Never before has the importance of technology been greater in financial services. Competition from fintech firms and big tech giants, increased expectations from the consumer, and new innovations connecting data to digital delivery are requiring banks and credit unions to embrace new technologies in order to build winning strategies.

Here are some of the most important technologies banks must focus on this year and in the foreseeable future. These are in no particular order, since each organization will be different as to the prioritization and investment allocation. Suffice it to say, however, than none should be ignored.

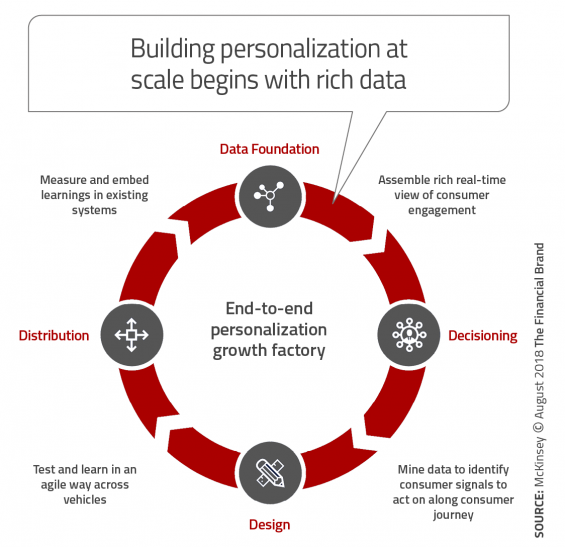

1. Using Data and AI for Personalization at Scale

When it comes to personalization, consumers are pretty clear what they want. They want recommendations that they wouldn’t have thought of themselves, and a clear direction about what they should buy when they are shopping for a product or service. In other words, financial institutions should show consumers that they have been listening and learning from their activities.

People also want their banking providers to know them, look out for them, and reward them no matter what channel they use or what time of the day or night it is. This includes letting them know their overall financial status — on demand. Finally, banks and credit unions must continuously show the value they provide for the insight consumers let them collect.

With artificial intelligence (AI), there is the potential to transform customer experiences and establish entirely new business models in banking. To achieve the highest level of results, there needs to be a collaboration between humans and machines that will provide a humanized experience that is different for each customer.

Read More: Banking Providers Still Aren’t Ready for Big Data

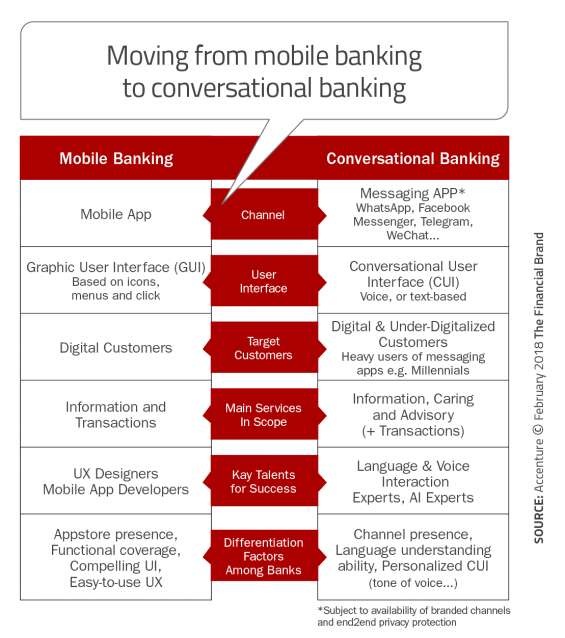

2. Voice-First Banking

A major part of the voice-first paradigm is a modern “intelligent agent” (also known as “intelligent assistant”). Over time, all of us will have many, perhaps dozens, of these agents interacting with each other and acting on our behalf. These agents will be the “ghost in the machine” in voice-first devices. They will be dispatched independently of the fundamental software and form a secondary layer that can fluidly connect between a spectrum of services and systems.

Most financial organizations will move from basic dialogue and account inquiries to doing transactions using voice commands. This can include being able to execute payments using voice commands, as well as doing account transfers and establishing account alerts using voice commands. Many believe that in the next five years, 50% of all banking interactions will be via voice-first devices.

With the vast majority of consumers having banking relationships spanning a decade or longer, the integration of voice, long-term transactional analysis, geolocation, and current contextual learnings combined with preferences and behaviors outside of banking over time, is where the power of AI and voice commerce becomes really exciting.

3. Open Banking

While the largest tech firms — Google, Apple, Facebook, Amazon (GAFA) — are leading the charge towards implementing open API platforms, the model they use may not be the one most banking organizations should follow. Not only do most financial institutions lack the technical expertise or the financial wherewithal to implement these models and support a vast developer community, the ability to acquire new customers to replicate their success is unlikely.

