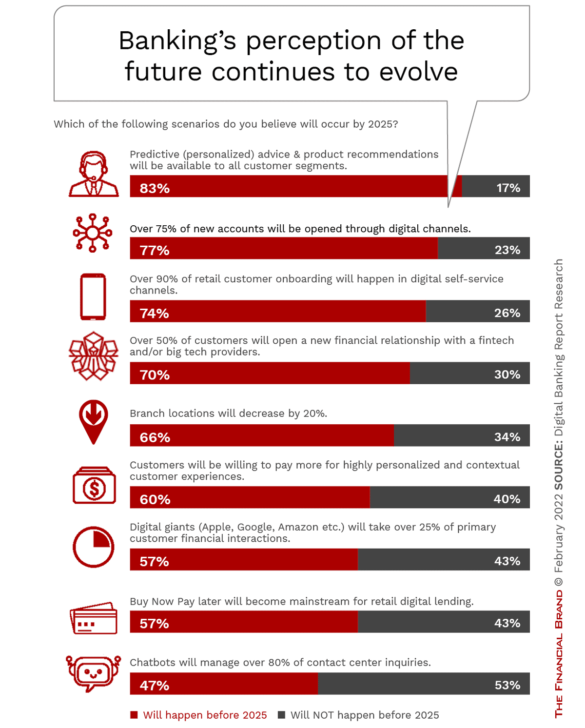

The research focused on nine perspectives — shown in the first chart, below — within four areas of banking:

- Customer experience

- The flight to digital

- Competition

- Innovation

As in any survey on the future of banking, all projections need to be taken within the context that change is happening faster than most financial services executives have ever seen. With that in mind, the projected speed of adoption of some developments (e.g. use of data to provide personalized experiences) can’t be ignored. The question becomes whether banks and credit unions will be prepared for the rapid changes they predict.

Read More: 14 Surprising Predictions on the Future of Banking

Banking is Changing Faster Than Ever

The most surprising takeaway from our research is that there is an assuredness of massive change in banking in the next few years. Based on the insights from financial executives globally, there is an overwhelming belief that personalization and predictive analytics will be close to a given part of the customer experience. The flight to digital was also thought to be close to a ‘given’, with digital account opening and onboarding being the next two most highly rated predictions.

With the exception of a belief that chatbots will manage over 80% of customer service inquiries, all of the projected changes in banking were thought to have better than a 50/50 chance of becoming a reality by 2025.

Digital Banking Transformation Highlights:

Most financial institutions may not be ready for the massive speed of change in customer experiences and digital transformation that their own executives predict.

Any of the predictions below, individually, will take a major investment and prioritization of resources to be prepared for. What used to be annual strategic initiatives need to be fast tracked to a much shorter timeframe that will most likely include the engagement of third-party solution providers to make happen.

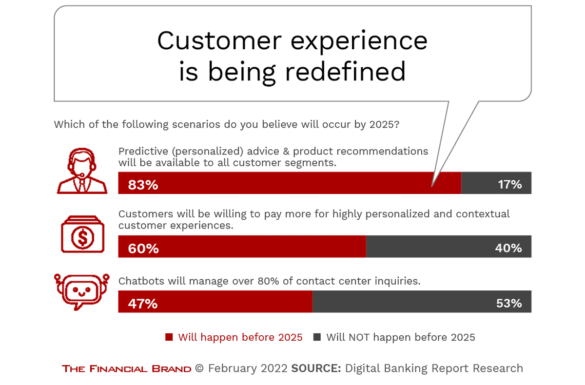

Customer Experience is Being Transformed

The concept of personalization in financial services is being redefined every day, becoming an important component of the overall customer journey. Much more than simply using a customer’s name in communication, data and advanced analytics enables financial institutions to deliver contextual communication, in real time, that will build engagement across all channels.

Brands that successfully meet the expectation of personalized experiences will be rewarded with more active relationships, increased loyalty, and greater revenue in the future. By 2025, 83% of financial institution executives believe personalized recommendations and advice will be commonplace across all customer segments. More importantly, 60% believe that consumers will be willing to pay more for a personalized experience.

Technology has made it possible for banks and credit unions to connect customer data across every possible touchpoint. Only connecting on mobile devices or a website is no longer enough; financial institutions need to create a presence across all touchpoints to deliver exceptional omnichannel experiences that will drive increased engagement.

