The ‘Great Resignation’ has been an unexpected result of Covid-19, but its impact on the banking industry could last long after the pandemic is tamed. Nationally, almost 35 million people have quit their jobs in 2021, with 4.4 million of those departing in September alone, according to the U.S. Labor Department. What makes the situation worse is the number of people returning to the job market is lower than expected, creating an increasingly tight labor market.

“Central bank officials are hoping that jobs lost during the pandemic return soon, but progress in recent months has been stop and start,” the New York Times noted. In October, almost 600,000 people joined the workforce, but that still left 2.4 million fewer people in the labor force than before the pandemic hit, according to the Wall Street Journal.

Frontline banking employees felt the weight of the pandemic as many financial institutions kept their branches accessible to customers and their call centers functioning. Perhaps it’s not surprising that more than a third (37%) of financial service employees say the pandemic had a net negative impact on their mental health, 22% more reported it took a toll on their workload and another 13% said the same of their physical health, according to BAI.

“Banking employees, for the first time in decades, appear to have the upper hand, especially in sought-after positions.”

— Mark Shilling and Anna Celner, Deloitte

At the same time, many non-customer facing banking employees shifted to a work-from-home mode, as millions of professional workers did. Being forced to step away from the office showed people that commuting to the office every day might not be what they really want to do.

“Banking employees, for the first time in decades, appear to have the upper hand, especially in sought-after positions,” write Mark Shilling and Anna Celner, Principal and Managing Partner respectively, for Deloitte.

Some sources, on the other hand, suggest the bank staffing issue might be overblown. Consulting firm Crowe reports turnover rates for nonofficer roles in banking dropped several percentage points from pre-pandemic levels of 23.6% in 2019 to 16.2% in 2021. Additionally, executive turnover also dropped from 7.3% in 2017 to 3.3% in 2021.

“The data shows that banks have been making great progress in reducing turnover, even during a time when many industries are seeing severe attrition in their workforce,” observes Timothy Reimink, a managing director specializing in financial services consulting at Crowe. Crowe’s report notes that there are institutions who appear to not even be struggling with staffing, which the firm attributes to the fact that almost three out of four banks (74%) allow portions (less than half) of their staff to work from home.

Regardless, experts advise there’s more on the horizon despite reports of low turnover — almost like a calm before the storm. One concern is that the perception of a lack of innovation in banking could keep job seekers from even applying. There are ways to keep talent flowing in and ultimately staying with banks and credit unions. They’re not all simple or easy, but are necessary to return to any sort of normal work environment.

Read More: Engaging Employees to Accelerate Digital Banking Transformation

Job Hopping on the Rise

The Great Resignation likely won’t end in 2022. In fact, Daniel Brousseau, Senior Director and Financial Services Solutions Principal at Medallia — a customer feedback software platform — suggests it will look more like the “Great Job Hopping.”

“A lot of Millennials’ tenure at banks is one to two years,” Brousseau explains to The Financial Brand. “But all the fintechs coming in offer a much more interesting place to work.”

Many fintechs and neobanks in the industry today can claim at least one former legacy banking executive, board member or employee. The freedom to work on new ideas attracts many.

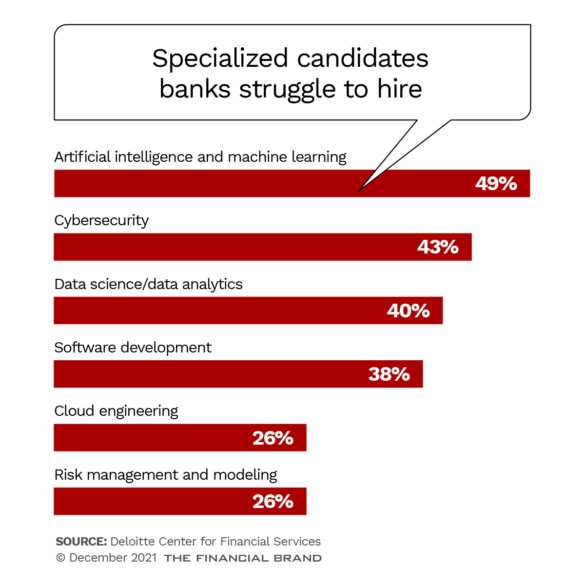

One of the biggest struggles for traditional banking providers, Deloitte finds, is that many institutions are drowning in unqualified talent. In its 2021 Global Outlook Survey, the consulting firm observes that two out of five banking executives say their workforce “was not ready to adapt, reskill, or take on new roles during the pandemic,” a concern that is seeping into interviews with new employees.

To combat this issue, Jill Nowacki — President and CEO of Humanidei and O’Rourke, a firm specializing in employee development at credit unions — tells The Financial Brand opening up the talent pool can be a crucial first step in sidestepping struggles to find the right employees. She says it means embedding diversity and inclusion right into not only the interviews, but in the channels used for posting job openings as well.

