The digital revolution is changing the daily lives of all consumers. No place is this more evident than in the way people bank. ATMs, telephone, online banking and mobile banking are transforming customers’ banking experience, enabling consumers to bank where and when they want.

As was the case with ATMs decades ago, consumers prefer the convenience of new technologies, combined with the assurance of a local branch. Despite this affinity for branches, the economics of yesterday’s branch don’t work.

The number of branches as well as the size and function of remaining branches must reflect today’s digital distribution realities. What is required is a ‘bricks + clicks’ model, significantly reducing the number of branches and digitizing the back and front office of remaining branches with a mobile-first perspective. Advanced ATMs and Universal Bankers need to replace traditional tellers, and remote advisory services need to be supported.

The Digital Banking Report entitled, ‘Bricks + Clicks: Building the Digital Branch,’ provides an in-depth look at how banks and credit unions are changing branching strategies to reflect consumer needs and today’s digital capabilities. Written in conjunction with Jeanne Capachin, this report provides insights into how financial institutions worldwide are integrating digital technologies with human interaction. The overview of new technologies, case studies and best practices is intended to help stimulate thinking beyond todays norms.

According to the report, branch distribution in the future must include these 5 digitally-enabled strategies:

- Improve Distribution Efficiency

- Close and Move Branches

- Reduce Branch Footprints

- Increase Digital Integration

- Improve the Customer Experience

Improve Distribution Efficiency

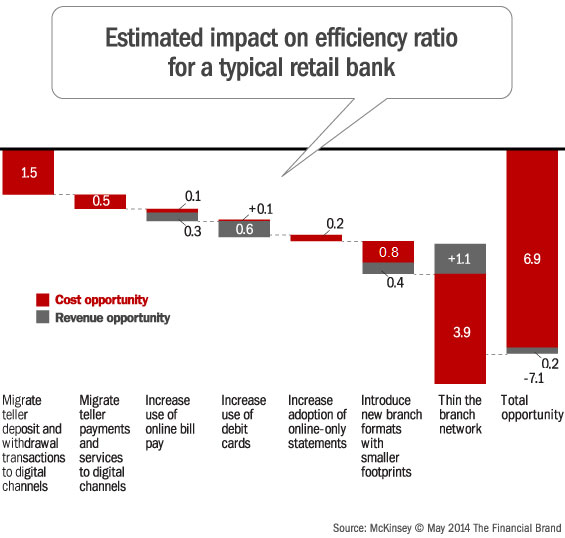

One of the biggest impacts of moving to a more digital delivery of services is the potential for an improved efficiency ratio, or the cost that is incurred for every dollar of revenue that is produced.

Using digital technology to automate both back-office and customer-facing processes – taking work that is currently done in a very manual and error-prone way and digitizing these processes – can eliminate large components of the cost structure including branch-based costs. It can also positively impact revenues across the board.

According to the director of McKinsey’s New York office, Somesh Khanna, “I can imagine us about five or ten years from now talking about efficiency ratios in the low 40s or high 30s (in banking). The value at stake is quite substantial. Between a 30-percent plus and a 20-percent minus, in terms of value shifts, could be achieved by those that actually adopt and embrace high-quality digital strategies early, versus those that don’t.

As can be seen in the chart below, the greatest impact on the efficiency ratio is achieved by closing branches. This is despite a potential reduction in revenue opportunities caused by this reduction (negative impact of 1.1). The next two important strategies that can improve a financial institution’s efficiency ratio are a continued migration of basic transactions to digital channels (mobile and online) and the reduction of branch footprints.

Close and Move Branches

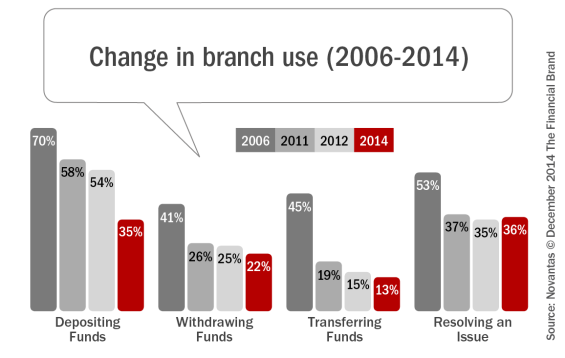

Aided by advancements in digital technology, the reduction in tellers, the introduction of mobile deposit capture and consumer lifestyles overall, branch transactions have been falling precipitously. According to the Novantas Multi-Channel Preferences Study, 70% of checking consumers said they’d prefer to make deposits with a teller in the branch in 2006. As of 2012, the percentage had dropped to 54%, and as of 2014, the preference for making deposits at a teller stands at 35% … a 50% reduction in preference for live tellers in eight years. Similar decreases have been seen with branch withdrawals and transfers of funds.

