Marketing segmentation is one of the most widely used marketing tools and has long played a crucial role in identifying and treating differences among customers. For decades, bank and credit union marketers have used demographic segmentation for product development, product positioning, marketing communication and results measurement. Traditionally, this segmentation has been done based on characteristics such as age, income, gender, family life stage, occupation, education, race, etc.

The reason for using demographic segmentation is that it is relatively easy to use for most financial institutions due to relatively accessible customer databases and because this form of segmentation is continuously referenced by both academic and trade literature. While it is still true that there are differences in the use of financial services across demographic segments, however, research as far back as the 1960s has suggested that demographic variables are only remote proxies for differences in buying styles, decision processes or sensitivity to promotional influences (A Two Dimensional Concept of Brand Loyalty).

A more recent research paper in the Journal of Financial Services Marketing entitled Suboptimal Segmentation: Assessing The Use of Demographics In Financial Services Advertising found that there is little support for the reliance on demographic variables for bank marketing. Despite continuing popularity, the research found that while demographics can explain broad behaviors, they play a weak role in explaining brand preference, product purchasing, innovation adoption, channel use and technology uptake.

The explanation provided by the research indicates that customers today are better educated, more individualistic, more marketing literate and more influenced by the convenience of new channels and product offers than the customers of the 1960s and 1970s (when demographic modeling first came into vogue). The result is a significant fragmentation of the marketplace into much smaller groups that can’t be defined by age, income, and other simplistic variables.

For the research, customers of the banks analyzed importance scales on 28 service related comments that related to nine key financial service factors such as website appeal, trust, customer service (pre- and post-sale), how the customer gathers insight, ease of contact, appeal of marketing, appeal of personalization (both in marketing and on the website), brand image and products used. The responses were analyzed against five demographic measures: age, gender, income, occupation and education.

Overwhelmingly, significant differences between demographic groups were not found, suggesting that demographic segmentation is a suboptimal basis for targeting marketing to customers. This should not be a total surprise to bank marketers if they were to do a simply straw poll of their demographically similar friends to see what services they hold, how they transact their banking, how much they trust the banking industry and their willingness to try new technologies.

More than ever, interests, opinions and overt behaviors are a much better indicator of customer demand according to the recent studies around the use of ‘big data’. How does the customer save, spend, and transact is a much more powerful determinant of future financial product purchase and use patterns than the demographic profile of a customer.

Beyond Demographic Segmentation – External Tools

Part of the challenge of going beyond demographics for financial services segmentation is that some key data elements may be missing on a banks customer database or may be difficult to collect for modeling purposes due to internal data silos (product use, channel use, spend and payment data, etc.). Secondly, the difficulty and/or cost of acquiring some primary customer data may be prohibitive (social insights, credit insights).

In response to these needs, some tools have been developed using census-based (non-personal) insights. Many of these have been marketed by credit bureaus and other providers, providing more accurate geodemographic classifications that can be overlaid on customer profiles for better targeting and analysis. A summary of the segmentation advances made by bank marketers can be found in another research paper entitled, The Evolution of Segmentation Methods in Financial Services.

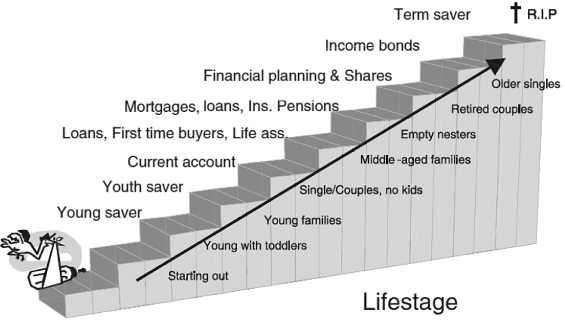

Within the context of the evolution of bank segmentation, some financial organizations have created needs-based segmentation that combines, age, family structure, age of children, etc. While some of this data is difficult to compile, it helps in the determination of produce needs and use. PriZm from Nielsen is a good example of segmentation based on lifestyle and lifestage. As with the geodemographic segmentation above, this type of lifestyle segmentation is not done at the household level but is approximated based on neighborhood insight. The power of this type of tool, therefore, will depend on how it is used (modeling, analysis) and how important personalized data is to the needs of the marketer.

