Branch banking is changing fast, but the proliferation of industry concepts and buzzwords has muddied the waters greatly in recent years. In a white paper entitled, Why a Branch Refresh Isn’t Just About Superficial Design, five core elements of the new banking branch model have emerged that should be present if the branch is to succeed. These are:

- Dialogue towers and cash recyclers.

- Branch staff trained as Universal Bankers.

- Value added products and services; ITM’s, financial consultancy, omnichannel focus.

- Enhanced branding and merchandising.

- Technology bars, café-lounges and learning spaces.

Note that superficial design components are not among these elements. Industry decision-makers selecting a builder for a branch renovation must avoid making the mistake of basing design criteria on cosmetics; it’s not a design competition, it’s an opportunity to incorporate deeper functions that will save your institution money, enhance the customer experience, and increase operational efficiency.

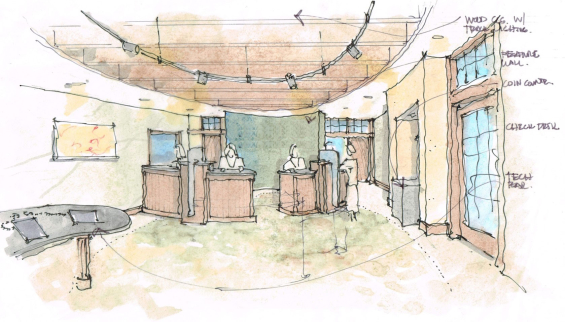

1. Dialogue Towers and Cash Recyclers

The benefits of installing dialogue towers go beyond just the appearance of the towers themselves. While the more open design allows the Universal Banker to come from behind the tower to greet customers, dialogue towers also enable deeper customer engagement. The power of dialogue towers is amplified when combined with cash recyclers.

Cash recyclers have brought an unprecedented level of secure cash handling to the banking world. They’re inconspicuous and are designed for enhanced security. Certified built-in safes mean the cash can be stored inside overnight with no external vault required.

Positioned in the center of the pod between the dialogue bankers, recyclers can process 10 notes per second (dispensed or deposited) in any combination of denominations. They can also log serial numbers for advanced error recovery. Their capacity can be as high as 17,100 notes, with continuous fast processing of large banknote deposits uninterruptedly.

Cash recyclers contain tamper-proof cassettes that are fully secure and can be organized by denomination. Recyclers can count, organize, bundle and strap cash at remarkable speed.

This relatively new technology frees up the dialogue banker, whose attention can now be directed at the customer. Dialogue towers allow engagement banking at its finest, where the branch employee – once chiefly preoccupied with counting cash – can now participate in deeper interaction, providing the key differentiator that drives brand loyalty, enables cross-selling and up-selling, and attracts new business.

2. Integrating Universal Bankers

Change is not easy. Such is the case with the integration of Universal Bankers, where there is almost universal failure to appreciate the time required to acclimate current staff to new the ‘universal banker’ role. Change management specialists and specialized training courses are the two chief tools available to financial institutions that are serious about adopting the Universal Banker model, but it’s recommended that any consultant or training course is properly vetted before sign-up.

Insight into the timeline, attitudes, and available solutions to mastering this sometimes difficult transition are discussed in the Why a Branch Refresh Isn’t Just About Superficial Design white paper.

3. Value-Added Products and Services

The ability to provide value-added products and services is possible only when branch staff is educated enough to speak to the multifaceted nature of the Universal Banker role. These value-added products and services include everything from ITM’s (replacing or augmenting teller functions), an enhanced in-branch consultancy functionality, and an omnichannel experience that ties these capabilities together.

The new branch model increasingly incorporates automated transactions and image capture deposit, with private consultation booths/offices, and roaming Universal Bankers. The objective is to combine both digital and human resources for the highest possible ROI.

4. Enhanced Branding and Merchandising

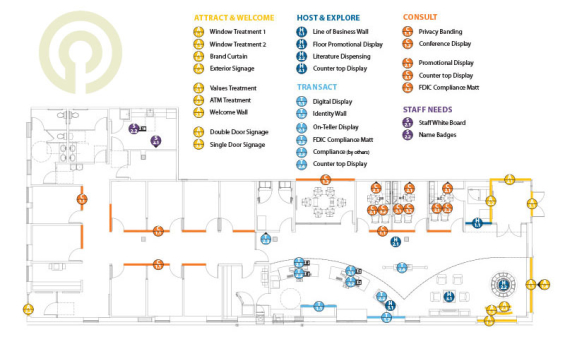

The merchandising and branding elements required in a modern banking branch are an exercise in ‘shopping science‘ rather than simple interior design. Branches have to create retail environments built around specific touchpoints determined by customer experience maps.

Data from large sample sets inform these maps, with all stages of the customer journey being transposed on the branch floor plan to form a holistic picture. This is a powerful in-branch marketing tool used most effectively by industry professionals. The current industry trend towards modernization and rebranding efforts means things are more competitive than ever, and professional advice must be taken when designing the customer journey.

5. A Page from the Apple Store Handbook

Technology bars (and even beverage centers) are powerful lead-ins to deeper community engagement. Self-service, semi-automated branches where visitors can charge and/or use mobile devices and enjoy a relaxing beverage are difficult to compete with if you’re a large legacy branch with excess space and large overhead.

Café-style smart branches complement the consultative element and meld with an omnichannel strategy perfectly. Customers or members can enter themselves into consultancy waiting queues, check finances, and generally move about between whatever channels your institution offers them.

Branch staff can also be alerted to the presence of prime customers when they enter the branch, thanks to beacons that can support the interaction between the person’s mobile device and digital devices in the branch. This increased online activity enables financial institution to harvest more customer data than ever before.