Do banks and credit unions really need yet another platform to manage their data?

Proponents of customer data platforms say integrating a CDP into an institution’s infrastructure can improve data management and the ability to personalize marketing messages. A valuable, even necessary goal, to be sure, but CDPs are not new and the question has always been whether they go far enough beyond what customer relationship management and other data systems can do.

CDP vendors naturally think so, but increasingly so do users.

At SafeAmerica Credit Union, the customer data platform is a critical component of marketing, compliance and aggregating data across the entire organization, says Steven Page, VP & Chief Marketing, Digital and IT Officer.

“It just gives bank marketers an upper hand,” Page told The Financial Brand. “You can do a lot more with the data you have and do everything faster and quicker. And on the backend, it helps with privacy, compliance, and content.”

Page’s comments are notable because CDPs are more often used by very large banks. SafeAmerica, based in Pleasanton, Calif., has total assets of just $512 million.

What CDPs Can Accomplish

In MarTech’s in-depth 2022 CDP status report, customer data platforms are defined as a “marketer-managed system designed to collect customer data from all sources, normalize it and build unique, unified profiles of each individual customer.” The firm notes CDPs offer five main capabilities: data management, robust analytics, orchestration of marketing campaigns, data regulation compliance, and third-party systems integration.

In its simplest terms, a customer data platform offers a unified view of the customer, so marketing and business teams can grow their business, deliver better customer experiences and drive loyalty, says Chris Jones, Chief Product Officer at Amperity, a CDP provider.

A Good Match:

Modern core banking systems, expected at more and more institutions over the next five years or so, will enable full use of a CDP's capabilities.

“A customer data platform will simplify data consolidation with an AI-based approach that includes all your customer data,” Jones states. “Banking is one of the industries that could most benefit from a CDP. Most banks do not have accurate, unified profiles of their customers with role-based accessibility for marketing and analytics.”

Read More:

- Banking Needs To Prepare For Marketing’s Data Arms Race

- Mastercard CMO: Why Traditional Bank Marketing Is Failing

- Solving the Marketing & Sales Attribution Dilemma in Banking

Data Gaps Are Still Common in Banking

Most financial institutions have a prodigious amount of customer data under their roofs, but often struggle to channel it into usable form. The reality is that legacy core platforms, whether in-house or outsourced, aren’t well suited for an era of unlimited data, mobile applications, omnichannel interactions, and real-time capabilities.

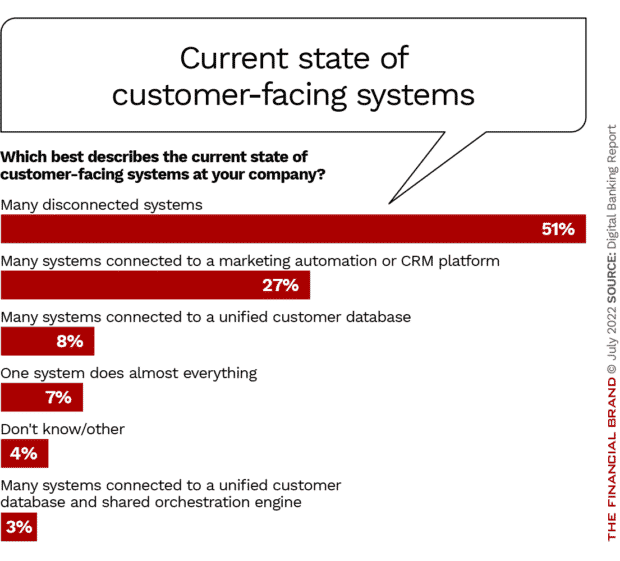

To be most useful, data must be accessible to all business units to access customer insights and support decision-making in real-time. The Digital Banking Report’s survey of financial institutions in 2021 and found many remain saddled with various disconnected sources of data and systems. Only a small portion had a central system for collecting, processing, analyzing and deploying insights.

“Until organizations establish an overarching data-driven culture, the optimization of data for revenue generation and cost containment will not be achieved,” wrote Jim Marous, CEO of the Digital Banking Report and Co-Publisher of The Financial Brand, in an earlier article. “More importantly, the application of insights for improved customer experiences will not be achieved.”

Interestingly, even many financial institutions that use CDPs aren’t yet fully optimized. In fact, 62% of organizations were either “highly dissatisfied” or “somewhat dissatisfied” with their current customer data platform and insight access, according to DBR’s survey. Yet, this sentiment may change as the CDPs expand and become more capable.

The CDP market is forecast to grow at a compound annual growth rate of 34% between now and 2027, according to Gartner. The technology research and consulting firm also predicts that by 2023, up to 70% of independent CDP vendors will be acquired or acquire other technologies. Many of these players will migrate into personalization, multichannel marketing, consent management, and master data management, Gartner states.

Read More: What Customer Data Platforms Can (and Can’t) Do For Banks

Wasted Marketing Horsepower?

While many banks and credit unions already have CRM software and automated marketing platforms, some question whether they need another solution. The proponents’ response is that while marketing automation tools and CRMs can support email and campaign orchestration, a CDP can enhance customer segmentation and profiles.

CRM systems “were never meant for data sharing and they lack the ability to bring data into a single environment where artificial intelligence can truly process this information,” states an Adobe blog.

Without complete data profiles, even the best marketing tools can leave financial marketers with poor targeting and wasted ad dollars. A CDP platform is “a little different than a CRM,” observes Page. “It puts together who our audience is and how we market to them. It makes us better marketers and gives members exactly what they want without a shotgun approach that blows everything out there hoping someone will understand it.”

Page says the CDP has become a critical tool for marketing and messaging at SafeAmerica. “You’re going to have a little bit more relevant content in campaigns to certain groups,” says Page. “We can now know exactly who a group is, what they need, and that [a message] will be more relevant.”

Read More: Go Beyond ROI With ‘Return on Experience’ in Banking

Hidden in Plain Sight

While banks don’t have a problem identifying their customers, their inability to connect the dots often leaves them with many missed opportunities, observes Jones. In one example, a banking client was shocked when its “data stitch process” tied what it thought was anonymous traffic back to customer churn. That visibility opened a new opportunity to pursue those customers and bring them back.

“Even when customers are well known, data siloes cause issues. ‘Why is my bank still sending me marketing messages to download the app I access daily?’ is one example of flawed data use,” says Jones.

As banks modernize their core systems — which many are expected to do over the next five-plus years — they have an opportunity to integrate a customer data platform that will make it easier to tap into the potential of customer personalization, says Kevin Shaver, VP of Solutions Engineering at software provider NGDATA, in a post on LinkedIn.

Such a core platform, using modern cloud-based technology, “can combine insights from every stage of a customer’s banking journey,” says Shaver, “from their transaction history to their current spending patterns, to create a constantly maturing customer account portfolio.”