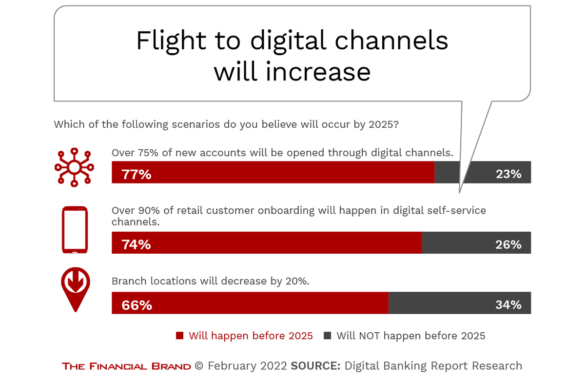

Flight to Digital Channels Escalates

According to J.D. Power, digital-only customers accounted for just 30% of the retail bank customer base prior to the pandemic. These customers also had the lowest level of satisfaction of any channel. In 2021, J.D. Power found that 41% of customers were digital-only, and satisfaction improved most among customers who had high levels of digital engagement with banking products and customer service.

When executives across the financial services industry spectrum were asked about the ‘next level’ of digital engagement, they were very optimistic about the potential of financial institutions to go beyond digital transactions, to include digital account opening and digital onboarding. In fact, 77% of those surveyed believed more than three quarters of accounts would be opened through digital channels by 2025. In addition, 74% of executives believed that over 90% of retail customer onboarding would be done digitally.

Digital Replaces Branches:

In the past six months, the percentage of financial services executives who believe more than one fifth of branches will close by 2025 increased by 74%.

The most radical impact of digital transformation may be the projected decrease in branches. Two-thirds of survey respondents believed the number of branches would decrease by 20% by 2025. Interestingly, in a similar survey done in August of 2021, only 38% of financial executives believed the reduction would be this high (an increase of 74% in six months).

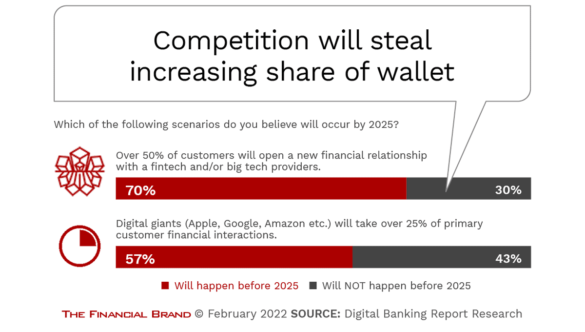

Competitive Landscape Continues to Evolve

While traditional banking organizations may not be seeing massive closures of checking or savings accounts, that doesn’t mean existing relationships are secure. In fact, 70% financial executives surveyed thought that more than half of consumers will open a new financial relationship with a non-traditional financial institution by 2025.

Our research also found that over 50% of financial services executives believed that digital giants (Amazon, Google, Apple, etc.) would take over 25% of primary financial relationships by 2025. This is aligned with research done in August of 2021, where almost three-quarters of executives surveyed thought that at least two fintech or big tech firms would be a top ten of financial institution provider (in terms of assets) by 2030.

‘Silent’ Attrition is a Problem:

70% of financial executives expect over 50% of customers to open a banking relationship with a fintech or big tech firm in the next 3 years.

Traditional banks have many advantages over most fintech firms and neobanks, such as funding and customers’ trust. However, legacy operating systems are acting as a technology anchor, weighing down the ability for traditional financial institutions to respond for an increasingly tech-savvy generation.

According to KPMG, the size of the global neobanking market is expected to hit $333.4 billion by 2026, at a compound annual growth rate (CAGR) of 47.1%. But, this estimate can change dramatically based on the ability of legacy financial institutions to respond to the needs of a digital consumer marketplace. The key to success (for any financial competitor) lies in fulfilling the needs of a segment of the marketplace, and adopting the right technology, business strategy and work culture.

Innovation Provides Differentiation Opportunity

More than ever, innovation is redefining how banks operate and the services they offer to customers. It is even possible that innovation will redefine the business model of many financial institutions as they try to serve new segments or partner for success.

The need for rapid and ongoing innovation impacts every component of banking, from new product development, to new ways to deliver services and provide customer support, to back office process rethinking that changes entire banking models.

Despite an ongoing rallying cry for improving the customer experience by financial institutions of all sizes, research by the Digital Banking Report continues to find that innovation efforts are overwhelmingly focused on improving operational efficiency, reducing costs and enhancing risk and security of applications. While these priorities are obviously very important, the consumer and business customer can’t be ignored in the process. This is especially important as fintech and big tech providers continue to improve their customer-centric solutions.

In the survey of banking executives, they mentioned the speed at which Buy Now, Pay Later services were integrated into the financial services product set. Almost 60% of these executives believed that BNPL services will be mainstream by 2025 within traditional banks and credit unions. The question is … what’s next?

By focusing on an overarching innovation framework, banks and credit unions can leverage innovations for long-term success. In the future, innovation must differentiate products, services and entire organizations from the competition.