Banks and credit unions are facing a shrinking deposit pie, so they’re being forced to pay up.

The same economic and competitive factors making deposits more costly also will make maintaining market share more difficult going forward.

In pizza terms, many will be paying more per slice for some time — and the slices will be smaller.

Rate wars are already starting, but with wrinkles that the older generation of financial marketers never faced. And younger marketers are experiencing the first deposit skirmishes in their careers.

This is the first in a series of articles where we’ll explore causes of the sea change, the impact of new competitive factors, and why traditional approaches to building deposits may not be as meaningful going forward.

This is the first of three related articles concerning deposit-gathering in the wake of renewed rate competition. The second installment is “8 Deposit-Raising Tactics You Might Not Be Trying” and the third one is “Rate Wars: How Digital Banks Keep Pushing CDs Higher.”

Why There Are Fewer Deposits to Go Around

Where are deposits going? Part of the answer is that a big chunk of the inflow to banking institutions got used to come from government intervention in reaction to Covid, says consultant Justin Bakst, executive director of Darling Consulting Group. When the government was cutting special checks for everyone and providing Paycheck Protection Program loans, and the Federal Open Market Committee was pushing rates down, “we were shouting off the rooftops, ‘some of this deposit surge will be temporary, start tracking today who these customers are, where these deposits are really coming from, and how might they behave when interest rates start to move higher!'”

A report from Deloitte Center for Financial Services, drawing on Federal Reserve statistics, cites $2 trillion of inflows that came into the banking system during the pandemic.

Experts say that many financial executives became complacent. “It made banks’ core deposits look like they were growing organically,” says Mac Thompson, founder and president at the White Clay consulting firm. “It gave everybody a false sense of security about where their deposits were coming from.”

When rates were low and many consumer expenses were temporarily suspended, balances grew. Now the Federal Reserve is letting a good deal of the water out of the bottom of the monetary bathtub. No one interviewed can say for sure how much of the shrinkage of the base of potential deposits is due to Fed actions, but they all agree it is big.

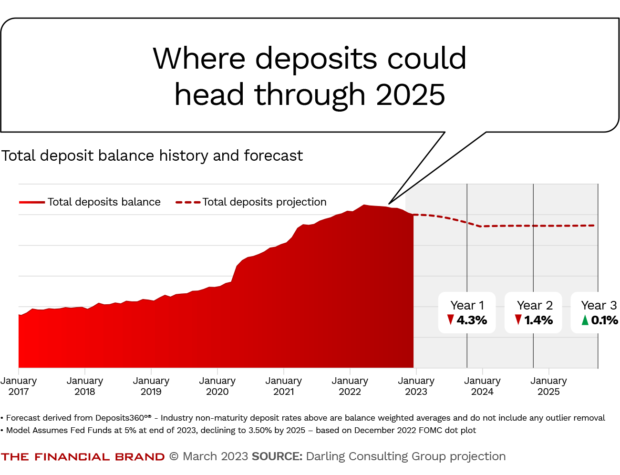

“The Federal Open Market Committee’s decision to relentlessly continue to fight against inflation will continue to contract the money supply, which, by definition, will reduce deposits,” says Bakst. “That doesn’t mean all institutions will see a contraction, but industrywide my firm’s models are showing a decline of over 4% for 2023, which may be a surprise for many bankers.” Bakst says larger deposit accounts are beginning to find more attractive alternatives including money market funds, Treasuries, and higher-rate CDs.

Darling Consulting Group is forecasting a decline in deposits not only for this year, but through 2024. The firm’s model, which works with a database of 20 years of historical data drawn from hundreds of institutions of all sizes, doesn’t indicate deposit growth returning until 2025.

Changing Economic Circumstances Demand Fresh Deposit Strategies

As those projections suggest, it’s not just the Fed’s drainage project that’s removing deposits from the system. There’s the dual impact of inflation and the continuing interest rate hikes the Fed has engineered to attack that inflation.

Many consumers are drawing down savings to keep up with inflation and that money isn’t always winding up back in someone else’s deposit accounts. Companies are affected by inflation too.

