It comes as no surprise that banking customers are continuing to migrate routine transactions and interactions to digital channels. At the same time, there has been a rapid shift in online shopping that has altered the marketing and sales funnels for banks and credit unions.

Despite this shift, there is still a segment of consumers committed to the traditional branch for certain activities. According to the Novantas Multi-Channel Preferences Study, the more that the growth of digital adoption and functionality changes channel usage across sales and service, the more things stay the same for some tasks and some customers.

Building on three prior editions of this study, this year’s edition shows that some trends, such as deposits leaving the branch, have accelerated, while others have flattened. The findings support that bank branches remain vital to new primary checking acquisition, but that the optimal branch count and branch experience far different from what most banks and credit unions offer today.

“Investment in technology has accelerated the shift in the consumer mindset from branch dependence to perceived branch convenience. The knowledge that a branch exists provides a necessary level of comfort, but customers prefer to transact with their bank from the comfort of their home, office or on the go,” says Chris Musto, Managing Director of Novantas. “In the coming years, virtual channels will be able to accommodate not only basic banking transactions, but also increasingly complicated service issues, and this will lead to a further drop in branch attachment.”

Branch Shopping Behavior

According to the Novantas study, shopping online is done most frequently by consumers switching primary checking accounts over the past three years, but visiting the branch is the most likely shopping method for those opening a checking account for the first time. In other words, as familiarity and confidence with banking products and services increases, there is a greater likelihood of transition to digital channels.

Across age, income and prior banking experience categories, recent checking purchasers tended to take advantage of multiple methods of shopping for an account, but Switchers were 18% more likely to have shopped online than in a branch, while the Newly Banked were 36% more likely to shop by visiting a branch. Similarly, 33% of Switchers cited online shopping as most helpful, while for the Newly Banked, the branch was cited as the most valuable method, with only 21% citing online shopping as the most helpful method.

![Most_helpful_shopping_channels_for_making_checking_purchases[1]](https://thefinancialbrand.com/wp-content/uploads/2015/01/Most_helpful_shopping_channels_for_making_checking_purchases1-565x377.png)

Interestingly, the youngest (presumably digital native) consumers (18–24 year-old) are most likely to shop through recommendations, followed by in-branch visits and then shopping online. For the 35–44 year-old age group, they are in fact 60% more likely to shop online than to shop by visiting a branch.

“Whether this pattern is driven by the banks making online shopping hard, opaque and complex, or by the nature of self confidence in driving channel choice, it points at the interesting phenomenon that less-valuable customers (younger, earlier life stage) may be more branch-centric in purchase terms than all others, and would potentially turn the ‘affluent branch’ logic upside down,” states the Novantas study.

Branch Usage Behavior

“When it comes to predicting which consumers will use and value the branch, age and income become especially unhelpful … the true differences are attitudinal.”

The Novantas study found that when it comes to predicting which consumers will use and value the branch, segments of similar demographic composition, such as age and income, use and think about branches very differently. In fact, as part of an attitudinal segmentation process done by Novantas, it was found that a majority of consumers (irrespective of age or income) use the branch very infrequently, but still have a loyalty and attachment to the branch.

By looking at the level of ‘branch dependence’ and ‘branch attachment’, Novantas found five segments of branch consumer:

- Thin Branch Ready (rarely use, modest attachment): 39%

- Mass Market (modest use, modest attachment): 29%

- Branch Traditionalist (heavy use, heavy attachment): 15%

- Innovation Seeker (use branch heavily, no attachment): 10%

- Internet Ready (rarely use branch, no attachment): 7%

The composition of these segments differs by institution and there is an opportunity to shift percentages based on branch network positioning. For instance, at Bank of America, which continues to promote mobile banking and has closed offices, 52% of primary checking customers are ‘Thin Branch Ready’. Alternatively, at Chase, which continues to increase its branch count, the percentage of ‘Thin Branch Ready’ is actually in line with large regional banks, at 39%.

