Comparison websites’ role in the marketing of financial products keeps expanding and changing. These websites, which frequently enjoy better traction with Google and other search engines than banking sites themselves, already straddle an unusual range of roles from advisory and rankings for consumers to editorial to paid-promotion for brands. Their increasingly powerful position in digital sales of banking products is now being augmented by another role: direct sales partnership with financial institutions.

Among the better-known financial comparison sites in the U.S. are NerdWallet, Credit Karma, Bankrate.com, WalletHub, The Points Guy, GOBankingRates, The Ascent (a banking-oriented site operated by The Motley Fool), The Balance, and Finder.com. There are also the four comparison sites owned by online lender LendingTree: ValuePenguin, DepositAccounts, MagnifyMoney and CompareCards. There are others, such as FindABetterBank, operated by Novantas, the banking data and consulting firm, and Wise Bread.

All of the foregoing sites are national in scope. There are also sites operated by nonprofit organizations, such as Consumers’ Checkbook, a family of sites that compare banks and many other types of local businesses in seven metropolitan areas, including Washington, D.C., as well as a national edition.

The approaches used by each site, the range of services offered, and the relative reliance on experts’ opinions versus technology versus consumer comments varies. But they have collectively built up the factors that make Google happy — so much that often, when consumers search for online guidance, they wind up on one of the comparison sites first, according to Lierin Ehmke, Senior Digital Marketing Analyst at Comperemedia, a Mintel company.

In a search for “best credit cards,” we saw, in this order, four Google Ads, with one from The Points Guy leading to a page consisting completely of sponsored card offers, followed by similar pages from Credit Karma, NerdWallet, and LendingTree. These were followed, on the first Google page, by some organic search listings, followed by more Google Ad pages.

That first Google search page contained not a single bank or credit union listing, other than a few logos from financial institutions. Clicking on these, with one exception, triggered Google Ads from those brands.

Comparison Sites Have Become Baked-In to Web Marketing

Working with comparison sites in a role beyond simply providing information is called “affiliate marketing,” according to Ehmke. She says that working with affiliate sites is growing increasingly important. Ehmke explains that affiliate sites use strong search engine marketing practices and tactics to ensure high placement for consumers’ searches. Nine out of ten searches for financial help begin on a search engine and consumers will likely spend at least some time on a comparison site before opening an account or applying for credit, she explains.

In fact, Gartner found in a study of major banking brands that less than 20% of their website traffic came from search. The majority of traffic came from customers who already had a relationship with the insititutions.

“Banks lose out on prospect ‘foot traffic’,” the report states, “due to a low share of first-page search results for nonbranded key words.” Among the banking brands Gartner studied, they were found to “only own 19% of organic first-page results for banking keyword searches (e.g., ‘checking account,’ ‘savings account’). With lending terms (e.g. ‘mortgage,’ ‘loan’), that ownership drops to 12%.”

Comparison sites own 34% and 25% of first-page search results for banking and lending, respectively, according to Gartner’s work. The study found that paying for placement is important.

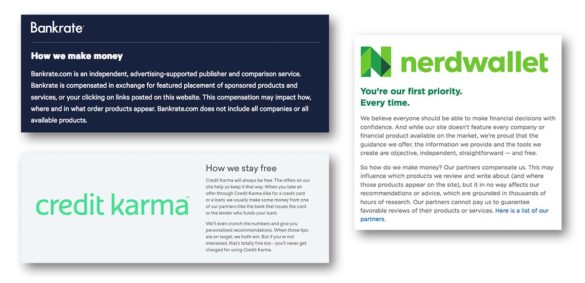

The payments are no secret. Practices vary among the sites, but generally somewhere on each there is an explanation of the way listed providers may be paying for exposure. Sometimes there are fees for more prominent placement, sometimes there is compensation for accounts opened as a result of visiting the site, sometimes compensation is made for clicks, and sometimes sponsored listings are labeled as such. Some pages displayed may consist of sponsored brands only, and are marked as an advertisement, while other sites cover that situation in some other way. There may also be straightforward digital display ads, clearly paid for.

Disclosures frequently run along the lines of the sampling below. The proviso that editorial judgments are not affected by any compensation from a provider is frequently made.

Click image to see larger version

One site that is a bit different is FindABetterBank, from Novantas. Rather than charge for placement, the firm’s site makes this data-oriented pitch: “FindABetterBank is the largest and most sophisticated research database about active bank shoppers. 90% of shoppers that use the comparison tool will be opening new checking accounts within 90 days — so understanding their preferences, behaviors and choices is important, regardless of your size or location. We provide custom reporting, on-going analysis and access to our experts. Fees are determined by an institution’s footprint, so small institutions can participate too.”

You won’t find a “rate card” on these sites. Ehmke explains that each affiliate site has a different partnership strategy when it comes to pricing and, further, specific deals are typically subject to negotiation. She says the sites keep the details of their pricing “very close to the vest.”

