The list of what consumers wanted from their bank or credit union 10 to 15 years ago used to be fairly short: local branches, loans with generous rates and customer service conducive to a convenient banking experience.

Now, the list is much longer. In addition to finessing the mobile and online world, financial institutions are also expected to at least be able to demonstrate their commitment to “sustainable banking” and ESG (environmental, social and governance) strategies. These terms — while they’ve been around for a while — have quickly garnered more interest in the financial industry.

But what is sustainable banking? It goes well past paperless statements and digital cards to encompass embracing and financing sustainable practices — such as lending to renewable energy companies.

A handful of financial institutions have even rolled out “green deposits” as a means to actively involve their customers in deciding where their deposit dollars will be loaned. Sustainable banking is also about financial institutions revamping their strategies to overall lower their carbon footprint.

It’s a global trend. Three out of every five (61%) banking customers in the U.K. said they wanted their banking provider to “do more to create a positive, social and environmental impact,” according to Deloitte.

Additionally, 71% would be more likely to choose a bank or credit union with a positive environmental and social impact.

While European financial institutions are ahead of the game now — U.S. banks and credit unions are closing the gap, according to Val Srinivas, Banking and Capital Markets Research Leader at the Deloitte Center for Financial Services.

“I think U.S. banks are beginning to take meaningful actions, whether it is allocating funds to address racial imbalances in housing finance, small business lending or women entrepreneurship,” Srinivas tells The Financial Brand. “This should permeate through the banking system quickly.”

Even the United Nations understands the gravity of the sustainable banking movement. The UN issued a statement on April 21, announcing 43 banks from 23 countries who are partnering together to be a part of the Net-Zero Banking Alliance, a global organization committing to have net-zero emissions by 2050 or sooner.

Of those 43 banking providers, 6 are from the United States: Amalgamated Bank, Bank of America, BBVA, Citi, Morgan Stanley and Santander.

Get Ready:

“Failing to take a stand or not advancing social and environmental causes won’t be an option,” says Deloitte’s Val Srinivas.

Where banks and credit unions are lacking in eco-friendly strategies, challenger banks are filling in the gaps. Aspiration, for one, is a big player in the sustainable banking space. The neobank’s catchphrase says it all: “Leave Your Bank, Change The World.”

But, exactly how invested are consumers right now in what their bank or credit union is doing for the environment and other social issues?

Read More: How Fintechs and Social Changes Are Radically Reshaping Banking

Who Wants It? And Then Who Really Wants It?

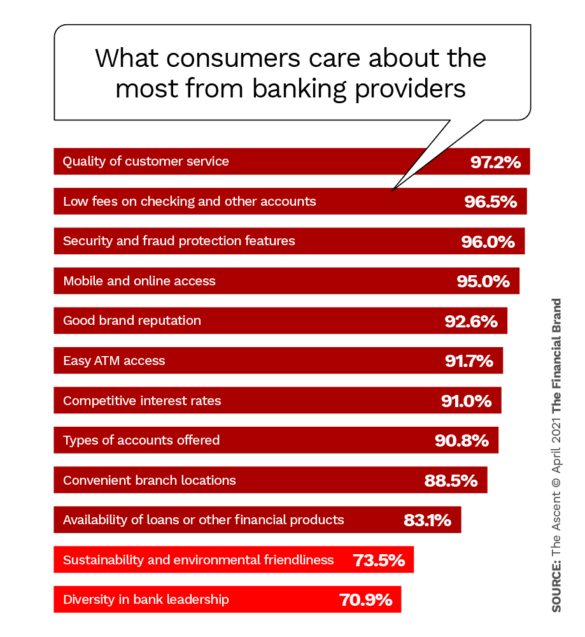

Consumers will always want what directly affects them in the short-term. According to an October 2020 survey by Ascent, over 95% of respondents noted “quality of customer service,” “low fees on checking and other accounts,” “security and fraud protection features” and “mobile and online access” were somewhat or very important to them. These four ranked above “good brand reputation,” which sat at 93%.

