Three of five Americans believe that their banking providers are failing to keep up with their needs in today’s digital world, leading many to wonder if traditional financial institutions will disappear… and what kinds of financial service providers might emerge to take their place.

57% of respondents in a study fielded by Blumberg Capital believe that the traditional banks and credit unions around today will cease to exist within their lifetime. Conversely, nearly 70% believe that fintech players are making their financial lives better and improving their financial health. The findings suggest a murky and difficult future for traditional financial institutions that fail to embrace new technologies and keep up with the pace of change in the new Digital Age.

Blumberg’s national survey of over 2,000 American adults asked respondents what they thought about traditional banks, credit unions, fintech companies and various new financial technologies. At a high level, the survey found that three in five Americans share a positive view of fintech generally, and nearly three-quarters agree that fintech players empower consumers with more control over their finances.

For instance, 70% of Americans believe that new solutions such as digital banking, online lending, payments and financial services, are making financial transactions easier than ever. 69% of Americans think the latest financial tech tools will help everyone be better off financially, and 65% of Americans agree that fintech levels the playing field by providing access to services previously only available to the wealthy.

Despite consumers’ apparent enthusiasm for fintech, there are still some major challenges that are preventing wider adoption of fintech services, specifically concerns over both security and privacy. The Blumberg survey revealed that 65% of Americans listed security as the main priority when considering features in a financial institution, and 72% of Americans listed security as something they worry about with the new banking services online and they are not completely confident their financial information is secure or private.

“Between the negative headlines about banks and American’s general distrust of large financial institutions, banking as we know it must change,” said David Blumberg, founder and managing partner of Blumberg Capital. “While no one knows what will happen in the banking business over the next 20 years, it’s clear that more Americans are increasingly dissatisfied and are excited to embrace new technologies.”

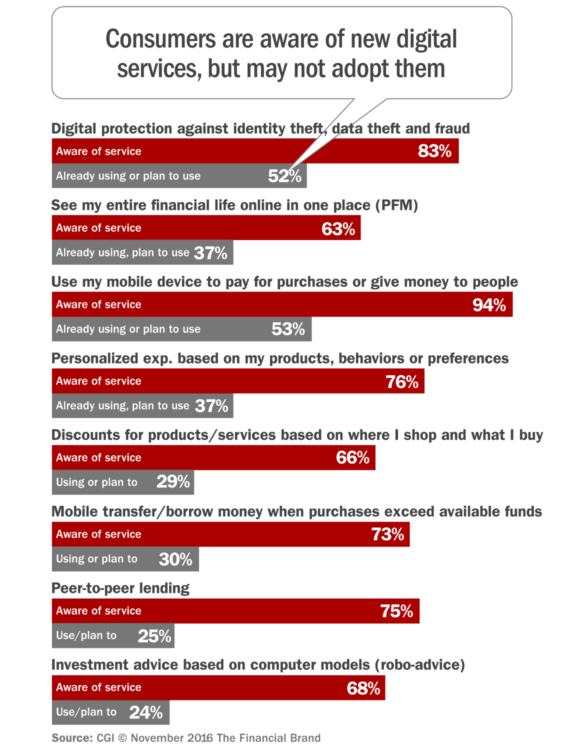

In another study, CGI surveyed 1,670 consumers in eight countries including the U.S. and Canada to examine 12 leading fintech-driven service concepts, including digital identity and fraud protection, aggregated personal financial management, mobile payments, and personalized digital experiences.

In CGI’s study, 61% of respondents identified personal financial management — including the ability to see all personal financial information in one place — as a highly valued service. 94% said are aware of mobile payments, with 53% saying they intend to use the service service.

CGI found that three quarters of consumers would prefer to acquire these new digital services from their current financial institution or another traditional provider over a non-traditional provider.

It may sound paradoxical. On one hand, consumers say banks will be extinct. On the other hand, consumers say they want to add more digital services from their current banking providers. Despite this apparent contradiction, it actually makes sense. Consumers are essentially saying that if traditional financial institutions don’t evolve, they could go out of business; but if traditional banks and credit unions can successfully grow and adapt, consumers would prefer to utilize them for new, digital services, features and tools. One way or another, consumers will get the services they want and need, either through traditional banks and credit unions (their preference) or through fintech players (not their first choice).

“Incumbent banks are well positioned to offer new digital financial services based on their trusted relationships with consumers,” said Kevin Poe, VP/Global Lead for Retail Banking at CGI. “Partnerships with fintech firms can allow banks to move more quickly — one of the approaches banks are taking to meet rising customer expectations for fast, personalized digital services.”

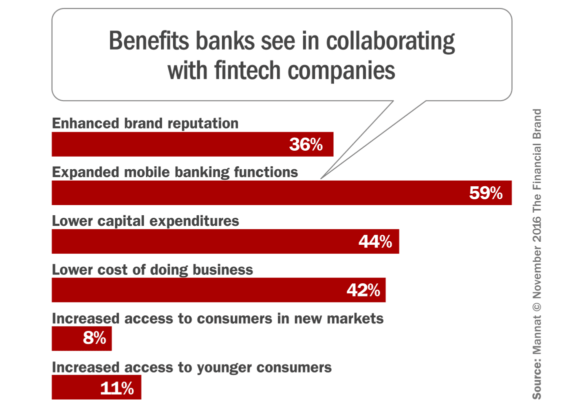

Another study by Manatt found that 54% of traditional institutions and 58% of fintech companies say they see each other as potential partners. On the bank side, respondents in the Manatt report cited a wide range of reasons for viewing fintech in a positive light. Specifically they singled out fintech’s ability to improve their digital services and decrease their technology costs.

Only 5% of traditional banks in Mannat’s survey said they view fintech players as a competitive threat.

There are differing views when it comes to collaboration between established banking institutions and fintech companies. For bank respondents, a large majority view working with fintech players as either “essential” (43%) or “very important” (43%), whereas just 16% of fintech respondents feel it is “essential” to work with banking partners. Over one-third of fintech participants (37%) said they believe it is “not important” to work with any financial institutions, arguing instead that they can thrive own — by pursuing other market segments or by targeting consumers through different means.

In Mannat’s research, nearly half of bank respondents said their institutions were only somewhat prepared (43%) or somewhat unprepared (5%) to address the challenges and opportunities presented by fintech. At the same time, most respondents said their board of directors had taken concrete steps to aid in the effort. More than four out of five said board members had attended conferences to learn about fintech, and the same percentage said directors had held meetings with fintech companies to discuss the potential for collaboration. 59% said their boards had also conducted a formal study of the opportunities and risks associated with fintech threats.