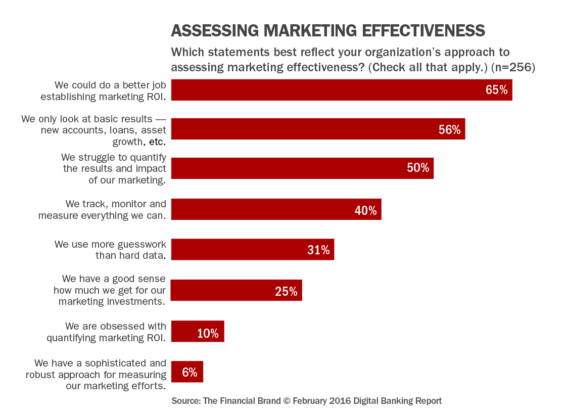

According to the 2016 State of Financial Marketing Report, published by the Digital Banking Report and sponsored by Deluxe, the majority of financial institutions do not know if their marketing efforts are bringing a good return on investment. Two-thirds of financial institutions completing the survey said, “We could do a better job establishing a marketing ROI,” with 56% mentioning that only basic results are reviewed and 50% saying there is a struggle with quantifying the results and impact of marketing.

Worse yet, 31% indicated, “We use more guesswork than hard data,” while only 10% said, “We are obsessed with quantifying marketing ROI.”. This is generally due to a lack of resources or a simple lack of discipline to track results. But throwing resources at the problem can be a wasted effort without properly tracking results.

Almost any type of marketing campaign has two interrelated objectives; 1) produce accounts and balances and, 2) have a positive impact of underlying customer relationship. The financial institutions that do manage to track campaigns focus almost exclusively on counting accounts and balances in promoted products. However, without the broader relationship component, they may be missing a material portion of the profit generated by a campaign.

Click Here to Download the 2016 Study

If a vast majority of financial institutions are not tracking their marketing efforts, then it follows that most marketing and growth strategies are not optimized. Simply put, marketing budgets could be better spent to maximize profitability. The largest reason marketing budgets are not efficiently spent is because financial institution are not using data to effectively identify marketing opportunities or to measure campaign results.

If a vast majority of financial institutions are not tracking their marketing efforts, then it follows that most marketing and growth strategies are not optimized. Simply put, marketing budgets could be better spent to maximize profitability. The largest reason marketing budgets are not efficiently spent is because financial institution are not using data to effectively identify marketing opportunities or to measure campaign results.

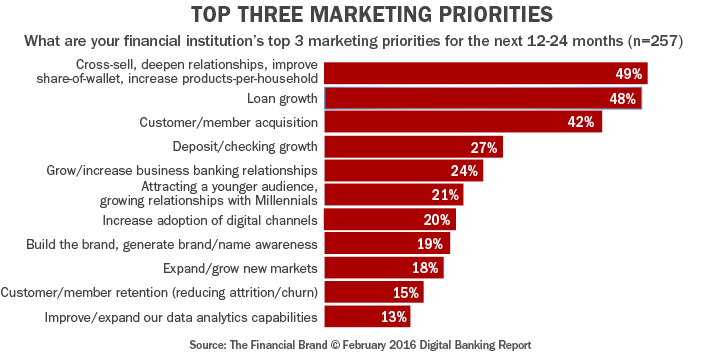

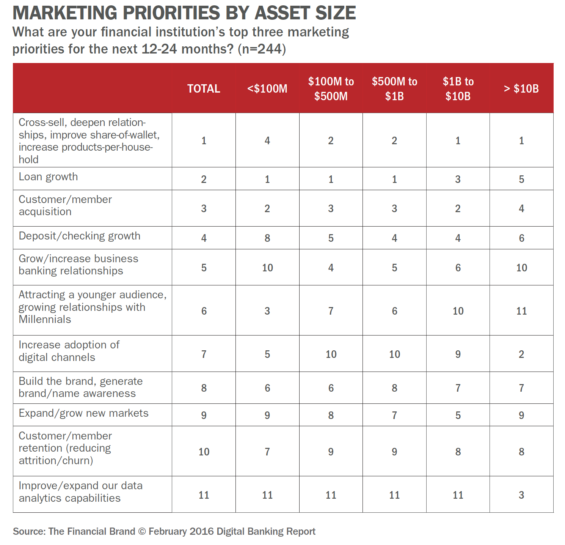

This is made clear in the Digital Banking Report research, where the priority of “Improve/expand data analytics capabilities” was ranked last, except by the largest financial institutions. This represents a marketing performance “perfect storm,” as senior management is demanding more efficient use of resources and measurement of results, yet most banks and credit unions are not budgeting or committing resources to this requirement.

Updating Old Marketing Measurement Tools

Financial institutions often rely on anecdotal evidence self-reported by branches and individual employees when attempting to determine the success or failure of a marketing campaign. Relying solely on the perspective of employees without data-driven, measurable analytics almost always underestimates the impact of marketing efforts.

There are three categories of data financial institutions should look at when attempting to gauge whether or not their marketing campaigns are successful; 1) account and balances data, 2) customer profile data and, 3) halo effect data.

Account and balances data gives the number of accounts and balances that were opened by the target audience during the timeframe of the campaign. However, even this data requires more than a cursory view. For example, what if a customer is attracted by a home equity rate offer, but doesn’t have sufficient lendable equity and opens an installment loan instead? Sorting through all new account activity associated with a campaign universe is an essential first step in determining the profit impact of the campaign.

Profile data describes what the customer relationship looked like before the campaign and how that relationship changed during the campaign. If utilized properly, profile data can help a marketer answer key questions like:

- What types of customers or members were more or less likely to buy the promoted product?

- What segments were disproportionately responsible for the account balances generated in the promoted product?

- How many single service customers/members became multi-service by virtue of responding?

- How many deposit-only customers/members bought their first loan with the financial institution?

- How many loan-only customers/members bought a checking account with the financial institution?

- How many customers/members who bought the promoted product had been with the financial institution for multiple years?

These types of insights have direct relevance to improving the next marketing event and on assessing the effect of marketing on retention and the long term value of key customer relationships. When a financial service marketer sells a product to a customer that is already profitable, they not only get a quality account but also reduce the financial institution’s attrition risk.

Related to profile data, halo effect data describes net inflows of overall balances at a customer level as well as products a client signs up for in addition to services which were directly marketed. A financial institution cannot accurately assess the impact of a loan, money market or CD campaign without comparing the account balance of a responder to the net inflow of new balances of that household.

A campaign that produces $10 million in money market balances with only a $2 million increase in net deposits is demonstrably different than one that produces $10 million in balances with a $10 million increase in net deposits. This type of analysis will often prove that proactive cross-selling can prevent attrition of balances that would otherwise take place.

In addition to assessing the net inflows of dollars, it is also important to quantify what other products the responder to the primary offer are buying. For example, it is very useful determining how many checking accounts were opened by responders to a home equity campaign or vice versa. This provides direct insight into sales effectiveness as a measure of how many sales people are able to turn one sale into two.

Marketing Optimization

A final note on getting a meaningful assessment of campaign results. The ability to benchmark results to peers provides obvious value by comparing response rates, average balances and halo effects for a variety of key segments. This data helps assess the relative effectiveness of key marketing components, which can include the offer, product, sales effectiveness, distribution of electronic services and pricing.

Financial institutions may think their marketing efforts are sufficient, but if they are not assessing the full range of data they are most likely not optimizing the impact of their marketing budget. Feedback from branches is not enough. The proper set of statistics can paint a more comprehensive picture of the success of every dollar spent from a marketing budget.