As banks and credit unions work to align their interactions with customers across channels and track relationships across the entire lifecycle, they are seeking out customer relationship management systems. But many are finding that CRM — whether they are adopting it for the first time or replacing a system they already have — is a complex process with a lot of potential pitfalls.

“I wish it were just as easy as finding the right vendor and going with them, but it’s not,” says Joan Reukauf, chief operating officer and market president at People’s Bank of Commerce in Medford, Ore.

“Finding a platform that will fit your bank for what you need is a challenge and takes time.”

Institutions that discover their CRM falls short typically say it is due to complexity, a lack of integration and customization, or not having anyone who can manage it. But following some best practices can help increase the odds of success.

Searching for a CRM System That’s the Right Fit

Both People’s Bank of Commerce and FNCB Bank are among those that have been disappointed.

Resources for Researching CRM Options:

• Capterra

• Clutch.io

• Crowd Reviews

• Experts Exchange

• Forrester

• G2

• Gartner

• GetApp

• IDC

• SourceForge

• True Digital

• TrustRadius

The CRM system at People’s Bank of Commerce doesn’t serve the entire institution, Reukauf says. When her bank implemented the platform a few years ago, it was only vetted by the operations team and didn’t suit the needs of all areas of the bank, such as the credit department.

FNCB Bank in Dunmore, Pa., adopted Salesforce seven years ago to help frontline staff build relationships and cross-sell, says Michael Cummings, its senior vice president and marketing manager.

But after the bank started to use it, the leadership team realized the system needed an expert to manage it. It also required a lot of time and customization beyond the bank’s capabilities.

“It was very powerful, but way more than we needed,” Cummings says. “It also required individual licenses and didn’t offer an enterprise-wide solution, which made the cost much higher.”

Read more: Customer Data Platforms Are Now a Critical Marketing Tool

Start with the Business Case for CRM

CRM systems — which are designed to make customer information understandable, transparent and actionable to employees — have many applications.

Institutions often deploy CRM to bring data into one system and out of the siloed technology platforms that serve various banking channels. CRM helps scale personalization, automate marketing outreach and improve cross-sales, among other benefits.

“If you ask ten people at a community bank what a CRM means to them, I’d bet you get ten different answers.”

— James White, Total Expert

But one of the primary challenges facing banks and credit unions when they shop for CRM systems is a lack of clarity about the business problem they want to solve, says James White, who is the general manager for banking at the CRM company Total Expert.

“Functionality is important, but often people are too focused on functionality,” he says. “Without knowing the business problem, you are trying to solve, teams can get really tactical and forget why they chose to buy a technology in the first place.”

Specificity matters. “They say I want a 360 view, I want to track, or I want reporting, but the institution doesn’t need the functionality in a vacuum,” White says. “Their questions should be: What part of the business are you trying to improve and why? Do you have a growth problem? Are you trying to improve customer service? A CRM may or may not be a part of that.”

With a business objective tied to the strategic plan of the institution, leaders have a far better understanding of the functionality they need. “Desired outcomes define the ways a technology will make it a reality,” White says. “Then leadership needs to drive the culture change.”

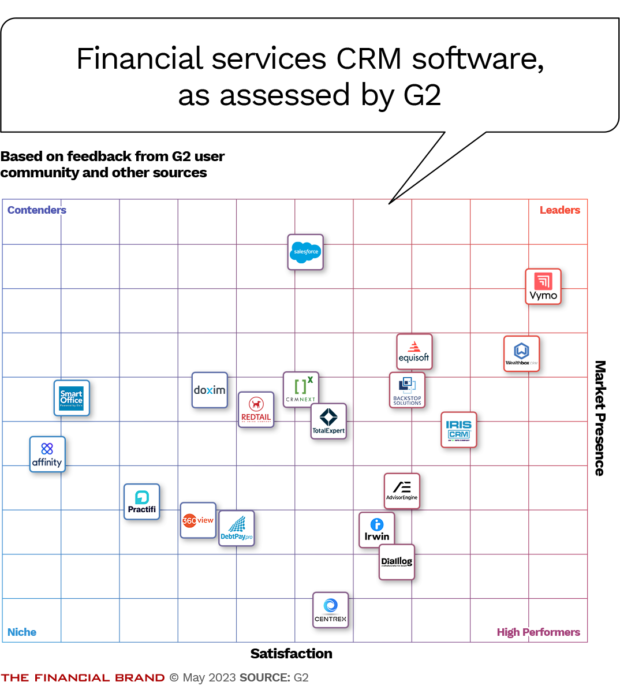

Many of the resources for researching CRM options are pay-to-play, but G2.com has the most information available without a paywall, including a list of financial services CRMs.

Getting Input and Buy-In During the CRM Search

Because CRM systems are a relatively big expense for community banks and credit unions, they need to choose a product that offers the most value based on integration, performance and cost.

Reukauf, who has worked at large regional banks and community banks, says smaller institutions lack the leverage to get customization assistance from most CRM providers.

Smaller institutions typically don’t have a skilled administrator either, so the staff often fumbles with onboarding and using the system. “Size does matter in getting help,” Reukauf says. “And finding that perfect CRM that will fit your company for what you wanted to do and is easy to use is a challenge.”

In its latest search for a new CRM system, the $803 million-asset People’s Bank of Commerce started the process with a group of stakeholders from across the bank, including the marketing, credit and deposit areas.

This time, collaborating and ensuring the system works for everyone is critical, says Reukauf. The group created a well-discussed list of needs before it even began looking at CRM options.

Read More:

- 4 Ways Digital Leaders Can Use Open Banking and APIs

- How TD Bank Works to Create an Emotional Connection with Customers

- See all our latest coverage of bank technology

Support from the Top Is Key to CRM Success

By 2018, FNCB Bank had entered the CRM market again, this time with a new game plan. It sought a CRM that could integrate with its core (Fiserv DNA), was built specifically for banks, was easy to use, and offered an enterprise-wide license.

The committee charged with evaluating the options included people from across the bank, including IT, marketing, finance, lending, operations, retail banking and executive teams.

The $1.7 billion-asset FNCB chose 360 View, a CRM platform specifically designed for banks and credit unions, last year.

Having executive sponsorship was critical, says Cummings. “As people tend to resist change, having a well-executed plan and a president who is a big believer in the power of data can help convince the organization of the need for a CRM,” he says.

Some banks mistakenly believe a CRM will create their sales culture when they need to create that first, says David Acevedo, senior vice president and national sales director for the CRM provider 360 View.

With CRM, “you can’t just flip a switch. You need a sales process and culture in place to support it.”

— David Acevedo, 360 View

This entails having a clear vision of what data the bank needs, why it needs it, and how sales will use it to drive revenue.

“I’ve even advised banks not to adopt a CRM until they are ready,” says Acevedo. “You can’t just flip a switch. You need a sales process and culture in place to support it.”

Acevedo also recommends institutions have a skilled CRM administrator who stays on top of the most recent updates and best practices and understands onboarding and how to make the most of the system. This person should also take an active role in enhancing the value that the CRM system delivers by offering user conferences and continuous education.

“Sometimes there’s a perception that a CRM is a cheap and easy investment. It’s not,” Acevedo says. “There’s a real commitment of resources needed.”