“Prices have gone up, but so have the costs of inputs, so there’s a lot more being spent, and labor costs too,” points out Timothy Partridge, principal and commercial banking segment leader at Deloitte Consulting. “Everything costs more.”

“We’re in a different world now, and you have to determine how quickly your bank can adjust to it,” says Thompson of White Clay.

Marketing will be a big part of that adjustment. Adam Stockton, Head of Retail Deposits at Curinos, says the long period of low or virtually 0% rates on deposits, was a historical anomaly, especially in that rate-based deposits were hardly promoted — except as a way into the business for direct banks, neobanks and fintechs to make incursions into traditional institutions’ consumer bases. Even then, with exceptions, the rates were “high” only in comparison with the rock-bottom rates.

“We’re going to see a lot more marketing activity for deposits than we’ve seen over the last three years and over the prior interest-rate cycle from 2009-2016.”

— Adam Stockton, Curinos

The motives for that stepped-up marketing will be mixed, according to the experts interviewed. In some cases the outreach will be broad, especially where institutions still hope for loan growth and the funding to support it. Pretty much every dollar garnered will be coming out of some other depository institution’s coffers. Meanwhile retention will be a battle nearly every bank and credit union will have to fight.

Some financial institutions, by virtue of a niche, a geographic specialty or otherwise, haven’t felt as much pressure yet. S&P Global Market Intelligence issued an analysis in mid-February listing publicly held institutions with very low “betas” — the higher the beta, the more of the increase in market interest rates an institution is passing along to depositors.

Among most of the low-beta institutions the analysts listed a review of their websites shows virtually nothing about deposit interest rates — in fact, on some sites it was hard to even find much information about deposit products. The firm’s analysts suggest that some of these institutions were clearly letting those people clamoring for rate go elsewhere.

By contrast, of the institutions identified as having the highest betas, some were attempting to grow aggressively and paying way up for CDs for fuel. Another subset of the high-beta institutions were crypto industry specialists that had suffered from the ripple effects of the crypto winter, which drew down those deposits, according to the S&P Global analysis.

S&P Global analysts suggest that more institutions will be concentrating on CDs, as well as borrowings from the Federal Home Loan Bank System to bolster their funding. They will be under additional pressure to use both for liquidity because a traditional lever will be avoided. “The spike in rates has left the majority of bank bond portfolios deeply underwater, and most institutions do not want to sell those positions at a loss to meet their liquidity needs,” the S&P Global report states. One upshot will be that the benefits to rising rates to credit portfolios will be lost to the degree that institutions have to pay up to increase or retain funding.

“Everybody is beginning to worry about liquidity and how it lines up with their loan growth strategies,” says Thompson of White Clay. “They’re still trying to grow their loan balances the way they’ve been doing it for the last ten years.”

There are also those who don’t see anything to be concerned about yet. Says Stockton: “One of the big traps that we’ve seen banks fall into is a little bit of hubris saying, ‘Runoff isn’t my problem, it’s somebody else’s problem. The big banks are seeing runoff, but I’m fine, because I’m a community bank.'”

Read More:

- Deposit Armageddon or Opportunity? How to Thrive in a Rate War

- Bankrate, Step Aside. Seattle Bank’s Unbiased CD Site Has National Plans

CD Promotions Ramp Up, But Is Gen Z Getting Lost?

Analysis by Comperemedia has found that the tendency to promote CDs to raise deposits quickly had its roots in 2022, beginning in July, and that spending on CD promotions increased six-fold over the course of the year. That acceleration has been continuing. While banks are in the mix, some of the largest credit unions, including Navy Federal and Pen Fed Credit Union, have been among the biggest CD advertisers, according to the firm.

“There’s getting to be a mad rush for deposits and a lot of people are going the CD route. Super traditional!” says Derek Baker, vice-president, growth and innovation at Mills Marketing. “It’s kind of always the game, playing with CDs, and yet at the same time everyone in the industry is barking that they want younger depositors.”

Indeed, Comperemedia has found that much of the industry’s spending has been on targeted direct mail promoting CDs, according to Andy Colman, associate research analyst. Comperemedia finds this pattern curious for a couple of reasons.

