Technology is constantly changing, and for banks and credit unions it can be difficult to keep up. Digital products and services that were once considered innovative are now common and are simply expected by customers. And sometimes once-hot areas — like buy now, pay later — suddenly lose their luster.

Technology has never been more important for financial institutions, and that goes for the largest global bank to the smallest, one-location credit union. Increased competition from non-financial firms, ever-rising consumer expectations and new strategies based on embedded finance principles are shaping the way financial services are delivered.

Increasingly technologies that were the “future” just a few years ago, like APIs and cloud computing, are becoming commonplace. Others, like artificial intelligence, continue to be a top tech trend because the potential has so far not been tapped to a great extent.

With that said, here are some of the most important technologies banks and credit unions must focus on now and for the foreseeable future, based on insights from leading financial technology analysts.

Trend 1: Using AI and Analytics to Deliver True Personalization

One-to-one personalization is the holy grail for financial marketers. Yet most still do not feel confident in their ability to deliver a truly personalized experience.

To solve this issue, financial institutions need to make greater use of artificial intelligence, machine learning and predictive analytics to deliver targeted offers tailored to individual customers, according to Capgemini in its Technovision 2022 report.

“The availability of real-time usage data (e.g., search history) pertaining to each customer helps build a unified customer profile, ensuring that insights are driven out of every interaction, thus opening up new opportunities for FIs to maximize their appeal,” the firm writes.

Capgemini adds that financial firms should integrate real-time data capture and analysis

capabilities with their customer experience offerings. As an example, the firm says personalized credit offers can be integrated with e-commerce companies taking into consideration credit risk assessment and customer behavior.

To achieve this, Capgemini advises that cutting edge applications are needed; ones that are not static but continuously changing.

“Many applications no longer look like the ones we used to know, as they morph into a connected mesh of microservices,” the firm writes. (Microservices are applications that are run independently and talk to each other via APIs.) “To satisfy rapidly changing demands, personalize experiences, facilitate real-time decision-making, and enable innovation around transaction services, these applications need to be built on cloud-native and microservices-based capabilities.”

Read More: How Data and AI is Transforming the Future of Banking

Trend 2: Self-Learning Autonomous Banking Systems

Financial institutions will use autonomous, self-learning computer programs to increasingly serve in customer-facing situations, Gartner predicts in its 2022 banking technology trends report.

Gartner calls these programs “autonomic systems” and describes them as “self-managed physical or software systems that learn from their environments and dynamically modify their own algorithms in real-time to optimize their behavior in complex ecosystems.” The technology research and consulting firm cites wealth management robo advisors as an example of a current, low-level version of an autonomic system. In the future, these systems could even play a role in powering robotic assistants in physical branches.

Robot Helper:

While AI in financial services is mostly software-based, in the future it could be used to power hardware-based systems that help customers in smart branches.

“Currently, autonomic systems are mostly software-based in the banking context. However, humanoid robots are emerging in smart branches that are examples of hardware-based autonomous systems that cater to clients and customers,” Gartner states. “They could be applied in autonomous debt management, personal finance assistants and automated lending.”

Gartner VP and analyst, Moutusi Sau describes autonomic systems as a “long-term solution that provides new options for business transformation in financial services.”

Read More:

- Why KeyBank Believes ‘Embedded Banking’ Is the Future of the Industry

- 4 Tech Trends That Are Massively Transforming Banking

- AI in Banking: Top Priorities for 2022 (And Beyond)

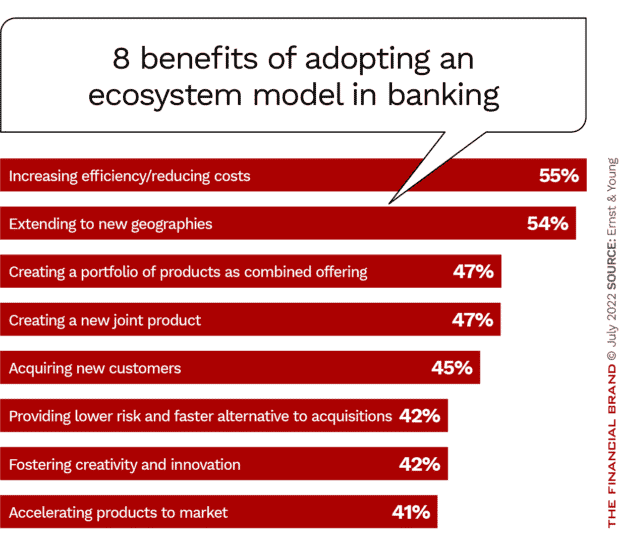

Trend 3: Harnessing the Power of Banking Ecosystems

The advent of concepts such as open banking and embedded finance has brought the idea of banks as ecosystem facilitators to the fore. All these related topics are as much business trends as technology trends, but as with so many banking developments, changing technology is the catalyst.