That said, an open banking platform future is within sight for financial organizations of all sizes. For instance, account aggregation is becoming much more commonplace, with firms like Citibank developing completely new digital-only products with this capability. Similarly, traditional banking functions like taking deposits or making payments could become integrated within non-traditional organizations (Starbucks, Amazon, etc.). In the end, key managers in virtually all financial organizations should already be meeting to determine what their organization may look like in the future and how services will be created, marketed and distributed.

4. Digital-Only Banks

Creating a digital-only banking proposition involves aligning new technologies and solutions with the legacy bank’s existing design, brand value and business model. There must be the involvement of leaders who are tech-savvy, building technology with customer-centric approach. Financial institutions can also leverage the technical capabilities of fintech startups to assist in the development of digital-only banks.

Having a digital-only proposition may become increasingly important as more non-traditional banking choices are available to consumers today, enticing them to switch banks for better customized services and value propositions. According to an Accenture report, “banking consumers in North America want it all — deals and discounts, convenience, relevance and banking customer experiences that combine the latest in digital banking with human interaction. Consumers will share personal data to get what they want and switch banks if they do not.”

Read More: 25 Digital-Only Banks to Watch

5. Cybersecurity

There is no doubt that the increased use of technology and digital channels have made the banking industry more susceptible to cyber-attacks and have forced banks and credit unions to be in the unenviable position of playing ‘catch up’. New open banking regulations that require banks to share customer information with third-party providers makes the industry even more vulnerable.

Now more than ever, banks must become proactive in their handling of data protection and managing cybersecurity risks. Unfortunately, consumers want the best of both worlds — ease of use and increased protection of data and identity. This will require the banking industry to implement multi-factor authentication, secure applications, digital signatures, and other forms of security such as biometrics.

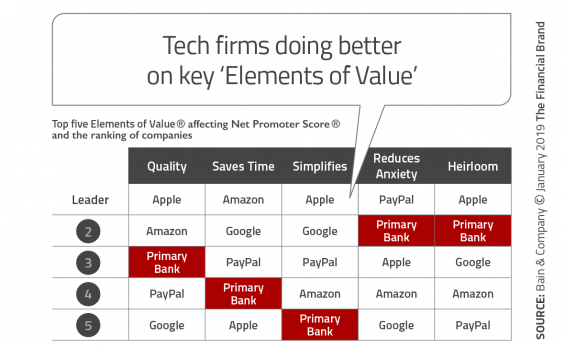

6. Threat of Big Tech

Almost six in ten consumers who are looking to move to a new primary financial institution (or would consider doing so) are open to Big-Tech firms such as Google, Amazon, Facebook or Apple, according to a report from Novantas. This represents a 14-point increase over the 2017 survey, illustrating the potential impact of a major banking product introduction by any of the major tech companies.

One of the primary benefits traditional banks and credit unions had over their competition in the past was trust. Nobody wants to put their life savings at risk or to partner with an organization that wouldn’t protect their identity and privacy. According to recent surveys, however, it does not appear as though trust is a big problem for firms like Amazon. In fact, many consumers trust Amazon more than their current primary bank.

If an organization wants to improve their standing against the likes of Google, Amazon, Facebook and Apple, it is best to focus on becoming a much better digital organization and making it easier for digital consumers to do business with you. That may require partnering with specialists or solution providers that excel in these transformations, but the investment is important as the gap in performance between the best and the mass is widening every day.

7. Blockchain Tipping Point

More and more financial institutions are using blockchain technology or are in the process of implementing blockchain capabilities given its myriad applications. These tests and roll-outs could push blockchain into mainstream adoption in 2019, especially at larger organizations.

For the most part, the focus of blockchain implementations has been around cost reduction and process simplification. The adoption of blockchain in payments, remittances, provenance, and traceability are where blockchain technology seems to be used the most extensively currently.

According to CBInsights, “For use cases that don’t need a high degree of decentralization — but could benefit from better coordination — blockchain’s cousin, ‘distributed ledger technology (DLT),’ could help organizations establish better governance and standards around data sharing and collaboration.”

8. Cloud-Based Solutions

According to the American Bankers Association, banks are generally receptive to cloud-based core banking, with 29% saying they would consider it, 50% saying they were unsure and 21% saying they would not consider it. Many experts think cloud-based core banking will soon become more mainstream, with many believing that the majority of new core banking projects launched by 2020 will be in the cloud.

Much of the momentum around cloud-based solutions is because any financial institution relying on a legacy infrastructure cannot compete against faster and more innovative digital competitors. Implementing cloud technology automates operations and workflows, resulting in increased efficiency, security and cost savings.

Whether banks go with a public or private cloud, security of data, identities, etc. is essential. And while cloud-based core banking may not be the biggest trend right now, banks and credit unions should consider this one of the most important technology trends in the future.