First, new research by the firm indicates that nearly half — 45% — of Generation Z consumers have switched checking account providers recently. “This is a group of people who are looking for ‘something else,'” says Colman. “Yet we’ve noticed a lack of Gen Z targeted messaging, which is an opportunity that would allow brands to get a better bang for their marketing dollar.”

That better bang is not a matter of sending direct mail to Gen Z homes. That’s not what this generation looks at, says Marisa Frys, digital marketing analyst at Comperemedia.

“To reach the younger generations, brands should be targeting them on the channels they are most likely to be on, which would be paid social or online video and display.”

— Marisa Frys, Comperemedia

Frys adds that direct mail tends to be a “bottom-funnel” marketing tool, where very targeted, personalized offers get made.

Colman says that some institutions, in tandem with sweetening the CD rates they are offering, have increased the minimum deposits they want to get those returns. Because they are willing to pay more, they want a bit more in return, he explains.

Another quirk is that most of what Comperemedia sees being promoted is still the standard CD product, no bells and whistles. By contrast, Colman points out, Goldman Sachs’ Marcus online-only bank, still out there pitching, has been promoting no-penalty CDs. Frys notes that Marcus has primarily been promoting its CDs via digital display ads and paid social.

Read More:

- Gen Z Takes Money Seriously at a Young Age — and Will Leave Banks That Don’t Deliver

- Can Banks Hang On to Low-Cost Deposits as Rates Rise?

Why the CD Skepticism?

Baker suggests that financial institutions are stuck in a rut with CDs. There’s one school of thought that Gen Zers and Millennials just have to be “educated” about CDs. Baker thinks that is old-school.

He sees younger consumers thinking over the proposition and scratching their heads: Where’s the attraction?

“So, I’m locking my money in and I can’t touch it without having to pay a big penalty?” says Baker. “It’s a product that’s been around for a long time. Older people like to engage with it more. So you are timing out your overall relationships.”

Baker thinks financial institutions have to think about what else is out there for younger people who are not risk averse to put their money into. He suggests that younger customers who have $100,000 to work with are going to do the math when offered a 4.5% interest rate, for instance.

Sure, “4.5% sounds nice over, say, 13 months,” says Baker, “but when you actually compute the interest, it’s not that much money — and then you tell me I can’t touch it during that timeframe?”

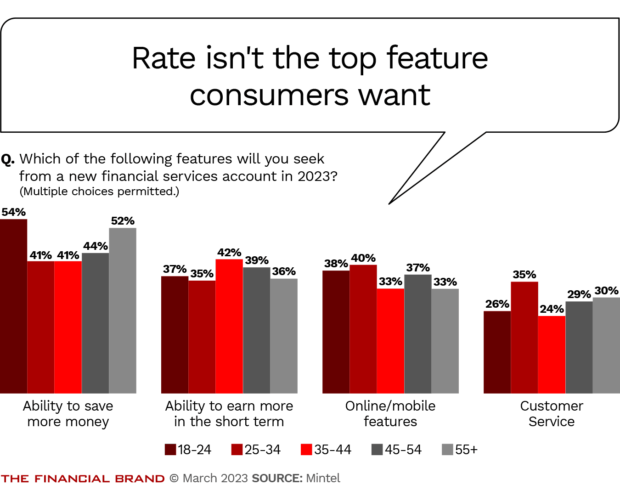

Mintel/Comperemedia has found that one of younger consumers’ top desires from a new financial services account is not earning more but saving more. While this is important to all generations to some degree, Gen Zers chose this 54% of the time in a Mintel survey — 17 percentage points more than those Gen Zers who want greater returns.

Are CD Offers Just a Snooze Button for Bankers’ Deposit Angst?

But that’s just part of Baker’s concern about the industry continually seeing CDs as their go-to. Offering a great rate can sometimes be a matter of kicking the funding challenge down the road. The issue: You always come back to it.

Baker argues that CDs almost by definition are short-term relationships. Offer something juicy now, and in six months or 12 months, when they begin to mature, what will be your retention strategy, he asks.

“Right now, they’ll say, ‘we need to raise this much money by this date,’” he says.

But, “how are you going to keep those deposits?” asks Baker. “No one’s thinking about that. I know that they’re saying, ‘Yeah, well, we’ll figure it out.'”