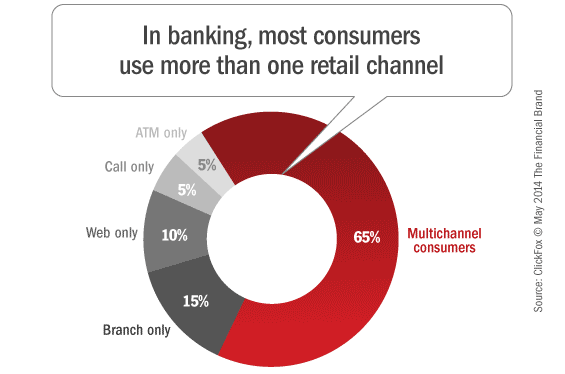

The rise of ATMs, debit cards, direct deposit, online and mobile banking means that most banking customers don’t have the need to go into a branch like in the past. In fact, according to a study be McKinsey in 2014, 65% of consumers interact with their financial institutions through multiple channels, with only 15% using the branch alone. While this shift has provided more convenience and efficiency for the customer, banks are losing a valuable touch point with their audience.

Since the consumer is able to do most of their everyday transactions on their own, when they do come into the branch, it means there is an issue, question or need that hasn’t been adequately addressed within the everyday banking channels. In fact, this creates a real opportunity for a branch to be a problem-solver and foundation-builder for the consumer, but it also means that the level of expectation and expertise needed to address all of a customer’s needs is quite high. Thus, the rise of the universal banker.

Building the Universal Banker

A universal banker is a bank or credit union employee who is trained, capable, flexible and prepared to provide both customer service functions and higher-level counsel to consumers, addressing numerous requirements simultaneously. And in today’s fast-paced, get-it-now environment, universal bankers must be nimble, knowledgeable and respectful of the consumer’s valuable time. The universal banker’s world is where skill and training meet efficiency and competence.

“The universal banker’s world is where skill and training meet efficiency and competence.”

The best cross-trained employee must not only have preparation and skill, but comprehensive tools that can maximize engagement with customers in a bank environment intentionally designed with both form and function in mind. One of the most powerful tools at the universal banker’s disposal is the tablet. This one device brings together multiple pieces of information into one place, where the customer can directly interact with all of a bank’s products and services, alongside a knowledgeable partner who can help guide them to the most customized solutions to their financial needs.

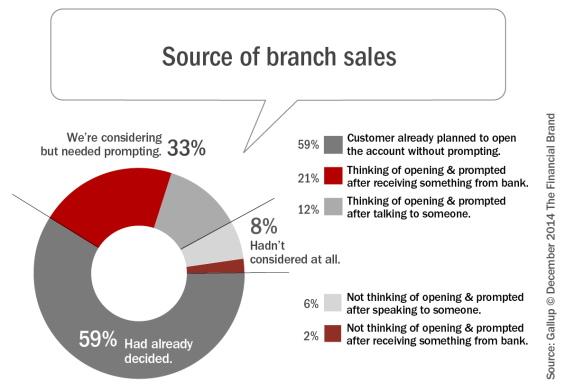

According to a Gallup U.S. Retail Banking Survey, 33% of new accounts were opened in branch by customers who were considering it but needed prompting, and 8% were opened by customers who hadn’t considered it at all. An additional 13% had considered opening an account or buying a service, but did not. These scenarios represent pivotal opportunities for the universal banker to deliver on-point advice and relevant options that speak directly to that customer’s situation.

The same survey highlights the differences between satisfied verses engaged consumer. 45% of satisfied consumer said they would consider their bank or credit union the next time they needed a product or service, yet it increased to 83% among consumer who were both satisfied and engaged. Additionally, engaged consumer were more likely to open a new account, add new products and services and/or obtain planning advice than those just satisfied. But how can bankers and credit union employees do that when they may not really have a direct personal connection? That’s where technology can help.

In today’s competitive banking atmosphere, developing a relationship with the consumer is the lifeline of a bank’s marketing efforts. People buy from those whom they think understand their needs and concerns. A banking consumer is looking for customized solutions made just for them – products and services that speak to their issues and solve their problems. Embracing technology tools can help ensure that there is no disconnect between a consumer’s expectation and a bank’s delivery, helping to facilitate conversations and allowing the consumer to directly interact with solutions tailored for them.

Top Digital Tools for Engaging Experiences

Digital Data. Digital data is only useful when used meaningfully. More than just stat tracking a consumer’s banking balance and activities, it can provide a snapshot of their financial lives that moves along with them. Useful digital data systems like Customer Relationship Management (CRM) allow bank and credit union employees to know information about a consumer, even if they’ve never met face-to-face. For example, a banker can see when a customer carries a high balance in a checking account and how they may be better served putting some that money in a higher-yield instrument like a CD or a Money Market account.

CRMs and similar types of flexible digital data platforms get smarter with time. So while they may begin as lean document tracking through transactions, they grow to become a robust interface through every interaction. This allows the universal banker to make meaningful recommendations that respond and adapt to the consumer’s changing circumstances.

Digital Collateral. Another item that is a must-have for the universal banker is digital collateral. Every industry, including banking, has undergone a revolutionary process of shifting away from a paper-based business model to a digital model. Instead of handing a consumer brochures and documents that outline benefits of an organization’s products and services, having them in a digital format that can be easily accessed and stored in a customer’s CRM and sent to them digitally fulfills the consumer expectation for on-demand information they can interact with and access any time, on any device.

The purpose of digital collateral is to generate awareness. It gives the universal banker an opportunity to display products and services and showcase consumer options and benefits. These tools can assist in selling, serving as a sales-aid to create and deepen conversations with consumer through education and interactivity, which can finally drive action. This can be in the form of opening account, purchasing a product or service or a customer email for trackable follow-up.

Digital Presence. Having updated digital collateral doesn’t just mean scanning in brochures, however. All of a financial institution’s materials must also relate seamlessly with the institution’s digital presence. Just as consumers have an experience when they walk into a bank or credit union office, they also engage with a brand digitally. Does the organization’s website provide fresh content that’s relevant to a consumer? Is it easy for him/her to get what they want? Does it provide the latest research and data in the financial industry? Can the consumer easily find a way to take action?

A financial institution’s digital presence is built from the ground up. It develops from the numerous touch points that the consumer has with their financial institution. Put simply, it is how a consumer experiences a bank or credit union brand – not what the organization wants to say the consumer, but what the consumer wants to hear from their banking organization. A financial institution’s digital identity is how the organization delivers on its customer’s or member’s expectations. The best way to achieve a cohesive, organic identity is to know who your customer or member is, ask them what they want, listen to what they say, and develop products and services that speak to them around their needs and expectations.

Today, nearly everyone has a powerful mobile device at their disposal at all times. Access to technology is ubiquitous – we have what we want, right at our fingertips, almost instantaneously. Banking consumer who do come in to the branch have often done their homework before venturing inside. For a universal banker, it’s up to them to stay ahead of the curve. When the consumer comes through the doors, the universal banker is expected to quickly analyze the consumer’s needs, access their financial data and provide answers and solutions on the spot.

When using a tech tools, the universal banker is sharing their expertise through up-to-date research and information which consumer relies on to make informed-decisions about their personal finance and clear ways to act on their options. This level of engagement expedites decision-making and fosters trust, which is the key to relationship-building. Rather than technology standing between the financial institution and the consumer, embracing the transformative power of technology will actually deepen relationships with consumers.