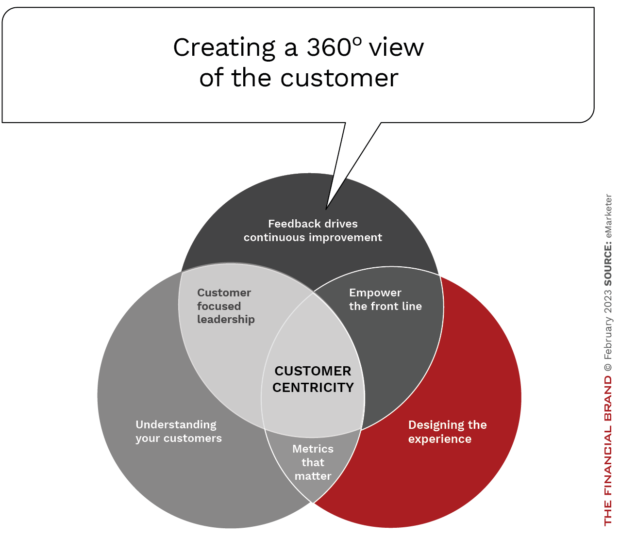

More than just a public relations talking point, customer centricity is a business philosophy that prioritizes the needs of customers in all business operations and decision making. For banks and credit unions, this goes beyond just good customer service. It includes product delivery, innovation strategies, marketing communications and financial wellness support.

When the customer becomes the core of a business, data is collected, analyzed and deployed on a regular basis to get a full 360-degree view of the customer. This data helps banks and credit unions in the following ways:

- Better understanding buying behavior, interests and engagement across entire customer journey.

- Identifying opportunities for new products, services, and promotions.

- Building segmentation strategies for increased loyalty and lifetime value.

- Empowering employees to better democratize experiences.

As financial institutions increase their focus on customer centricity, the importance of improving experiences and moving from transactional engagement to relational engagement increases. There are four ways financial institutions can directly impact the customer experience to become more future-ready, according to Capgemini:

- Transform traditional brick-and-mortar facilities into “experience centers.”

- Collaborate with fintech and other third party providers to overcome business model gaps.

- Increase assistance with consumers on their financial wellness journey.

- Establish an “owner” of the overarching customer engagement.

The future of customer centricity in banking involves a combination of tech and business model transformation. Leveraging digital technologies, combined with the power of marketplace collaboration and enhanced utilization of data, financial institutions can offer a seamless, personalized and superior omnichannel experience.

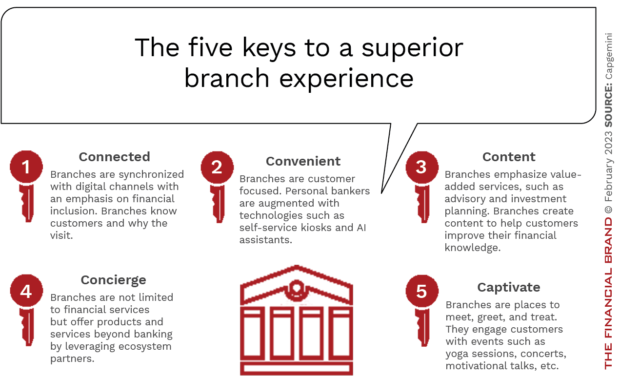

Transform Traditional Branches

In the past, banks and credit unions leveraged branches to build market share. As digital banking adoption increased, especially during the pandemic, financial institutions were forced to rethink the delivery of banking services. Increasing the need to reimagine the functionality of branches was the impact of fintech providers that delivered a superior digital experience for everyday transactions as well as the need to reduce operational expenses.

A Nasdaq report indicates that building a full-service office facility can cost more than $1.5 million in the United States, with an annual operating cost of almost $1 million per branch. With labor costs increasing, and operational costs remaining higher than digital alternatives, few branches are profitable. Despite this ominous metric, most consumers still find branches relevant.