“Investment in technology has accelerated the shift in the consumer mindset from branch dependence to perceived branch convenience. The knowledge that a branch exists provides a necessary level of comfort, but consumers prefer to transact with their bank or credit union from the comfort of their home, office or on the go,” says Chris Musto, Managing Director of Novantas. “In the coming years, virtual channels will be able to accommodate not only basic banking transactions, but also increasingly complicated service issues, and this will lead to a further drop in branch attachment.”

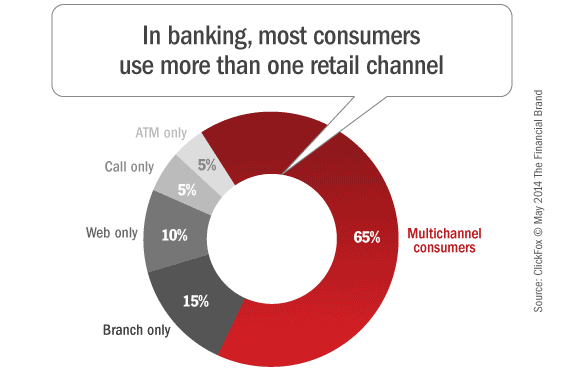

The challenge is that instead of moving completely away from branch transactions, customers using mobile and online banking more than once a week are still over 60% more likely to be active retail branch users than those who do not, according to a McKinsey & Company research study entitled, The Future of U.S. Banking Distribution. This may be a case of ‘We have built them, so they will come.”

The reality is that this branch usage no longer supports the number and size of branches available today. Many of today’s branches were built in the 1980’s or before, when the vast majority of consumers had to visit a branch to get cash, deposit a check and/or make a payment … usually weekly.

“The biggest risk facing traditional banks is the distribution and cultural bias towards physical branches. The process of unwinding this investment is extremely difficult due to the vast scale of branch networks.” – Brett King

These offices are often standalone offices, that include 7-15 teller stations, double or triple drive-through windows, multiple new account desks and a safe deposit box area. Despite their functional obsolescence, the vast majority of these branches remain open and underutilized today. According to many banks highlighted in the Digital Banking Report, these oversized offices of yesteryear are a significant drain on profitability.

Doing nothing with today’s branch structure is not an option in an environment where costs need to be reduced and the customer experience needs to be improved. An effective distribution strategy in the future includes closing branch offices. Remaining offices will most likely need to be moved to higher traffic locations and right-sized for their future purpose.

Reduce Branch Footprints

“By reducing the size of the branch footprint alone, organizations have been able to reduce the cost of distribution by 40-80%.”

— Peak Performance Consulting Group

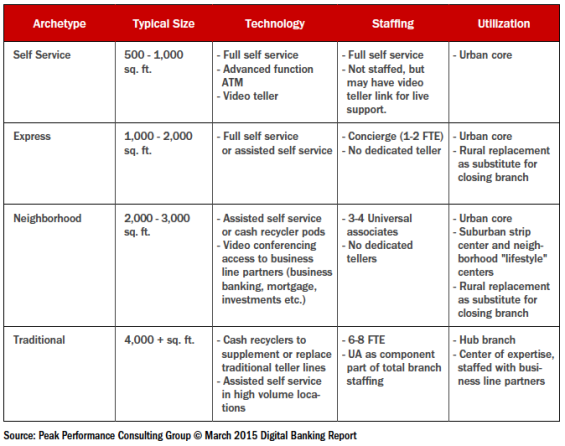

In 2014, the average branch size remained at 3,000 square feet, with a cost of over $2M to build and equip. It is expected that the average size of a retail bank branch will soon be 1500 sq feet, according to research by Oliver Wyman. This shrinkage will occur as larger branches are closed and remaining branches have a reduced footprint. As is shown in ‘Bricks + Clicks’ Digital Banking Report, most branch functions can be achieved is spaces that are significantly smaller than 1,500 square feet.

However, the change in square footage is only part of the story. Most banks will likely need to adopt a hub and spoke approach, with far fewer full-service branches supporting fewer fully or partially automated branches.

At a recent conference, Peak Performance Consulting Group led the session, Transforming Branches – And the Branch Network, where they shared the alternative formats that branch organizations are gravitating to. It was shown that by reducing the size of the branch footprint alone, organizations have been able to reduce the cost of distribution by 40-80% depending on the size of the office and the staffing model implemented.

By reducing the size of the individual units, institutions may find that they can access new locations that couldn’t support a full service branch, and in other cases replace full-service branches with less expensive models. This may bring rise to the question, what defines a branch? Is an unattended location with video tellers that can do everything a live teller can do, a branch or an ATM?

