As the banking industry tries to upgrade core systems, improve mobile delivery and respond to new regulatory requirements, the need for technology expertise has never been greater. Beyond the need to support technological innovation at the management and staff levels, banks and credit unions are facing the need to increase the technology expertise at the board level as well.

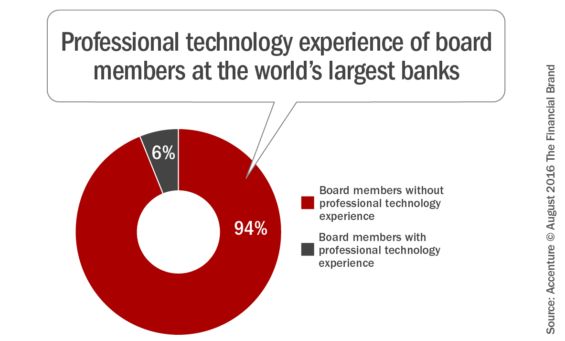

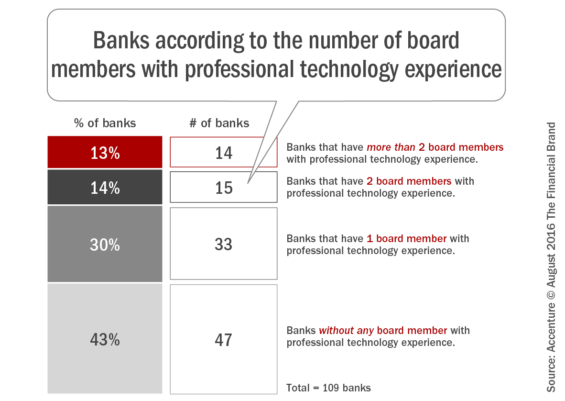

Unfortunately, less than 6% of boardroom members and 3% of CEOs at the world’s largest banks have professional technology experience, according to the Accenture report. In addition, of the more than 100 of the largest banks surveyed across the globe, 43% of boards had no board member with professional technology experience, while 13% had more than two.

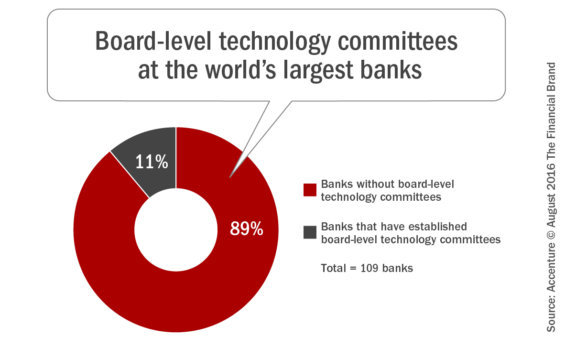

The survey also found that only 11% of banks had technology committees at board level, suggesting that the potential (and risk) of technological transformation may not be fully grasped by many boards of directors. According to the report, for a director to be classified as having ‘professional technology experience’ they must have held a senior technology position (chief information officer, chief technology officer or chief digital officer) at a company or had senior responsibility at a technology firm.

“Many of the biggest challenges now confronting banking are intimately connected with technology, so directors need a robust understanding of technology if they are to make informed decisions,” said Richard Lumb, group chief executive of financial services at Accenture. “Fintech, cyber-security, IT resilience and technology implications of regulatory changes have all become critical board-level issues, but many bank boards simply don’t have adequate expertise to assess these issues and make decisions about strategy, investment and how to best allocate technology resources.”

The Intersection of Technology and Boards

The financial services industry has long been the biggest spender on IT. Banks will spend more than $360 billion worldwide in 2016, more than any other sector, according to Gartner.

Unlike the past, however, when technology made back-office processing more efficient and had little bearing on the relationship with the customer, digital is changing everything. Today, technology is a central part of the business strategy at banks and credit unions. Digital not only means new banking channels, it also offers a unique opportunity for banking organizations to drive growth and profitability.

Technology Innovations: Digital technologies open up new revenue opportunities, serving customers more contextually than in the past. Advanced analytics lets banks and credit unions offer highly personalized financial services and advice, while improving customer engagement and the overall customer experience.

By digitizing manual, paper-based processes, and increasing self-service options for customers, digital can also help reduce costs while improving customer service.

Digital disruption isn’t confined to within the legacy banking firewalls. New start-ups and fintech firms are rapidly making their way into the domains of traditional banking. New solution-specific firms, and even large technology organizations such as Apple and PayPal, are changing the competitive landscape.

According to Accenture, “These new competitors could put about one-third of bank revenues at risk by 2020. As a result, bank boards need a full understanding of the implications, opportunities and threats around technology in order to set strategies.”

