Financial marketers usually look at consumers in terms of basic demographic variables — e.g., their age, income or ZIP code. If they were honest, most banking providers would have to confess that they don’t examine their audience in ways that reveal anything truly insightful about people — e.g., their preferences, goals and aspirations. But using behavioral segmentation, marketers can really get to know the prospects they are targeting, and use that information to effectively shape every interaction and personalize the experience in ways that align with people’s needs and expectations.

Don’t get the wrong idea, traditional demographics is still a useful tool to segment consumers, but crude datapoints like age and ZIP code alone won’t tell you why consumers are attracted to a particular product (or not), nor why they choose to do business with a particular bank or credit union (or not).

Most marketers would love to know what makes someone a flight risk. What are the indicators signaling a red flag? To gain that type of insight, banks and credit unions will need to look beyond demographics and categorize consumers by their behaviors, interests, activities and opinions and then use that data to create highly targeted marketing campaigns based on psychographic drivers.

According to the data analytics team at FICO, consumer behavioral and attitudinal data cuts across all demographic segments, providing important insights into payment tendencies, technology preferences and financial goals and aspirations.

“Banks and credit unions can integrate behavioral-level consumer data into every decision and consumer interaction to gain an edge over competitors that depend on demographic data and operate reactively to competitive threats,” FICO explains in a white paper.

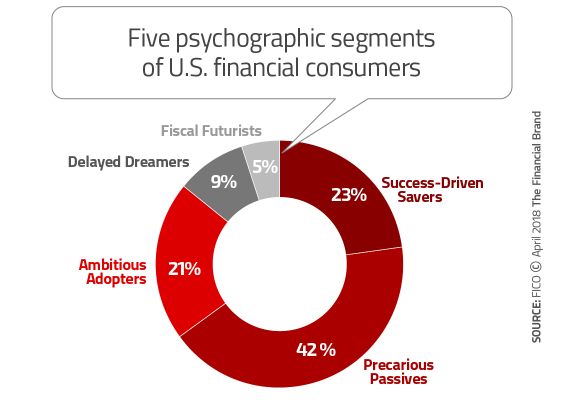

For its report, FICO surveyed more than 1,000 consumers and segmented them into the following five categories based on their behaviors and attitudes toward financial institutions and financial products and services.

1. Precarious Passives

These consumers really don’t care about finance and aren’t particularly hyped up about saving or financial planning. They’re pretty blasé when it comes to banks and credit unions, so it’s a struggle to get their attention. But you can’t just ignore them because they are the largest segment of consumers. Or can you?

These consumers really don’t care about finance and aren’t particularly hyped up about saving or financial planning. They’re pretty blasé when it comes to banks and credit unions, so it’s a struggle to get their attention. But you can’t just ignore them because they are the largest segment of consumers. Or can you?

Strategy – Engaging Precarious Passives will take some work and, according to FICO, the effort may not be worth it. This segment tends to lump all banks and credit unions together and from a practical standpoint, there is little you can do to differentiate your institution. Spend your time and energy on the four other smaller, more engaged and profitable consumer segments.

2. Success-Driven Savers

Confident in their financial knowledge and capabilities, these folks actively manage their financial health, but they are not particularly tech-savvy. They use online tools and mobile apps, but they aren’t tethered to digital. Since they hate credit card debt, they try to — and often do — pay their credit card bill in full each month.

Confident in their financial knowledge and capabilities, these folks actively manage their financial health, but they are not particularly tech-savvy. They use online tools and mobile apps, but they aren’t tethered to digital. Since they hate credit card debt, they try to — and often do — pay their credit card bill in full each month.

Strategy – You won’t wow this crowd with cool technology. They prioritize good old-fashioned excellent service and traditional financial planning tools over digital tools. But because they are hyper-focused on results, they like digital tools and apps that show their progress toward their goals.

3. Ambitious Adopters

Welcome to your future high-value consumers. Younger and tech-savvy, these consumers are up for trying something new, whether an app or product — or a new bank or credit union. They have money and are open to expanding their relationships with financial providers.

Welcome to your future high-value consumers. Younger and tech-savvy, these consumers are up for trying something new, whether an app or product — or a new bank or credit union. They have money and are open to expanding their relationships with financial providers.

Strategy – Open your wallet and get ready to invest in technology. This is the group you do need to wow with your sophisticated digital capabilities.