Capgemini’s World Retail Banking Report 2022 states that 75% of customers believe branches are an important channel, but they want more than just transactional capabilities. Specifically, 64% said they wanted self-service options, 44% seek an extended workplace, and 31% indicated an interest in a more immersive (augmented reality/virtual reality) experience. The challenge is to integrate the branch with other channels for an omnichannel experience.

With an omnichannel experience, branches would leverage customer relationship management platforms that have seamless integration with other digital channels, providing highly personalized service and product recommendations. “Redesigned branches will feature streamlined layouts, more digital and self-service tools, and rationalized human-driven (teller) activities to boost effectiveness through cost savings and increased sales,” states Capgemini. The result will be greater engagement and increased value transfer between the financial institution and the customer.

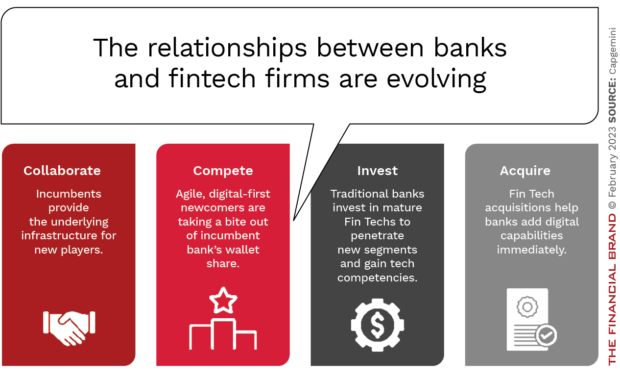

Create Purpose-Driven Fintech Collaborations

To respond to increased demands from a more digitally savvy customer base, banks and credit unions are increasingly pursuing collaborations with fintech firms and third-party providers. These partnerships (and acquisitions) help to overcome business model gaps, leveraging each other’s strengths and addressing their respective weaknesses, creating mutual benefits.

In 2022, there were seven bank acquisitions of fintech firms, according to a report from S&P Global Market Intelligence. In 2021, there were eight buy-side bank deals. With a digital customer base, but lower-than-desired profitability, fintech firms can help traditional banking organizations build new value propositions, develop cross-sell opportunities, and provide an active customer base, according to Capgemini.

Beyond an acquisition, fintech collaborations can also provide innovation opportunities that offer both speed and scale of deployment. Recently many traditional financial institutions have looked to third-party collaborations for the building of improved digital account opening processes, enhanced rewards programs and better mobile banking experiences. Other collaborations have been executed to improve operational efficiencies and reduce costs and to access new technologies offered by fintech firms.

Read More:

- Where to Look for Value in the Fintech Wreckage

- Banks Should Scavenge Troubled Fintechs’ Talent and Technology

- Why Neobanks and Fintechs Have Made ‘Underbanked’ an Obsolete Term

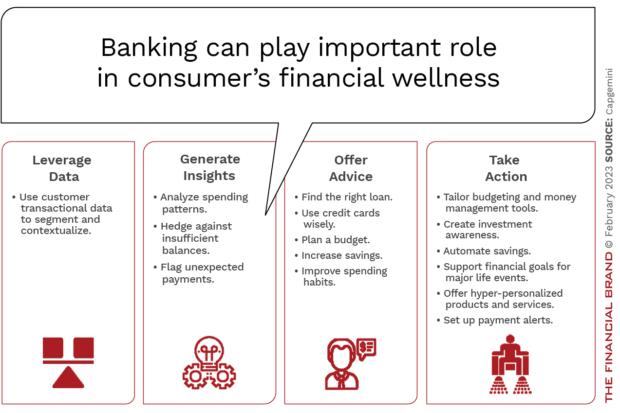

Assist with Customer’s Financial Wellness Journey

As the economy becomes less predictable and cost-of-living pressures increase, more consumers are looking for ways to improve their overall financial wellness. Because of the banking industry’s expertise, reach, trust, data and technology capabilities, banks and credit unions are well positioned to assist consumers with their search for financial wellness assistance and help them make informed financial decisions. The payoffs can be significant.

