Over the years, we have heard financial industry experts claim that the demise of bank branches is imminent. Equally qualified consultants argue that financial institutions should increase the investment in brick and mortar facilities to better meet the needs of the ‘phygital’ consumer who uses both physical and digital delivery channels.

Unfortunately, as it is with a lot of research, organizations can often find survey results that support their predetermined direction. If your organization wants to double down on the investment in current branches, there is a ton of insight that appears to reinforce this decision. There is an equal, if not greater, amount of research supporting the closing of branches and increase in investment in digital functionality.

How can both sides of branch/digital argument be right?

First of all, and most importantly, there is no single right answer. The decision to invest more in branches and/or digital channels must support overarching strategies that take into account current competitive positioning, product offerings, technology and back office infrastructure, target audiences today and in the future, and your organization’s leadership and appetite for cultural change.

But in making your decision around investment in channel support, you must be cautious about good research that may lead to poor decisions. In other words, a lot of very valid research can be misinterpreted because of outside variables that are impacting the results.

Below are some examples of some branch metric myths.

Read More: Do the Majority of Americans Really ‘Want’ to Use a Branch?

1. ‘Branches are Essential’

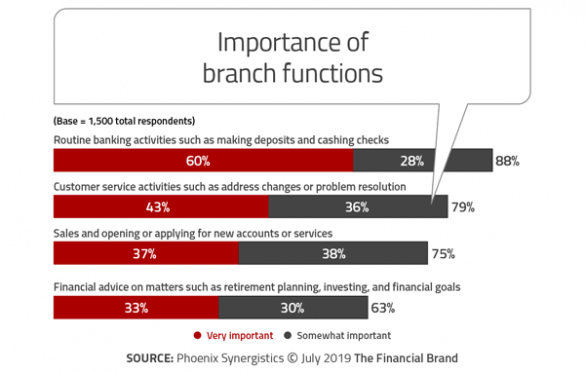

According to the study from Phoenix Synergistics, “The New Digital Bank Branch,” half of consumers report bank branches were ‘essential’ to how they handle their banking. Baby Boomers were most likely to hold this viewpoint, with two in five Millennials also finding branches essential for their banking. Overall, more than one-third indicated branches were ‘important,’ but not essential. Only a very small percentage of consumers found branches ‘unimportant’.

Phoenix Synergistics found that consumers primarily see branches as transaction facilities. Going forward, they believe branches will need to become more proficient at being service, sales, and advice centers. Phoenix agrees that this transformation will not be easy.

Counterpoint: There is no reason to doubt that consumers (including Millennials) believe branches are essential. But two major questions remain: 1. How often are branches essential, and 2. Does the financial institution make branches essential by not providing a viable digital alternative?

For instance, the top three reasons consumers said branches were essential are: daily transactions, routine customer support activities and opening new accounts. Many banks already have the capability to complete these transactions without branch engagement. So, the issue becomes consumer education around this functionality.

Unfortunately, not every financial institution supports these activities digitally end-to-end. For instance, several banks and credit unions have highly restrictive limits to the amount that can be deposited via mobile deposit capture functionality. In addition, most routine customer support functions are virtually invisible on both a mobile and online app.

Finally, according to the Digital Banking Report, the vast majority of financial institutions still can not support digital account opening without a subsequent visit to the branch. In other words, the use of a branch is only truly ‘essential’ because digital options are either unknown, invisible or impossible.

Read More: True Digital Account Opening Totally Eliminates Need for Branches

2. ‘Consumers Love Branches’

While there is no argument that branch visits by consumers have consistently declined over the past decade, a majority of consumers continue to visit branches on a monthly basis (albeit not as often and not always by choice). In addition, Millennials also tend to use branches for a wide range of activities.

The question is, do consumers love going to branches? There are many studies that will confirm and refute this finding, and much of the research depends on what organizations are studied.

For instance, the New Digital Bank Branch report from Phoenix Synergistics found a positive correlation between more frequent branch visits and a higher net promoter score (NPS). This should be expected since more loyal consumers tend to frequent their financial institution more often. Does this mean that consumers love branches?