4. Delayed Dreamers

These consumers, mostly female, love to dream about financial goals like a vacation home or a prestigious college education for the kids, but they are worriers: about their budget, their debt and their perceived inability to save money. They rely on debit cards a lot, even for online purchases, since they don’t trust their ability to use credit responsibly. They check their account balances often and they pay their bills online.

These consumers, mostly female, love to dream about financial goals like a vacation home or a prestigious college education for the kids, but they are worriers: about their budget, their debt and their perceived inability to save money. They rely on debit cards a lot, even for online purchases, since they don’t trust their ability to use credit responsibly. They check their account balances often and they pay their bills online.

Strategy – Delayed Dreamers want financial security, but they don’t know how to get there and don’t trust their own abilities. Educate them about financial literacy and give them automated personal financial management tools.

5. Fiscal Futurists

Young and cocky, they believe they’ve got this financial thing down. The good news is that most of them like their current bank or credit union; the bad news is that they get excited about new financial providers and aren’t afraid to leave their incumbent financial institution for a more attractive offering.

Young and cocky, they believe they’ve got this financial thing down. The good news is that most of them like their current bank or credit union; the bad news is that they get excited about new financial providers and aren’t afraid to leave their incumbent financial institution for a more attractive offering.

Strategy – This is the group that is most likely to believe that in a decade they won’t need banks or credit unions at all. For this segment, your biggest threat isn’t the bank or credit union down the street — or even the mega banks. Your biggest threat is non-traditional providers. And they provide convenience in droves. Focus on creating friction-less and fast offerings to compete with fintechs.

Targeting Millennials and Gen Z

Megabanks are popular with FICO’s Fiscal Futurists and Ambitious Adopters — consumers who tend to be younger. National banks also dominate Gen Z and Millennial segments with credit cards. But remember, these consumers get excited by new products and tend to be more transitory than other consumer segments. Plus, they are wary of debt and want help in managing it.

For these younger consumers, credit cards are ideal gateway products. Community banks and credit unions can keep pace with national banks by developing and marketing entry-level credit cards for Gen Z and Millennials. An entry level credit card can help these consumers build credit while ensuring that they don’t get in over their heads in credit card debt.

Digital account opening is another smart strategy, as younger digital native generations increasingly prefer finding and acquiring products online.

Convert Consumers to Credit

Delayed Dreamers are not confident in their financial management skills and worry that they are not saving enough. The result is that they are more likely to use debit cards instead of credit cards to curb their spending and keep within a budget.

Offer these consumers a credit card with built-in, easy-to-use tools to manage spending and encourage savings.

In contrast, credit cards are popular with Success-driven Savers who are confident in their ability to manage their finances and are most diligent about paying off their balance at the end of the month. Offer these consumers credit cards with benefits such as sign-up bonuses, travel rewards and no foreign transaction fees.

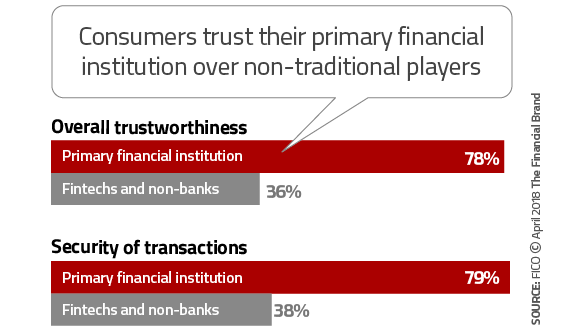

3. Stress Trust and Security

Across all consumer segments, trust and security is of paramount importance. In its research, FICO found that 44% of US consumers are deeply concerned about identity theft and banking fraud. This was more than double those who said their top concern was being the victim of a terrorist attack (18%) and twice the number who were worried about their own death or that of a loved one (22%).

The good news? Banks and credit unions have an advantage over non-bank providers in the area of trust and security.

Most consumers are happy with the way their primary financial institution handles security and rate their trust as high. But community banks and credit unions should look for additional opportunities to capitalize on their competitive advantage by providing additional resources and education, particularly in the area of cybersecurity.

Consumers are not only concerned about the threat of a personal data breach; they are unsure how a breach might impact them. Consumers don’t really understand what a “data breach” is and what it could means to them. If a breach does occur (anywhere, not just at your institution), explain the exact nature of the breach and implement a prepared communications plan to become even more of trusted advisor.