Many banks and credit unions have a digital onboarding problem that could be costing them dearly. It’s perhaps the biggest disconnect between consumer expectations and the reality of what is being offered.

People have been conditioned to be able to sign up for a new product or service with other businesses with a quick, simple and entirely digital process. For many financial institutions, onboarding — specifically account opening — still often requires coming into a physical branch or location to complete. ID verification and signatures being the two most common steps requiring a branch visit, according to the Digital Banking Report.

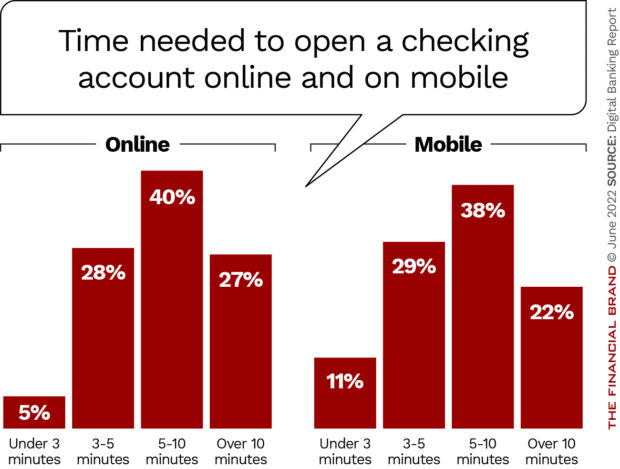

Even for banks that enable some digital steps in the onboarding process, it is still often a subpar experience for consumers. The process simply takes too long compared with what people are used to. (You can test this out fairly simply by opening an Apple Card or Chime account on your mobile phone and see how your institution’s process compares.)

A Key Marketing Moment Is Too Often Missed

An extensive consumer survey by European ID tech vendor Signicat found that 68% of people abandoned the digital onboarding process for a banking product during 2022, up from 63% in 2020. The trend is especially notable with Gen Z, but even people up to age 44 “tend to have a higher likelihood to abandon an application process entirely if it doesn’t work the way they expected,” the company states.

Broad Impact:

After a bad onboarding experience, more than half of consumers are less inclined to use a banking provider again, Signicat data shows.

“Digital onboarding … is a key moment for online financial services,” states biometrics provider Innovatics. “Many marketing investments lead to this point, and failing to successfully onboard all customers at this stage in their journey represents significant [loss of] money.”

Indeed, bank software firm Backbase, writing in ABA Bank Marketing, estimates that retail client acquisition in a physical, siloed world costs an average of $280, while shifting to digital onboarding reduces the cost to $120 and in subsequent years for additional clients to $19.

The Backbase article cites Oliver Wyman research, which found that 30% of prospects who visit bank websites move on to the product details page, and 13% complete a product application. In branches, 85% of customers complete an application. The problem of course is that many fewer people come into branches now.

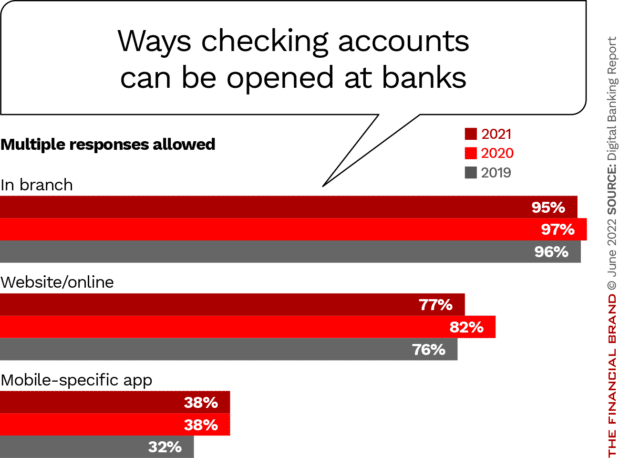

As shown in chart below based on 2021 Digital Banking Report research, the onboarding emphasis at banks is still heavily skewed to the branch.

A BAI report, cited by FintechFutures, notes that three-quarters of Millennials say they would switch banks for a better mobile experience, while even Gen Xers’ appetite to use digital methods to open bank accounts for savings and loans is rising.

Simply put, banks and credit unions that can do digital onboarding right will have a significant competitive advantage.

Read More: Growth Is Impossible Without Faster Digital Checking Account Opening

Areas Banks Can Target to Improve Digital Onboarding

Perhaps the single biggest thing banks and credit unions can do to improve the onboarding process is by streamlining the experience. One way is by allowing customers to initiate the onboarding process from multiple digital channels and third-party touchpoints, says an Oracle blog.

There is opportunity to streamline the process further, however. As the technology company writes: “Post signing-up, customers should not be burdened with cumbersome additional requests. For instance, their personal information must not be requested multiple times across various banking processes.

Instead, the request for information should happen once at the start of onboarding, and then automatically be relayed to other banking processes downstream, saving time and effort for the customer.”

Another key to improving digital onboarding experiences is to adopt re-targeting strategies that address customers who abandon the application process part way through, says Backbase. This can be accomplished by storing the applicant’s details in a customer relationship management, or similar, system and then sending them notifications to complete the application.

Or simply refer prospects to call center employee who can follow up by phone. “Such approaches can boost completion rates by 15% to 20%,” Backbase states.

Read More:

- 5 Ways to Maximize Your Account Opening and Onboarding Process

- Bank Accounts Opened Online Are Less Profitable: How to Change That

- What’s the Future for Checking Accounts?

Turn Regulatory Requirements Into a Plus

A reality of banking is regulatory compliance requirements that add an extra layer of friction to account opening, regardless of whether it’s done digitally or in a physical channel.

Deloitte advises that banks and credit unions turn this into an advantage by letting customers know that these extra steps they must complete to open a checking account — compared to, say opening a streaming service account — are actually beneficial to them.

“In this regard, banks might even want to emphasize it in their overall messaging strategy as a benefit that customers don’t get from less regulated non-bank competitors,” says Deloitte. “At a broader level, banks should communicate that customer security, and not just meeting regulatory demands, is the motive for greater inquisitiveness during the account opening process.”

Banks can also use the information and data they already have in order to enable a quicker and more seamless account opening process.

“Consumers demand that banks use their existing information to not only speed the process up, but also to cross-sell relevant products to them,” Deloitte states. “Delivering a faster account opening experience — especially to young existing customers, who tend to be the most demanding — likely relies on fully exploiting information that the bank already possesses.”

Listen In: Innovation in Digital Account Opening and Onboarding

Finally, one piece of advice can help put traditional institutions in a more competitive position. Don’t compare your process to what your traditional “cross-town rivals” are doing. As suggested earlier, open an account with a fintech or neobank or big tech company. That’s what sets consumer expectations.

Achieving the same speed and efficiency of such providers may seem impossible, but there are many options available now from bank technology providers and fintechs to bring such capability within reach.