It’s important to understand that the brands don’t just get exposure on the comparison sites. Ehmke explains that the backlinks the sites provide to the banking brands’ sites benefit those sites, because Google takes the affiliation as a sign of a strong website.

“This is a bigger bank game,” Ehmke explains, “because they are paying more to appear higher up in listings.” Bigger budgets bring bigger exposure.

“The best way to get an affiliate site presence on the cheap is to keep your finger on the pulse of newer affiliate sites.”

— Lierin Ehmke, Comperemedia

“The best way to get an affiliate site presence on the cheap is to keep your finger on the pulse of newer affiliate sites,” says Ehmke, and talk to them while they are still small. Another angle is newer categories. In a recent blog post Ehmke noted that The Points Guy had started covering business credit cards, and that while Capital One has a big presence, there is still white space waiting for alert brands to fill.

“It’s a new-age way of marketing that’s gathered steam in the last decade,” says Ehmke. “It’s a lighter, soft sell, that’s not quite as in-your-face as traditional ads.” She believes the method accounts for about 15% of financial institutions’ total digital advertising budget.

Read More:

- Most Retail Banks Score Poorly for Digital Marketing

- The Digital Ads Banking Consumers Hate Most (And Why)

Some Are Now Partnering with Comparison Sites

There’s yet another twist on working with comparison sites that has already been launched by at least two players, neither of which are industry giants. This is partnering on the offering of banking accounts in some fashion.

“We see this as the 2.0 version of how a bank and a personal finance site can provide consumers with a more cohesive experience.”

— Chris Tremont, Radius Bank

In December 2019 Radius Bank started offering an exclusive high-yield savings account on NerdWallet’s mobile app. Radius is a branchless bank based in Boston with $1.4 billion in assets that pursues numerous strategies, often with a partnership approach.

Radius had worked with NerdWallet both editorially and through a pay-per-click affiliate marketing relationship, according to Chris Tremont, EVP-Virtual Banking. NerdWallet told the bank, which is known for raising deposits via virtual means, that it wanted to include an in-app savings account option for its members. This was a first for NerdWallet, and one proviso was that consumers be able to open the new accounts without leaving the app. This includes know your customer compliance and other technical details.

“It’s about speed and convenience,” says Tremont. The account will exclusively be promoted within the app’s universe, but this is attractive, according to the banker, because a huge number of consumers are using the NerdWallet app.

“We see this as the 2.0 version of how a bank and a personal finance site can provide consumers with a more cohesive experience,” says Tremont. This was the bank’s first foray with a partnered offer of something other than a checking account, he notes. Now that the savings account is up, he adds, the bank is working on an in-app checking product. The bank believes these offerings will be of strong interest to Millennials and Gen X, which are two key groups for the bank, as well as Gen Z.

In late October 2019, Credit Karma, which has spent most of its history on the debt side of finance, launched a high-yield savings account with $1.9 billion-assets MVB Bank, which has a fintech partnership operation in addition to its community banking activities. The accounts can take up to $5 million and remain insured, through an 800-bank network MVB works with.

In both efforts, a key element of the account opening process will be accessing as much applicant information as possible from member records at NerdWallet and Credit Karma, to save time.

Read More: Design Ideas Banking Execs Can Use to Amp Up Their Websites Now

How Comparison Sites Could Impact Voice Search

Another angle to the comparison-site marketing channel goes hand in hand with the movement towards voice search. Both comparison sites and virtual assistants like Siri and Amazon Alexa rely on algorithms for aspects of their information gathering. In a report, “Your Website’s New Job — Supporting Third-Party Content Aggregators,” Charles Golvin, Senior Director Analyst with Gartner, says that brands must rethink the role of their websites.

“Customers and prospects are starting their purchase journey with third-party aggregators, web search, and virtual agents, forcing your website into a supporting role supplying or connecting them to your branded content,” Golvin writes. Essentially, financial institution websites must be built, or rebuilt, to work smoothly as machines go hunting for information, either for a comparison site or to give the virtual assistant something to say.

In a sense, financial brands are increasingly dealing with machines, and they had better present them with something to use, if they want exposure.

“Standardize your content,” continues the Gartner report. “Boost internal connections among your content creators — such as product and SEO teams — to maximize content relevance to machine site visitors.”

Golvin makes it clear there’s two-fold challenge here. Banks and credit unions, like all other brands, will have to devise websites that serve human visitors well when they do come, but they must also acknowledge that some won’t come, at least not initially.

“With customers increasingly consuming web content without actually visiting your brand’s website, you need to focus on adapting your content to be relevant to the agents that gather and re-present your content in these other channels. Scrutinize the structure of your content, platform algorithms, and audience queries to ensure your content matches the needs of desired audiences.”