Developers in financial services know that this industry has a special set of problems, from clunky legacy software to intricate rules and regulations. At times, the situation can seem hopeless. How are bankers supposed to innovate in a space that has been built to stay exactly the way it is?

One solution is to focus more directly on application programming interfaces (APIs). APIs have been used at banks and credit unions for decades, allowing internal developers the ability to interact with banking functionality without having to interact directly with the organization’s back-end systems. The beauty of an API is that it can modernize legacy infrastructure.

The difference today is that financial institutions are allowing external access, expanding the possible use cases exponentially. Peter Wannemacher, a senior analyst with Forrester Research, said that “APIs will be, in the near future, a necessary and valuable means by which banks will do their jobs.” He added, “There’s a component of inevitability.” Tech writer Brian Koles says, “A company without APIs is like a computer without internet.”

APIs are being used primarily to allow for the building of fintech solutions with a reduced time to market. Some banks have started this journey, with APIs blurring the lines between fintech firms and legacy financial institutions, marking a new era of progress in banking.

Let’s look at three examples.

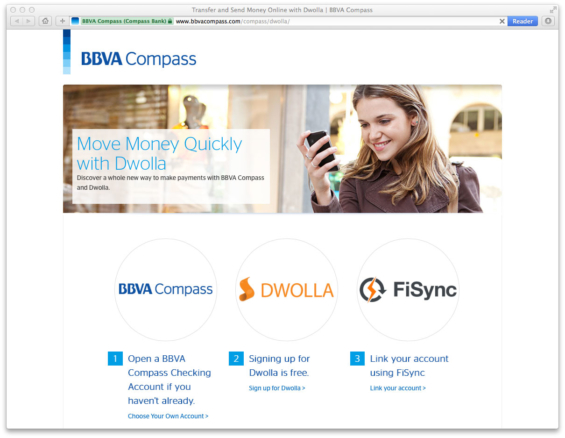

1. BBVA Compass / Dwolla

BBVA Compass is leading the charge toward open APIs with their BBVA API Market. They first laid the groundwork by switching their core to a real-time system, and they’ve now rolled out innovative ways to make use of that system via APIs.

For example, they’ve partnered with the fintech company Dwolla to offer real-time payments to BBVA users. In other words, instead of waiting for 24-48 hours for processing via ACH, users of the Dwolla/BBVA Compass partnership can see their money move immediately — even on the weekend.

The key here is that APIs have blurred the lines between these two companies. BBVA highlights Dwolla on their site, and Dwolla highlights BBVA on theirs. In other words, both companies are using APIs in a way that forms a productive union.

As BBVA Compass Chairman and CEO Manolo Sánchez said, “We’ve set our minds on being the best bank in this digital century, and we believe strongly that the best way to get there is to combine our in-house capabilities — our real-time core banking platform, for one — with startups whose very existence is designed to redefine the financial services industry.”

2. USAA / Coinbase

Coinbase enables developers at various companies to add a cryptocurrency component to their application. So far Coinbase has processed more than $5 billion in payments in 33 countries and are set on making Bitcoin and Ethereum easier to understand and use.

USAA has incorporated the Coinbase API to enable their users to send Bitcoin via their products. This marks a major move toward pushing the envelope and taking cryptocurrency mainstream.

Because the concept was so new, USAA started with a test run. Through this process they soon found that the response was better than expected. As project lead Darrius Jones said, “There’s always a gap between feedback and reality. Sometimes highly vocal members who are dogmatic about a capability may or may not represent entirety of the membership. But was this something people wanted.”

As a result, USAA has now opened the Coinbase API to all of their users, locking their company in as a leader in cutting-edge technology.

3. Citigroup / PayCommerce

Citigroup has launched the Citi Mobile Challenge, which enables developers with a wide range of backgrounds to innovate on Citigroup’s core offerings. Developers can retrieve account summaries, validate user credentials, use an authorization token, pull account balance information, find branch and ATM locations, and much more.

The Citi Mobile Challenge offers developers access to three APIs from PayCommerce, geared around cross-border disbursements, global collections, and enterprise payments. PayCommerce connects 80+ correspondent banks in 72 countries with settlement in 80 currencies, and their API offerings position Citigroup (a bank with a very sizeable global presence) to reach a wider audience more easily than ever.

Abdul Naushad, PayCommerce’s founder and CEO, says that their service never takes custody of any money transferred. Specifically, PayCommerce sends the funds straight to the bank’s account for depositing foreign currency. He says, “The money goes straight to that bank’s account, and we coordinate the flow of information to the beneficiary bank in the other country.” Essentially, they send an invoice that lets the bank know what to do in the transfer.

All of this enables Citigroup and PayCommerce to produce something that neither company could do on their own. PayCommerce APIs make global payments via Citi easier than ever, and Citigroup APIs give PayCommerce a much broader reach than they would otherwise have.

The Future of Banking is About Fintech + Banking

As you can see from these three examples, the lines between fintech and banking are blurring as APIs increasingly take center stage. Fintech startups are interested in APIs from banks and vice versa. What’s more, consumers are embracing this unity on a greater and greater scale.

As a result, it’s no longer a matter of whether fintech startups or banks will win a fight against each other. Instead, it’s a matter of which companies will use the right combination of APIs to create something that consumers really want.

Some argue that sharing of APIs may cause an unbundling of the legacy banking industry supply chain, allowing aggregators to select products and services to be reassembled in new ways. While that potential exists, others, like Ron Shevlin, believe traditional financial services firms hold the cards because of their existing customer relationships. He believes that the opportunity for platformification™ is powerful.

Either way, don’t expect fintech companies to dominate at the expense of financial institutions, or financial institutions to dominate at the expense of fintech companies. APIs are creating a third way. An amalgamation of fintechs + financial institutions. The API blur.

That is the future of banking.