Notably, “sustainable and environmental friendliness” didn’t even make the top ten ranked factors, falling below “easy ATM access” and “competitive interest rates.”

But, Keep This In Mind:

Although sustainability isn’t the top issue for banking consumers yet, nearly three quarters say it is at least somewhat — if not very — important to them.

While it’s not exactly top of mind for consumers right now, the “sustainable banking” train has trudged through the industry for a while. Srinivas estimates the trend is at least a decade old.

It really picked up speed in the last three years, according to Celent’s Wealth Management Analyst Neil Sheehan, who noted some of the progress can likely be attributed to BlackRock and JP Morgan’s progress with sustainable banking.

“Larry Fink [CEO of BlackRock] and Jamie Dimon [CEO of JP Morgan] got together and they put out this push from an institutional side,” Sheehan told The Financial Brand. Typically, the view has been that a corporation maximizes shareholder profits, he explains, but these high-profile financial executives changed the message to, “It’s not just the shareholders that matter. It’s the stakeholders,” which includes employees and the communities they serve.

“There’s been a huge push around investing in things you believe in.”

— Neil Sheehan, Celent

Sheehan says Fink and Dimon were two of the first top executives to outline their sustainability goals, because so many institutions and people look to them to set the standard.

And sustainable banking strategies are just an indicator of a larger trend, Sheehan adds. Consumers want their banking providers to understand their values, whether that be a need for diversity on a board of directors or a focus on human rights and child labor beliefs.

Read More: Banking Must Take A Stand On Tough Social Issues

“There’s been a huge push around investing in things you believe in,” Sheehan observes, adding that the environmental element catalyzed the greater ESG movement. The environmental side is the most mature and has traditionally been a focus for many firms.

Srinivas says he’s noticed the demand for the closely related concept of “green banking” isn’t a high priority yet. “even to the most environmentally conscious consumers.

But that shouldn’t mean banks and credit unions can dismiss it.

“Those banks that are leaders in the space will definitely strengthen their reputations, especially among Gen Z and Millennials,” Srinivas continued. “So, in the long run, banks cannot ignore green or sustainable practices.”

How Are Traditional Strategies Changing?

Everyone in the industry attacks sustainable banking differently. Some institutions have centered their executive strategies on the idea and others are slowing adding green to their game plan.

In the first few months of 2021 alone, major banking players have jumped on board to announce new programs.

For instance, Goldman Sachs jumpstarted a “sustainable finance” campaign, announcing in February it finalized an $800 million sustainability bond that would promote financing for “clean energy, sustainable transport, sustainable food and agriculture, waste and materials, ecosystem services,” among other things.

“The launch of our first sustainability bond shows that investors can drive innovative solutions by using our firm’s extensive platform and resources,” David Solomon, Chairman and CEO at Goldman Sachs, said in a statement.

Several weeks later, MUFG Union Bank announced the launch of its new “Green Deposits” program, allowing its customers to choose how and where their deposits are invested in ESG projects, such as renewable energy or sustainable food, waste management or greenhouse gas reduction, just to name a few.

MUFG, part of Japan’s Mitsubishi UFJ Financial Group, has been in the sustainable solutions space since 2004 when the company started participating in the Carbon Disclosure Project, which encourages corporations to disclose their impact on greenhouse gas emissions.

Also in 2021, JPMorganChase — in addition to contributing $200 billion for transactions supporting climate action and sustainable development — established a team of bankers who will facilitate partnerships with eco-friendly companies.

Before these moves, Citibank introduced its own green deposits framework in November 2020. Val Smith, Citi’s Chief Sustainability Officer, said the bank was “seeing demand for a full range of sustainability offerings, and we are committed to working with our clients as they look towards a smooth transition to a low-carbon economy.”

Noteworthy Point:

Not every financial institution is pivoting their entire strategy to prioritize sustainable banking, nor do they need to. Little steps are still progress.

Other institutions are involved in the Global Alliance for Banking Values, a network of worldwide banks and credit unions focusing on ESG principles. Of the 65 institutions in the alliance, nine are based in the United States.