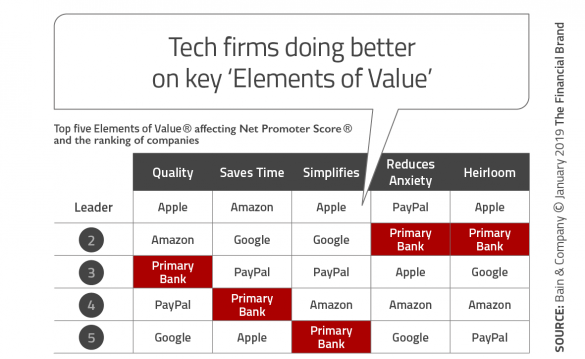

Counterpoint: In banking, companies that perform well on four or more “Elements of Value” have, on average, more than twice the Net Promoter Score of companies with a high score on just one element. In banking, the five Elements of Value that were found to have the greatest impact on Net Promoter Score were ‘quality’ (by a wide margin), followed by ‘saves time’, ‘reduces anxiety’, ‘simplifies’ and ‘heirloom’ (ongoing stability).

Consumers, on average, give their primary bank a lower rating on these elements than at least one of the major tech firms. This indicates that consumers prefer the components of digital banking more than branch banking, plus that traditional financial institutions may need to be concerned about big tech firms foray into banking.

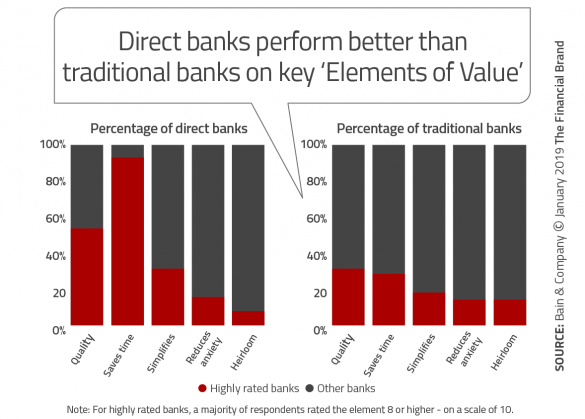

When Bain & Company compared the key elements of value between direct banks and traditional banks, there was a clear distinction between the two types of financial institutions, with the digital alternatives performing better. In other words, when done well, consumers will rate digital alternatives higher than branch-based options.

3. ‘Digital-Only Banks Won’t Succeed’

When I travel globally, many bankers remain relatively satisfied with the number of branches they have and the progress they are making to becoming more digital. The majority are not closing or reducing the size of many branches and have no intention of becoming a digital-only bank.

When asked about their rationale, many will reference the hundreds of fintech firms that have not generated the level of scale required to become a viable competitor in a traditional sense. More recently, they will reference the closing down of the digital-only bank from Chase (Finn) and the continued building of large branches by Chase.

This may be a shortsighted perspective.

Counterpoint: First of all, many current leaders in the banking industry have been in the banking business the majority of their careers. This has the combined effect of providing a vast amount of traditional banking experience along with a limited exposure to how digital organizations compete and succeed.

For instance, few traditional bankers viewed the introduction of Square, PayPal, Venmo or even Apple Pay as important competitors when they hit the streets. This is because the acceptance of these payment options did not explode overnight. That said, nobody can argue with the reality that a large percentage of the payments business has moved to non-traditional players. The same can be said for direct lending, mortgage lending and investment services.

As referenced in the article, “Was Chase Bank’s Digital-Only ‘Finn’ Spinoff a Viable Strategy?”, the demise of Finn by Chase may have been the result of internal politics around the support of a banking option that could displace the traditional banking network as opposed to Finn being a bad strategy.

For a digital-only banking unit to succeed, there must be unequivocal support for a digital banking organization … from the inside out. There must be significant investment in the new entity and the acceptance that the streamlining of operations and cutting of costs will involve tough decisions — including staff displacement.

Caveat Lector (Let the Reader Beware)

Ron Shevlin, director of research at Cornerstone Advisors and contributor-at-large to The Financial Brand, has often referenced the practice of ‘quantipulation’ — defined as the act of using unverifiable math and statistics to convince people of what you believe to be true. While quantipulation is usually not about false data, it does involve leveraging insights to make a point that might have been biased or self-serving.

Bottom Line: For those organizations looking for ‘scientific proof’ that branch networks should expand, remain at the same level or be shut down altogether, the answer lies in the acquisition, retention and growth strategies your bank or credit union wants to pursue.