New research from Celent reveals that banking providers are failing to get the customer experience right, as they rush to remap their retail delivery strategies and ramp up digital channels. In the study, smaller banks and credit unions posted significantly higher Net Promoter Scores (NPS) than big banks, despite lagging behind in digital channels. For the time being, a superior branch experience is giving community-based banking providers an edge over their larger rivals, but that advantage is tenuous. Today’s strength could quickly become tomorrow’s liability if smaller institutions don’t up their game and overcome their digital CX shortcomings.

Celent points out that all the advances in mobile banking to date have related to transactions, and that the kind of true digital engagement you get from Amazon and others has been missing in the U.S. banking sector. Even as more and more banking transactions are handled digitally, the fact remains that many consumers still use branches to get questions answered, open accounts, get loans, and more. This has led to a situation where branch-centric consumers are most satisfied, even though they represent a segment in decline, while digital-centric consumers are least satisfied, though growing in number.

Celent’s research proves that “omnichannel”— the ability to serve anyone with the same data and a comparable experience in whatever channel they choose — is more important than ever. When it comes to the debate about branches vs. digital channels, it’s not an “either/or” decision — it’s both.

“This is not a debate over high tech versus high touch,” says Celent analyst Bob Meara. “Both are imperative for institutions seeking to deliver excellent customer service.”

Why Smaller Banks Are Winning… For Now

Net Promoter Score (NPS) uses a single question with a 10-point scale to gauge the loyalty of customer relationships: “How likely is it that you would recommend us to a friend or colleague?” Those who score a 9 or 10 are called Promoters. Those who score between 0 and 6 are Detractors.

NPS is calculated by subtracting the percentage of Detractors from the percentage of Promoters. NPS can be as low as -100 (everybody is a detractor) or as high as +100 (everybody is a promoter). Any positive NPS is good, while an NPS of +50 is excellent.

A key finding in Celent’s research is that people banking with smaller institutions are substantially more likely to recommend their bank or credit union to a friend or colleague than customers at larger banks. Why? When it comes to the in-person experience, smaller financial institutions perform better across every dimension Celent measured.

“Over and over and over again, small banks and credit unions win the day,” said Meara in an interview with The Financial Brand.

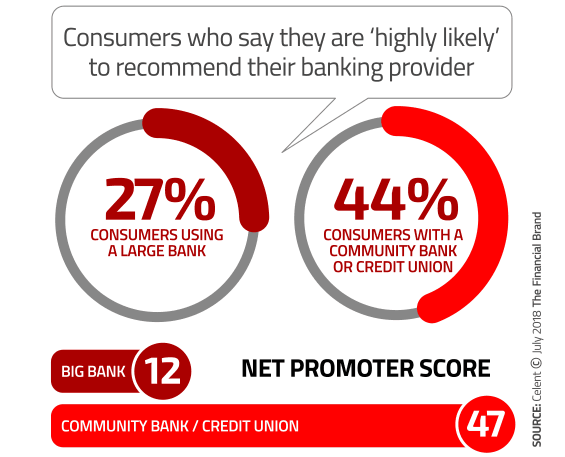

44% of those at smaller institutions said they were “highly likely” to recommend their banking provider vs. only 27% at bigger banks, resulting in substantially higher Net Promoter Scores — 47 vs. 12. Customers of the top five banks gave their institutions even lower NPS, ranging between -8 and 4 in Celent’s survey.

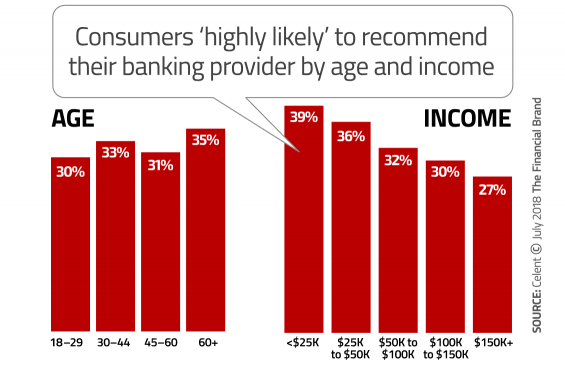

Celent’s report, “Delivering Excellent Customer Service: Why Digital Engagement Will No Longer Be Optional,” further explores how Net Promoter Scores vary by various demographic segments: age, geography (rural, suburban, urban), and income.

These findings puzzle Meara.

“How can community banks and credit unions have significantly higher net promoter scores when they offer a poorer digital experience?” he wonders aloud. “Clearly larger banks put a disproportionate amount of R&D into digital. So why isn’t that moving the needle?”

Ultimately he concluded there are two reasons.

- Problems With Personalization. Consumers understand that their banking provider knows a lot about them, but that knowledge isn’t reflected in how they communicate in digital channels. By comparison, at companies like Amazon, it is very obvious not only that they know a lot, but they adroitly use it to present relevant, tailored and contextual messages.

- Demographic Profiles and Channel Preferences. Meara says it’s easier to offer “a better banking experience” to those who are less digitally involved (and thus have lower expectations). That describes the average rural consumer — who often prefers branches over digital — compared with the typical urban/suburban/higher-income consumer.

Banking providers everywhere — but particularly larger banks — have struggled with personalization in digital channels, said Meara.

“It’s hard to deeply personalize an offer or communication at scale,” he said. “It is much easier to do that at smaller banking companies where they actually know many of their customers.”

For now, small banks and credit unions may have the NPS advantage, thanks to their branch experience. But will it last? Celent’s research suggests that it won’t, without significant effort.

“Banking providers can’t deliver excellent customer service just relying on a single channel,” Meara explains. “For the overwhelming majority of consumers, this means their financial institution must execute well both digitally and in-person.”

Read More: New Study Shatters Myth That Digital Channels Are Killing Branches

Digital Customers Less Satisfied

According to Celent, financial institutions need to pay particular attention to two categories of consumers: (1) Millennials and other younger consumers, because of the opportunity they represent for lifetime customer profitability, and (2) high-income consumers because of their need for additional products.

The study’s results suggest that many banking brands are at risk with both these important groups. As the chart below indicates, Millennials showed the lowest Net Promoter Score among all surveyed age groups, while the high-income earners — those with annual incomes over $150,000 — showed the lowest NPS among income groups.

Even though Celent’s research found that the likelihood of attrition among banking customers overall is low, Millennials say they are twice as likely to change banks as those over 60.

Older consumers are more branch-centric than younger adults and have the highest Net Promoter Scores, but they aren’t the future of banking. The problem, according to Meara, is that the growing — and most important — segment that prefers a fully-digitally enabled experience yields a Net Promoter Score 20 points lower than those preferring branches. Not surprisingly, these digitally engaged consumers are heavily represented in the Millennial and the 30-44 year-old age segments — the bread and butter for financial institutions.

Celent believes banking providers of all sizes are “blowing it.” Big banks are not keeping the level of personal service in their branch networks where it needs to be, while small banks and credit unions aren’t keeping up with rising consumer expectations in digital channels.

Of the two groups, however, Meara is more concerned that the smaller institutions will struggle to keep up with what bigger institutions are able to do. Large banks have the opportunity to turn the tables if they do a good job at making digital banking more personalized, said Meara.

Regarding the poorer branch experience offered by big banks, Meara said it’s more a question of investment in human capital than technology. On the basis of short-term value for shareholders, he said, it’s hard to justify further spending on the branch model given the rapid shift to digital banking. But if the focus is on improved customer service, then an enlightened bank will invest in both.

“Over-reliance on digital channel investment in the short term would be a huge mistake,” Meara cautions.