Banks will play a greater role in ecosystems in the coming years, both by offering their own customers access to third party products and services, as well as facilitating embedded finance. Examples include helping car manufacturers to offer subscription services and enabling telecom companies’ customers to charge the cost of movie rentals and other content to their phone bills, according to an analysis from Ernst and Young.

Financial services respondents surveyed by EY cited increased efficiency and cost reduction, expanding to new geographies and creating new products in conjunction with other organizations as the top benefits of ecosystems.

“From direct-to-consumer retail to complete homebuying services delivered on an app, companies from a wide range of sectors are acting on their belief that they cannot serve their customers on their own — especially when it comes to ensuring their financial peace of mind,” EY wrote. “To deliver the experiences customers increasingly expect, embedded finance is becoming not just a nice to have, but a must have for many businesses.”

Clearly this could be a significant opportunity for the financial institutions that are able to embrace and support such nontraditional arrangements.

To get started in an ecosystem environment, EY advised banks to think about what customers want from them and what partners might help them serve that need. Banks then need to define their role in that ecosystem, and ensure that both the technology infrastructure as well as leadership vision is in place to move forward.

“By identifying where and how an ecosystem can add value, defining your role, and transforming to deliver — financial services companies have a roadmap that will enable them to make finance effortless for their ecosystem partners and their end customers,” wrote Jan Bellens, EY Global Banking and Capital Markets Sector Leader. “That will increasingly make financial services providers key to delivering the value that ecosystems promise.”

Trend 4: Metaverse Impact on Digital Assets, the Workplace and CX

There’s so much hype about the metaverse that it’s easy to file it as “worry about later.” Many observers believe, however, that move would be a mistake for financial institutions. One reason is that “metaverse” encompasses much more than the popular conception of virtual reality headsets and gaming.

While there is no neat, simple definition for “the metaverse,” the term is typically used to describe the future iteration of the internet, “made up of persistent, shared, 3D virtual spaces linked into a perceived virtual universe,” as Forbes states.

Despite the emphasis on “future,” the metaverse already exists in a variety of ways, several of them relevant to financial institutions.

The rise of blockchain, non-traditional digital assets and virtual products in the metaverse will lead to a proliferation of digital goods that people need securely stored. Banks can play a key role in facilitating transactions in digital realms and helping consumers store digital assets, of which non-fungible tokens (NFTs) are a growing part.

“With blockchain enabling monetization of the metaverse, companies are piling in to facilitate and create digital assets for purchase,” Morgan Stanley observes. “Some of the biggest technology enterprises are expanding their online platforms in which people can work, play games and socialize, while well-known consumer companies are creating NFTs to sell. On platforms that sell digital land, brands are also creating online versions of their stores.”

Virtual Lockbox:

Banks can play a key role in helping customers store and secure digital assets in the metaverse.

Blockchain powered transactions in the metaverse pose intriguing possibilities for banking, Accenture maintains. Becoming a trusted custodian of digital assets is a main possibility, the firm said.

“Asking people to take care of their most valuable digital assets on their own is asking for trouble,” Accenture wrote. “People implicitly trust banks with their money right now. There’s no reason why they shouldn’t trust banks with their money and digital assets.”

Read More: 14 Surprising Predictions on the Future of Banking

Beyond digital assets, the metaverse will impact banks and credit unions in two key areas, as outlined in “The Banker’s Guide to the Metaverse,” by Jim Marous, Co-Publisher of The Financial Brand, and CEO of the Digital Banking Report.

1. The metaverse will change the future of work, with much more immersive forms of virtual collaboration and more interactive learning and development. McKinsey predicts the emergence of AI-enabled “digital twins” — virtual coworkers that can handle repetitive work.

2. The metaverse has great potential to take customer engagement to a new level — not only personalized but with a greater ability to emotionally engage consumers. Simple examples include enabling a customer to virtually explore the house of their dreams, in 3D, or sit in the driver’s seat of a virtual version of a car they want to buy, beyond what is possible today.