Core Banking Systems: Most legacy banks have core banking systems that date back to the 1970s or even 1960s. As new innovations have been added, such as ATMs, online banking, mobile banking, etc. banks and credit unions have patched on new IT systems around the core.

As a result, banks have spent the majority of their IT budgets just to maintain antiquated infrastructures, as opposed to developing new digital capabilities that are needed to remain competitive. In fact, according to Celent, three-quarters of all IT spending in 2014 went to maintaining aging systems, leaving only a quarter to spend on innovation.

As organizations are faced with the decision to patch up ancient systems, or biting the bullet and revamping entire core systems, boards of directors will need to determine prioritization and investment levels.

Regulatory Compliance: A wide variety of new compliance regulations are changing the way banks and credit unions interact with customers, monitor staff and report to regulators. All of these regulations require time-consuming and expensive reprogramming and changes to IT systems.

The capacity of financial institutions to manage existing IT infrastructure, cope with changes taking place, and address growing cybersecurity risks requires close supervision from the highest level of the organization … the board.

“These reforms are already at the top of boardrooms’ agendas, but given their technology implications, boards will need technology expertise to make informed decisions,” says the Accenture report.

Board-Level Technology Expertise Lacking Globally

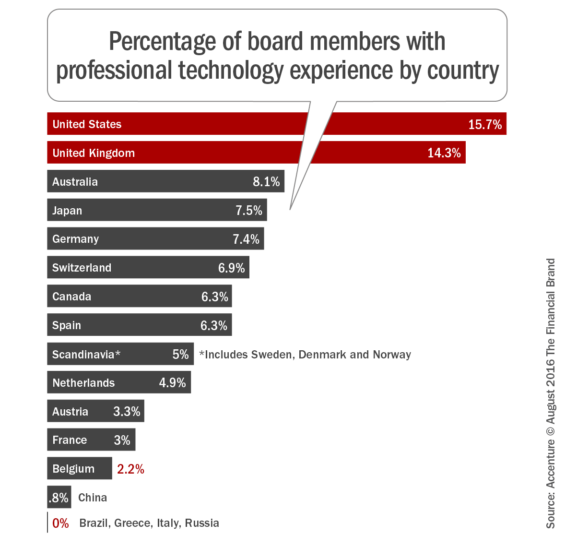

While boards of U.S. and U.K. banks have the most directors with professional technology backgrounds, numbers are still low in these countries and even worse elsewhere.

According to the related research, the financial services industry has one of the lowest percentages of boardroom digital expertise

(13%), behind the health care (39%), consumer products (42%) and technology (48%) industries.

The Accenture research found:

- In North American banks (U.S. and Canada), 12.1% of board members have professional technology experience, compared with 5.1% for European banks and 5% for Asian banks.

- While the boards of banks in the U.S. and the U.K. have higher percentages of directors with professional technology experience than those in any other countries, the numbers are still low, at 16% of directors in the US and 14% in the UK.

- Less than 1% of directors at Chinese banks – and none of the directors at Brazilian, Greek, Italian or Russian banks – have professional technology experience.

Preparing the Boardroom for a Digital Future

My friend, Chris Skinner, has been beating the drum for years, saying that his biggest frustration with incumbent banks is that they continue to be run by financiers, not technologists. According to Skinner, “Digital transformation is not a project run by a function, but a complete change of the bank. You cannot change the bank without strong leadership … and most are failing.”

Accenture recommends that financial institutions respond accordingly:

- Put technology on the boardroom agenda: Having one or two technology experts in the boardroom is not enough. To bring about change in boardroom culture and to better understand the risks and opportunities that technology provides, technology must take a much higher priority on the boardroom agenda.

- Provide technology coaching for boards: Boards need in-depth personalized coaching. Accenture recommends six-month coaching

programs that include insights into the technology landscape and the business implications for the financial services industry as well as other sectors. - Establishment of technology committees: These committees should be similar to audit and risk committees and should include both internal and external experts who can advise the board on technology issues. Currently, only 11% of leading banks surveyed have this type of committee in place.

As we have seen in a number of other studies in the banking industry, realizing that change is occurring is not even half the battle. The real challenge is to take meaningful action on this knowledge.

There needs to be a very clear, well documented and communicated innovation agenda with measurable objectives, investment commitments and an execution strategy. Boards of directors must lead this effort, beginning with filling the current technology expertise gap in their own boardrooms.

As was said in the Accenture report, “One thing is certain – change is coming. How boards deal with that change caused by the challenges and opportunities of technology will go a long way to determining who become the winners and losers of the coming transformation.”