If you had any doubt that legal medical and recreational marijuana and related derivatives have become a very big business in the U.S., consider that a recent edition of Marijuana Business Magazine ran 154 pages. The issue was stuffed with advertising to serve the needs of marijuana retailers, medical-use clinics, processors, and producers. The goods marketed range from packaging and processing equipment to branded manufactured candies infused with cannabis to marijuana consulting services. There’s been an explosion in entire categories of companies and fledgling trade associations serving the business, as what was once a completely illegal trade has gone legal, or, at least, been decriminalized, in more and more states.

There’s already consumer research to draw from — including categorization of pot-using consumers into “personas.” New Frontier Data, an analytics firm that concentrates solely on the cannabis industry, breaks the customer base into nine segments, including “traditional lifestylers,” “discreet unwinders,” “social opportunists,” and “infrequent conservatives.” The top ranking reason for consuming marijuana-related products in New Frontier’s study was relaxation (66%) followed by pain management (42%) and finally by “making boring things more interesting” (19%).

No longer just a back alley business funded by the mob and other criminal elements, marijuana-based companies have become an industry watched by professional stock analysts, including some from BofA Securities and Canadian Imperial Bank of Commerce, and talked about on The Motley Fool, Seeking Alpha, and Yahoo Finance.

Is this growing business one that banks and credit unions want to serve, or should serve? It’s been a matter of intense debate from boardrooms to the halls of Congress. Among the marijuana news and advice websites there are few bank or credit union ads to be seen.

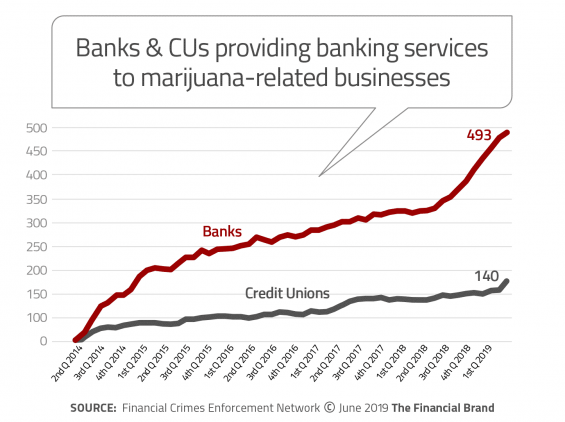

Yet several hundred mostly small banks and credit unions have ventured into this field. As of March 2019 493 banks and 140 credit unions did so, according to the Treasury Department’s Financial Crimes Enforcement Network.

Mixed Interest Among Banking Providers

Most financial institutions serving the cannabis business appear to keep a low profile. When you visit the main websites of these banks and credit unions there isn’t a clue about these specialized banking activities. A handful of active players maintain separate promotional websites for pot-related services or put out a press release about it, and the rest appear to rely on word of mouth and occasional mainstream news coverage.

Some institutions have entered the business and then exited. One example is Florida-based First Green Bank, which began serving that state’s marijuana industry and then mysteriously left it. The mystery was cleared up later, as reported by The Palm Beach Post, when it turned out that Seacoast Bank, which had made an acquisition offer, didn’t want to be associated with the trade.

Most large banking brands have avoided much involvement, if any, in this industry. In early 2019 Business Insider reported rumors that Citigroup has been mulling getting into the business. On the other hand, Jamie Dimon, CEO at JPMorgan Chase, responding to a question about his skepticism about Bitcoin and whether it was a better investment than marijuana, told CNBC Squawk Box that “it is, but we’re not banking pot either.”

Read More:

- Chase Commits To Long-Term ‘Digital Everything’ Strategy

- JPMorgan Chase CMO Says You Can Kiss Traditional Marketing Goodbye

- Marketing Lessons From Chase Bank’s Twitter Blowup

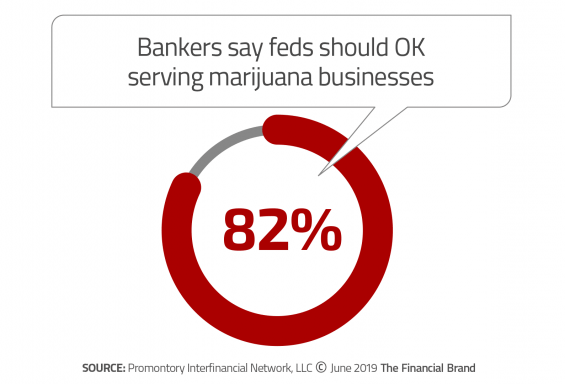

On the other hand, expanding into serving marijuana-related businesses has appeal to banks needing new accounts, more deposits, and added loan volume. In a nationwide survey by Promontory Interfinancial Network, LLC, four out of five bankers polled favor the federal government allowing financial institutions to serve marijuana businesses.

