When consumers shopping for new banking relationships visit FindABetterBank.com, they have the opportunity to compare which institutions and accounts will cost the least, meet their feature requirements and have the most convenient locations. There are no clear winners: Shoppers don’t all choose the account with the lowest fees or choose the account that meets all of their needs.

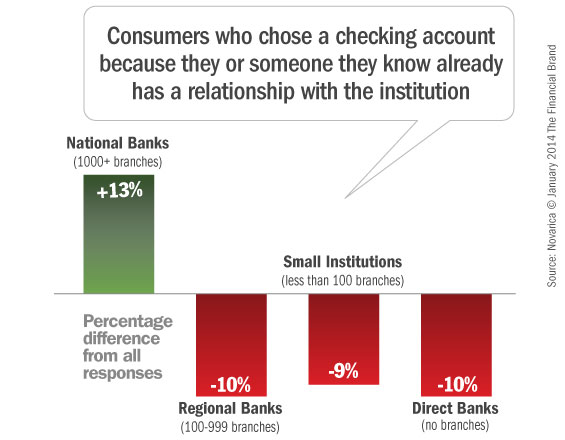

To understand their choices, we asked shoppers why they chose specific accounts. Most give more than one reason. Someone who selects an account with the lowest fees may also like the convenient locations and the mobile app. Another shopper might select an account that doesn’t meet all their needs and costs more than other options because they feel it’s more accessible, or they have a recommendation, or there’s a promotion, etc.

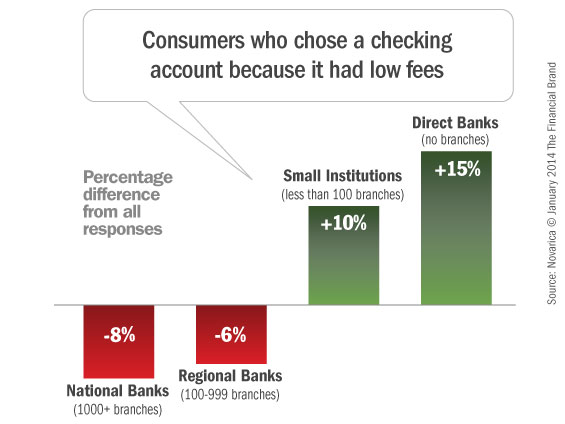

In Q4 2013, 35% of shoppers on FindABetterBank considered price a factor when selecting an account. Differences emerge when comparing shoppers’ responses based on the type of institution they selected.

National Banks (1,000+ branches). Most national banks don’t offer free checking anymore. But they have low-end accounts that enable many shoppers to meet the minimum fee-waiving requirements. Thirty-two percent of shoppers selecting big banks indicated low fees played a role in their choice. This is lower than what shoppers selecting other institutions indicated, but the relatively high response (32%) is an indication that their “no free” pricing strategies have been somewhat effective.

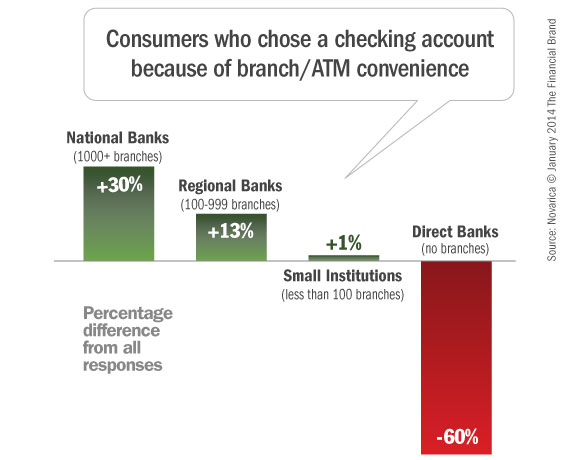

Regional Banks (100 to 999 branches). Price and convenience of locations were the top reasons why shoppers selected mid-sized institutions. But fewer shoppers cited price compared to small institutions and direct banks and fewer cited convenience compared to national banks. These institutions don’t carry the brand-power of the national banks and the fixed costs of maintaining their networks make it difficult to compete on price with the smaller institutions and direct banks.

Small Institutions (less than 100 branches). Fewer shoppers selecting community banks or credit unions cited convenience of branch or ATM locations compared to those selecting larger institutions. These shoppers are much more likely to say price influenced their choice. The gaps in marketing spend and expertise compared with larger institutions is evident: Most small institutions offer access to surcharge-free ATM networks and credit unions even have shared branches. Yet, consumers believe these institutions have less convenient locations.

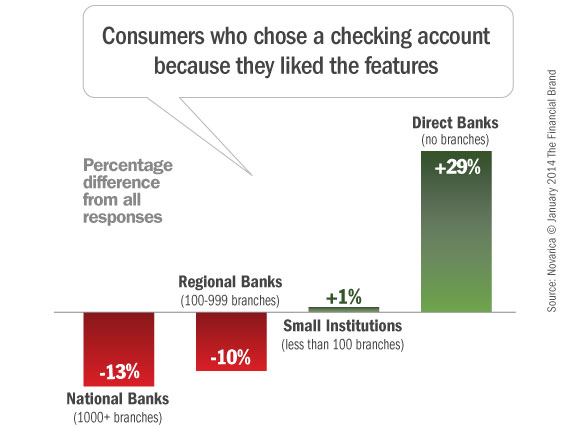

Direct Banks (no branches). Without expensive branch networks to support, direct banks’ checking account options are cheaper than most accounts at branched banks and credit unions. Therefore, one would expect direct banks to attract a large share of price-sensitive shoppers. But 32% of their shoppers say they like the features with the account – much higher than their branched brethren. It shows how advertising engrains impressions: Direct banks’ ads are always about features. Many branched institutions’ ads focus on accessibility – highlighting convenience of their branches and ATMs.