Beyond Demographic Segmentation – CRM Tools

At its core, CRM is primarily concerned with obtaining knowledge about the customer at three levels:

- Understanding the demographic composition of the customer

- Understanding how the customer interacts with the bank (what products are held, what is the balance of the accounts and how do they use the service(s)

- Understanding channel use and preferences

- Understanding how to leverage this insight to sell more and prevent attrition

- Understanding a customer’s channel preference for purchasing new products and transacting with current products is invaluable for banks and credit unions that have both extensive physical networks but also evolving online and mobile channels that impact a customer experience.

Organizations without channel preference insight from a marketing perspective are at a competitive disadvantage and are apt to be wasting significant marketing dollars. Similarly, those banks that simply defer to email and/or online or digital channel are also missing significant opportunities from consumers who prefer traditional channels.

While third party tools have been developed to approximate consumer channel preferences, research has shown that channel preferences differ between most other industries (retail) and financial services. By understanding customer demand for each channel, institutions are able to optimize channel mix and allocate resources accordingly.

Behavioral Segmentation

Behavioral marketing is gaining followers within the marketing community while the dimensions of how to segment based on behavior differs from institution to institution. While some organizations will segment based on internal purchase, payments, and/or use dynamics, others are expanding the realm of behavior captured to include digital and/or social behavior.

Decisions as to what behavior to include usually is based on access to insight and ability to process the insight. As was intended by demographic segmentation, the goal of behavioral segmentation is to divide the customer (or prospect) base into quasi-homogeneous groups that align with a bank marketers’ business strategies.

A report from Aite Group uses a customer’s financial activity to distinguish between segments, providing insights into purchase behavior, likelihood of referrals, interest in deals, revenue potential, risk of attrition, etc. By assigning a score to the frequency of various financial activities, insight can be gained regarding marketing opportunities (and risks) by segment.

“Segmenting consumers by how many products they own or whether they are of a certain age, income classification or educational status does very little to help banks or credit unions improve marketing effectiveness,” stated Ron Shevlin, senior analyst for Aite Group and author of the report. “Tracking customers’ engagement is a much better predictor of customer relationship growth and referral behavior, and it helps banks and credit unions improve the relevance and focus of their marketing communications.”

Interestingly, as with any segmentation or grouping of customers, there are risks to making broad assumptions with the insight. For instance, in the Aite report, highly active customers provided both an excellent source of relationship growth and referrals but also were more likely to attrite (consistent with their high activity and comfort level with channels). That said, the report found ways to make this highly active group more engaged through Personal Financial Management (PFM) tools which are valued by the highly active segment.

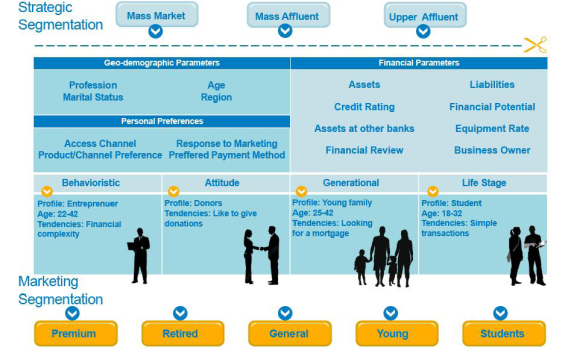

Bringing It All Together

While any one segmentation process can be powerful as a tool for bank marketers, many of the larger financial organizations combine many of these tools to provide a multi-dimensional view of their customers and their needs. An example of this type of segmentation was provided by AdKit:

Options For Financial Marketers

In an era where information is prevalent and relatively easy to obtain, it is imperative that advanced segmentation dimensions be identified, tested and utilized for more effective (and efficient) marketing. With increased competition and ever-tightening margins, firms that are not able to successfully pinpoint potential customers, cross-sell indicators and income opportunities will be at a significant disadvantage to those more progressive organizations.

It is time to pursue targeting of customers and prospects that goes well beyond demographic variables that have been proven to be suboptimal. This will require testing and mirroring what is being done by the best in the financial services industry as well as other industries.