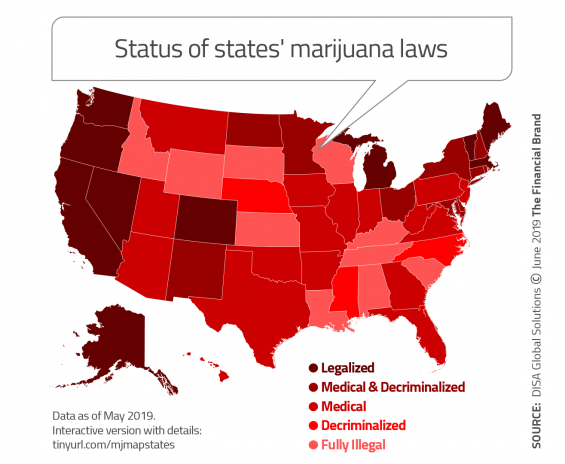

The fact is that while it is booming nationally, the marijuana business exists in a twilight state economically, culturally, and even legally. New Frontier Data says that 33 states and Washington, D.C., have legalized cannabis for many medical uses. Ten states and Washington, D.C., have legalized marijuana for adult recreational use. (There are many nuances on what’s permitted, state by state.)

State laws are a patchwork of licensing schemes and requirements. In one state, for example, a firm must choose to be a seller, a processor or a producer, but not all three. In another, “vertical integration,” combining all three, is mandatory. Under multiple current federal laws, neither medical nor recreational sales of marijuana and other cannabis products are legal.

Hard to be in Business without Business Banking Services

Proponents of serving the pot business among banks and credit unions point out that legally licensed businesses all require banking services in some form. Prominent among these is a way to handle the large amounts of cash the marijuana business generates.

The cash deposits wouldn’t be so large if more retailers and dispensaries could accept credit and debit cards, but many traditional financial institutions and payment processors have declined to offer cannabis businesses merchant card accounts.

In the absence of being able to have a true banking relationship, marijuana-related businesses conduct high-value transactions using cash that other types of firms would never consider using currency for, including paying taxes.

Read More: How to Elevate Bank Business Marketing to Starting Lineup

Banks and Credit Unions that Serve Marijuana Businesses

While serving marijuana/cannabis-derivative businesses has not gone mainstream yet, a growing number of banks (up 13% in the first quarter) and credit unions (up 24%) have been doing this to some degree.

Partner Colorado Credit Union formally entered the business in early 2015, after a six-month pilot in 2014. (Colorado legalized marijuana in 2012.) Today the credit union offers services for approximately 240 marijuana-related firms through its credit union service organization subsidiary, Safe Harbor Private Banking. The firms include retailers and dispensaries, growers, processors, and ancillary supplies and service providers.

Along the way, Sundie Seefried, CEO of Partner and its CUSO, learned the ins and outs of handling such businesses and wrote a self-published how-to book based on the credit union’s experiences.

The subsidiary maintains its own staff of specialized banking officers. A key to making this work is heavy attention to compliance issues.

“This industry was born from the black market, so we have a motto that every dollar is a cartel dollar until we prove otherwise,” explains Amanda McComb, Assistant Vice President at Safe Harbor, in a Bloomberg video.

The credit union felt there was a need to get the massive cash amounts taken in by marijuana businesses off the street. To get a sense of the numbers, consider that Safe Harbor’s clientele alone bring in $140 million in cash every month.

“It’s been a blessing to have Safe Harbor as our institution to bank with,” says Don Andrews of Lodo Wellness Center during the same video. “I can pay all my vendors and suppliers with checks and we don’t have to deal with the stress and strain of having that much cash around a retail business.” In fact, Safe Harbor provides its cannabis customers with placards declaring that no cash is kept on the premises.

Though the learning curve for handling this business has been steep, Seefried says the effort has given her and the credit union “a front-row seat to an emerging market” that is on the threshold of massive growth.

Maps Credit Union, Salem, Ore., has been providing banking services to marijuana-related businesses since 2014. Testifying in Congress in early 2019, Rachel Pross, Chief Risk Officer, says the credit union saw the move as a community service and public safety issue — “though Maps has no position on whether cannabis should be legalized federally, we acknowledge that the voters of Oregon have already spoken on that issue for the people of our state.”

To date, Maps is serving about 500 cannabis businesses, though it does no advertising and the firms must sign an agreement not to talk about their banking relationship. The credit union files Suspicious Activity Reports with FinCEN even on these licensed businesses, per federal law, which Pross says has resulted in thousands of filings since 2017.

“Because the cannabis industry is primarily cash-based, these transaction records would not otherwise be available if financial institutions were not permitted to serve the industry,” says Pross. “We firmly believe that providing banking services to this industry delivers a significant benefit to law enforcement, because Maps is essentially providing free, highly detailed information at least every quarter on cannabis-related monetary activity in the State of Oregon.”