Many smaller financial institutions — such as Sunrise Banks, a Global Alliance member — are actively involved in sustainable banking. Some have pledged to not finance fossil-fuel endeavors. Others offer “green loans” and “green mortgages” or “green credit cards,” sourced from environmentally friendly materials.

Regardless of where a banking provider is in their eco-friendly game plan, BankTrack, a support organization for financial institutions, recommends banks and credit unions focus on six primary principles to achieve sustainable success.

Commitment to Sustainability

Financial institutions need to make a pact, promising they will integrate ecological limits and consider environmental justice when looking at business practices, such as credit, investing, underwriting and advising.

Commitment to ‘Do No Harm’

BankTrack recommends banking providers ensure they promise to “Do No Harm” when evaluating their existing portfolios and operations.

Commitment to Responsibility

Banks and credit unions need to be accountable for the impacts they have on environments, paying “full and fair share” of the risks they create.

Commitment to Accountability

Financial institutions should also ensure they are accountable to their stakeholders and allow them to have an influence in the back-end financial decisions these financial institutions are making.

Commitment to Transparency

In light of the last point, BankTrack also notes banking providers should disclose financing and other banking practices to their stakeholders, ensuring they understand the transactions taking place.

Commitment to Sustainable Markets and Governance

Lastly, banks and credit unions should also publicly support policies and regulatory legislation which encourage sustainability in social and environmental ways.

Sustainable Banks and Credit Unions vs. Green Neobanks

As mentioned earlier, banks and credit unions aren’t the only ones galvanized by the sustainable banking movement. Various neobanks recognized the gap in the segment, jumping in to flood the industry with new green alternatives.

Take Aspiration, a challenger mobile bank offering personal debit and credit accounts to consumers. Its “Dimes Worth of Difference” campaign commits to donating ten cents from every dollar the company earns to its catalog of charities.

The neobank also offers 5% cash back on socially conscious transactions and an option for consumers to round up their purchases, putting the extra funds toward reforestation. Aspiration also promises that, when a customer opens up a “Spend & Save” account, their deposits won’t go toward fossil fuel projects.

Read More: Fintech for Good: Five Innovators Changing The Banking World

Tandem, U.K.-based neobank, is likewise piloting a sustainable mortgage lending program. In order to make good on their promise, the bank acquired Allium Lending at the end of 2020, which offers financing to consumers to “make their homes more energy-efficient and environmentally friendly.”

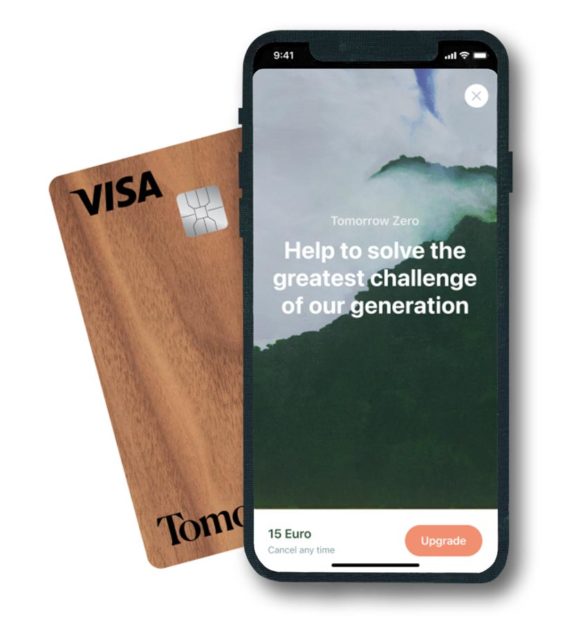

On the other hand, Tomorrow, a neobank based in Germany, offers a wooden debit card, sourced from an Austrian cherry tree. The company says one tree can provide “enough wood for 10,000 cards,” in contrast to a single-use plastic card.

The digital bank also invests in sustainable bonds, pushing nearly $4.3 million into renewable energies and $7.1 million into social housing. Additionally, Tomorrow boasts that, for every euro paid using their card, consumers can save one square mile of the rain forest from deforestation as the company invests in sustainable solutions.