The segmentation done by Novantas illustrates that organizations must look beyond traditional demographics when targeting consumers regarding branch use and that there is an opportunity to move market share based on branch strategies.

Trends in Banking Transactions

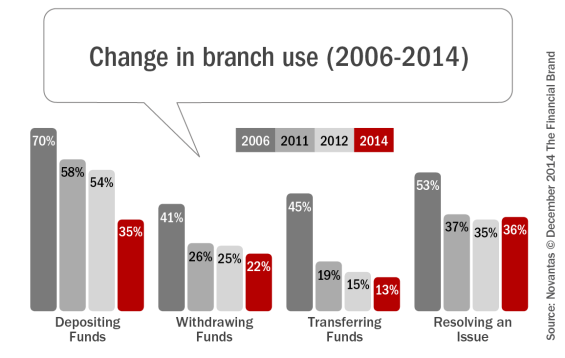

Even with differences in behavior and attitudes regarding the branch, consumers as a whole use the branch for fewer transactions every year. But this trend is far from constant across transaction types, according to Novantas.

Aided by advancements in digital technology, the reduction in tellers, the introduction of mobile deposit capture and consumer lifestyles overall, branch deposits have been falling precipitously. In 2006, 70% of checking consumers said they’d prefer to make deposits with a teller in the branch. As of 2012, the percentage had dropped to 54%, and as of 2014, the preference for making deposits at a teller stands at 35% … a 50% reduction in preference for live tellers in eight years.

On the other end of the spectrum, when it comes to resolving an issue, the rate of preference for the branch is down only 30% in eight years, from 53% to 36%. Interestingly, the preference has remained the same since 2011.

What has changed is that consumers are increasingly preferring to move call center issue resolution to the online channel. In 2011, the phone channel was the most popular channel for issue resolution (49%). Now, the call center preference is at 34%, behind the branch (36%) and ahead of online channel resolution (23%).

According to Novantas, “Branches have gone from being significantly more preferred for making deposits than for resolving issues, to equally preferred for both. It’s not just overall activity in the branch that’s changing; it’s the mix and the role: Sales and problem resolution, not withdrawing, depositing or transferring funds.”

When viewing the value of the branch in the eyes of the affluent consumer, while the Internet Ready segment is disproportionately affluent, the affluent are not, for the most part, attitudinally ready to leave the branch completely behind. That said, they are still less likely to prefer the branch than other consumers. So, while a bank branch may help the bank brand itself with the affluent, it is becoming less helpful in serving them.

Recommended Branch Banking Actions

Branches still play an important role in banking, especially with specific segments of consumers and during the process of new account opening and with issue resolution. But as the defining purpose of branches is changing, the structure, penetration and business case for branches must adjust accordingly.

To adapt to this continuing shift in customer preferences, Novantas recommended that banks take several actions:

- Bank marketing programs need to recognize the decreasing importance of the branch in the overall sales process and utilize out-of-home advertising, market-specific digital campaigns and other channels that will reach consumers who won’t begin their purchase process in a branch.

- Banks and credit unions will need to support digital channel awareness and consideration and provide the option to open accounts online or by visiting the branch. These efforts should most importantly be focused on the Thin Branch segment.

- Organizations need to support a multichannel experience including both digital and branch fulfillment. This may mean aligning the experience and the product presentation, simplifying the opening process and aligning incentives and attribution measurements to foster collaboration between the digital and branch channels.

- Banks and credit unions must move beyond ‘basic mobile banking’ offering experiences that are simplified and differentiated.

“The traditional distribution strategy relied solely on branch dominance, but as preferences shift to online channels, banks need to adjust their spending and strategy accordingly,” comments Kevin Travis, Managing Director of Novantas. “Banks must be fully capable of effectively handling customer service and sales issues at every touch point. And, more importantly, banks need to ensure positive experiences as customers move from consideration to fulfillment — no matter what combination of channels are used in the process.”