Umpqua Bank has been working from a hub and spoke approach since 2007, and they have one of the most mature approaches. They divide up their geographic footprint into quadrants. A single full-service branch, with neighborhood branches in satellite locations, supports each quadrant.

The neighborhood branches are placed in high traffic areas and are about half the size of the hub branch. These neighborhood branches can be constructed very quickly – just 45 days, with a cost that is half as much as a flagship branch. Umpqua doesn’t skimp on technology though – with digital walls, cash recyclers, video conferencing, and tablets along with location specific amenities.

While Umpqua is often the poster child for next generation branch experience, Chase, Bank of America, PNC and other national brands are also pursuing the hub and spoke network approach. PNC and Tangerine (formerly ING Direct in Canada) have even tested Pop-Up branches.

Other banks, such as Barclays have built completely self-service branches. These self-service locations include traditional ATMs, video teller machines, and digital walls to reinforce the brand. They are open 24 hours a day, without a staff, and with a footprint (and cost) that are much smaller than a traditional branch.

Increase Digital Integration

With significant numbers of branches projected to close and branch visits becoming less frequent, these encounters must become more valuable and more interesting. Instead of first encountering lines of sterile teller windows, consumers entering branches today are likely to be greeted by a concierge or digital sign that steers them to the appropriate bank employee.

Some banks and credit unions are also encouraging visitors to access websites or check their email using Internet connected tablets and computers that help create a more casual atmosphere. Another change in branches is the extensive use of digital signs to promote interest rates and other financial products.

Much of the branch software that exists today is staff-based, supporting traditional transaction processing, account opening, and customer service. Going forward, the software needs to change, mimicking many of the digital innovations already in place for mobile and online banking engagement, such as digital account opening, digital onboarding and proactive recognition of a consumer’s relationship and future needs.

Beyond hardware improvements, such as advanced technology ATMs, video tellers, branch-based tablets, cash recyclers and digital signage, branches need to integrate digital workforce management for internal resource optimization and digital schedulers for customers, where appointments can be pre-arranged. In addition, the potential for leveraging iBeacon technology at the branch level provides potential.

Finally, the biggest change in digital integration may be in how organizations leverage analytics to maximize the value of in-person interactions. For starters, institutions are investing in analytics to evaluate sales performance and provide a metrics-based approach to branch locations and staffing.

For example, analyzing community characteristics will determine the need for financial advisors, business bankers, and lenders at each location. Analytics will also ensure that these employees have the tools they need to be effective. Sales effectiveness tools will be used to marry data and analysis to meet compliance requirements, guide conversations, and suggest products. This will be where the power of branch-based digitalization could most impact the customer experience.

Improve The Customer Experience

Digital capabilities are completely changing the customer experience across industries. With greater insights into customer transactions, the channels customers use and even where the customer is at any point in time, there is the potential for a highly custom and personalized experience.

Banks and credit unions are already working hard to personalize the customer experience during online and mobile interactions. The most progressive institutions are also personalizing interactions with branch tellers, branch platform personnel as well as during and after historically paper-based processes such as new account opening, onboarding and relationship expansion.

By showing the consumer that you know them, will look out for them, and will reward them, satisfaction will increase as will cross-sales and loyalty. Similar to how the book industry, music industry, movie industry and airline industry have transformed their businesses from an in-person, tactile experience to one of almost complete automation, so must the banking industry.

What’s exciting is that by digitizing the way consumers do business with their bank or credit union, and by learning from every consumer interaction, service levels will improve as will sales effectiveness in and out of the branch.

Outlook For The Future

There are lots of different paths a branch transformation process can take, and you’ll need to find the right approach for you and your customers. A great place to start is with your brand and what you want to communicate to your customers and prospects.

Consider what expectations you are building with your online and mobile experiences and how your distribution strategy fits into this model. Remember, you need to have a strong online and mobile offering before you remove your physical presence.

But, waiting and hoping things will stay the same in not an option. Despite lagging branch data from the Fed and consumer preference surveys that are biased and poorly structured, the consumer is moving at breakneck speed to embracing digital technology and replacing traditional branch visits with mobile and online interactions.

Consumers may say they desire a banking storefront nearby, but they definitely don’t need a standalone facility with multiple in-branch and drive-up teller windows. They will also eventually prefer meeting advisors either using in-branch 3D interactive devices or while sitting at home with their interactive TV.

Investing in your overarching digital strategy while closing, shrinking and digitally enhancing today’s branches is imperative. If you don’t invest in a revised distribution strategy now, you’ll be as out of step with your customers as a 1970s branch.