The 2022 J.D. Power Retail Banking Satisfaction survey revealed that only 44% of U.S. banks support customers during financial hardship. Meanwhile, about 63% of U.S. customers said they would switch banks if they were not supported, while 78% said they would stay if they received support.

Banks and credit unions are in an advantageous position because they have access to a wealth of data and analytics that can be used to understand consumers’ financial behavior and needs, and to develop targeted financial wellness programs and resources. Financial institutions also have strong infrastructures and technology capabilities that can be leveraged to develop and deliver financial wellness resources and tools, such as mobile banking apps, online financial management tools, financial planning calculators and highly targeted financial wellness content. Retail banks are also exploring fintech partnerships to augment their financial wellness offerings.

Ultimately, financial wellness efforts are an excellent way for banks and credit unions to move from transactions to engagements, building trust and loyalty. Financial institutions that offer robust financial wellness programs and resources can also differentiate themselves from competitors and gain a competitive advantage in the marketplace at a time when consumers are searching for answers to financial questions more than ever.

Read more:

- Core Issue: Plug-and-Play Trend Is Transformative for Banks

- Three Ways to Invest in Innovation for Growth-Minded Banks

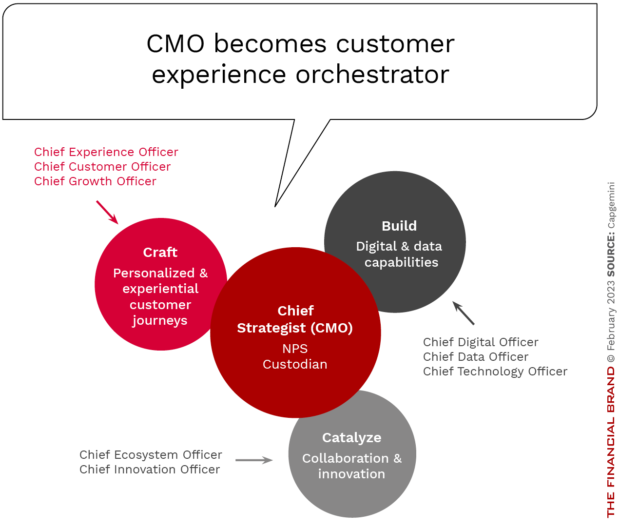

Establish an ‘Owner’ of Customer Engagement

A good customer experience, while important, is only a transactional interaction between the customer and the financial institution. On the other hand, customer engagement involves ongoing, two-way communication and a commitment to meeting customers’ evolving needs and expectations. This level of interaction and commitment can lead to a stronger, more sustainable relationship between the customer and the brand. To achieve this level of relationship requires a central point of authority.

The Chief Marketing Officer (CMO) persona (or another key central point of authority) will be pivotal to leveraging data, artificial intelligence and analytics tools to create higher levels of engagement and a better customer experience. The data and analytics allow for the development of personalized products and solutions with omnichannel visibility, creating recurring customer interactions and greater user-level data.

The result will be a flywheel effect, decreasing the cost of acquisition, increasing engagement and revenue potential and reducing the potential for attrition.

The “owner” of the customer relationship may be the CMO or another individual within the bank or credit union. According to the 2022 World Retail Banking Report, 34% of the assigned leaders said they directly manage marketing analytics, and 26% said they oversee digital partnerships. In addition, about 74% said they have direct responsibility for innovative marketing strategies and planning, and 22% directly manage end-to-end customer experiences or have access to complete customer profiles.

“Customers have numerous financial services alternatives, but expected 2023 market volatility offers banks an opportunity to power up their game by leveraging their scale, assets, broad customer base, and regulatory knowledge,” according to Capgemini. To improve marketplace differentiation and become a trusted financial partner, banks and credit unions will need to better understand the needs, motivations, challenges and behaviors of customers across the entire customer journey.