Severn Bank, in Annapolis, Md., has been serving the state’s medicinal marijuana clinic businesses since 2017.

In the publicly traded bank holding company’s 10-K report, several interesting figures appear:

- Cannabis-related deposits added $17 million in deposits in 2018, about 2.2% of deposits.

- Cannabis-related loans added $14.1 million in loans, about 2.1% of loans.

- Deposit service charges rose 188.5% in 2018, due mostly to on-boarding fees charged to medical-use cannabis businesses.

- Interest income related to medical marijuana firms came to $720,000 for the year, and noninterest income came to $1.4 million.

The 10-K also discloses the risks that it sees in serving marijuana businesses, and the iffy state of federal enforcement. “Any change in the federal government’s enforcement position could cause us to cease providing banking services to the medical use cannabis industry in Maryland,” the report states.

O Bee Credit Union, in Tumwater, Wash., credits the structure of the state’s licensing system, enabling full legal marijuana use, for making it easier for the organization to bank cannabis since 2014.

“By having Washington state take a lot of that on itself to make it a cohesive program, it lessened the risks for Washington state-chartered banks and credit unions,” James Collins, President and CEO of O Bee, told South Sound Business.

The credit union’s dedicated cannabis banking page invites visitors: “Let’s be buds.”

However, being a “bud” only goes so far. Collins says the credit union will not lend to marijuana-related businesses. This is because bankruptcy laws involve federal courts. “How do you go to bankruptcy court for a loan if the courts won’t even recognize that kind of business exits?” asks Collins. “So, we aren’t doing any lending.”

Understanding the Compliance Challenges Up Front

When the massive federal anti-money laundering reporting and tracking process first came in decades ago, bankers complained about being drafted to be cops. Ironically, in her book, Safe Harbor’s Seefried explains that one of the necessary tasks of banking marijuana businesses is policing the business itself. If anyone in the firm is dealing the firm’s cannabis on the side or if the firm is handling unregistered crops, this could trigger legal issues.

Such issues have driven growth in specialized cannabis banking compliance software and consulting. Tony Repanich, a veteran banker in pot-friendly Washington state, formed Shield Compliance, where he is President and COO. He notes in a podcast for BAI that the scope of needs of these businesses varies from state to state depending on licensing and state control over the size of the business.

Validating the flow of funds through any cannabis business is part of the challenge of doing this type of banking, according to Repanich. He says that when a banker or credit union executive expresses interest in getting into banking marijuana-related businesses, he asks if the institution really needs the business. If they say that’s not the case, he advises them to stay out of marijuana banking — even though they could be a customer for Shield.

Gregory Deckard, Chairman, President, and CEO of State Bank Northwest, Spokane, Wash., testified earlier this year in Congress that in spite of full legalization in his state, the uncertainty of a potential federal policy shift has kept State Bank out of the business. “The legal stakes are simply too high for me, my board, and my investors to tolerate,” he explains. “We owe it to our community to ensure that our doors remain open.”

“This is a high-risk portfolio,” acknowledges Repanich, and not something for the casual player. Serious underwriting of the business, from both a credit and compliance perspective, should take place before accepting a cent of marijuana money.

Indeed, in his congressional testimony, Washington state banker Greg Deckard makes the point that regulators require banks serving cannabis-related businesses to have an exit plan to unwind loans to such companies. “That requirement does not exist for any other category of lending,” says Deckard.

Repanich also suggests that smaller banks and credit unions may not have the field to themselves much longer. Parts of the cannabis industry are growing and some consolidation has been taking place. Big Tobacco firm Altria put $1.8 billion into a marijuana company in late 2018.

As the companies grow larger, they will require services not in smaller institutions’ skill sets, such as more-complex treasury management.

“So there’s an opportunity for the next tier of institution to step in and provide a broader range of services to this industry,” he says, if they choose to take advantage of it.

The hang-up for most banks and credit unions of any size is the uncertain status of federal enforcement. While others may object on ethical grounds, typically, lobbying groups address the regulation of this activity and disagreements between state and federal law. In testimony and other forums, the groups typically say they have no official position on the legalization of cannabis.

During congressional hearings earlier this year, a former J.P. Morgan & Co. banker and former thrift regulator testified for Smart Approaches to Marijuana. This group opposes legalization of marijuana and any erosion of federal policy regarding the drug. Jonathan Talcott, Chairman of S.A.M., says that “contrary to the promises of legalization the black market hasn’t gone away in legalized states. Many unlicensed operators have storefronts, delivery services, and even pay for internet advertising. It is not far-fetched to think they would also apply for bank accounts were they given the opportunity.”

It’s a tricky market for bank and credit union executives to size up. But clearly it’s on the radar of more and more institutions.