“If the first pass of your candidate pool is 100% male, then you’ve probable missed out on some potentially really qualified applicants that might bring a different perspective,” Nowacki explains. She also anticipates the correlation between labor shortages in banking and childcare shortages will become a growing problem. She predicts that mothers struggling to find people to take care of children could soon dominate the next round of staffing conversations.

Listen In: The Increasing Need for Talent, Inclusion and Diversity in Banking

Widening the channels in which your institution looks for employees is crucial.

“The argument that I get most often is that we don’t hire for quotas, we just hire,” Nowackie continues. “But, if you don’t have candidates fully represented in your pool, you don’t know if you’re hiring the best possible candidates. By casting that wider net and making sure you’re reaching more places, you’ll likely bring in more women. You may bring in more men too, which might be more qualified than the men who you had in the first pass.”

A Crucial New Strategy:

Hiring biases can happen unintentionally. By throwing the net out in new directions, financial institutions might find the talent they’ve been looking for.

Nationwide Financial suggests looking outside the financial industry for specific roles.

“Are there educators who are looking for a different job?” the insurance company prompts in a blog post. “Or, Millennials who gravitate towards technology and working from home? Or, recent retirees who are looking to start a second career? ”

Some financial institutions are leaning on the value of job outsourcing. Amerant Bank, based in Coral Gables, Fla. with about $8 billion in assets, partnered up in November 2021 with bank technology company FIS, which will take on chunks of the bank’s backend office work. It is anticipated to save the bank an estimated $12 million dollars annually.

Automation Takes The Stage

In addition to other remedies, it’s important to acknowledge the impact of automation as a possible solution to worker shortages. It doesn’t mean discarding your entire employee network, but instead allowing them to work more efficiently. Wells Fargo, in particular, is prioritizing automation in their strategic planning. Managing Director Mike Mayo spoke to Bloomberg about the megabank’s tech strategy, prophesying that for any jobs lost in the banking industry, automation can be used as a supplement.

“Tech should enable banks to become more efficient than they’ve ever been before in history, and that’s by modernizing back-office branches and call centers,” Mayo explains.

This comes back again to the idea of hiring outside the banking industry. If financial institutions are struggling to find people to staff phone support lines or otherwise, they can instead look to engineers who can innovate old, manual systems which require human staff.

“Tech should enable banks to become more efficient than they’ve ever been before in history.”

— Mike Mayo, Wells Fargo

Sandeep Kumar Sood, Founder of Kunai — a tech-based advisory service for fintechs — says employee shortages might actually work to the benefit of financial institutions. It has happened before, he says.

“What we’re seeing today isn’t really all that new. Ten years ago, Google, Amazon, and Facebook were pilfering engineers from companies like IBM,” Sood notes, adding that banks have to be comfortable with breaking away from the norms they still find themselves conforming to.

“Banks should consider what we already know about the history of engineer shortages,” he explains. “They can address the most common issues by creating attractive opportunities for engineers, changing the way financial institutions hire, train, reskill and upskill developers, working with partners who can circumvent hiring hurdles. Using one or a combination of these approaches will help banks hire and keep development talent.”

Read More: Bad Things Happen When Bank & Credit Union Employees Aren’t Engaged

‘But My Branches Need Employees

Not all jobs can be replaced by automation or engineers at banks and credit unions. Hope isn’t lost, however, there are still plenty of ways to both retain existing employees (and keep them engaged) as well as bring in new staff members that are also highly qualified.

Change the Culture. Culture hasn’t always been top of mind in banking, but it’s going to be. However, banks and credit unions are discovering it’s not easy to just reconstruct an office culture — it takes time and focus. It requires working with existing employees to figure out what they need from the workplace.

“Trust is a really important aspect that’s continually used in marketing and in talking to customers,” says Melissa Arronte, Employee Experience Solution Principal at Medallia. But employees aren’t treated with that same prioritization of trust, she says. “Often, it’s more command and control in a bank, or a compliance mentality.”

Arronte maintains that continually surveying employees — when they finish customer service calls, when they fill out applications, working with a new system, etc. — is crucial for making sure staff stay engaged.

“Every day, we should be able to look and see where are we with applicants, with turnover,” she says. Her co-worker Brousseau adds feedback at each stage can prevent burnout or unnecessary frustrations.

Sometimes, it also takes culturally prioritizing mental health. The Filene Research Institute, a credit union-orientated think tank, spoke to leaders at four different credit unions about how they address mental health for existing employees. Credit unions who report happier employees say they have taken advantage of existing Employee Assistance Programs (EAPs) — voluntary programs that offer counseling — provided opportunities for employees to talk with executives through Q&A forums and helped teams manage work and life balances.

Change Up Traditional Work Norms. Some banks and credit unions have taken the opportunity presented by the pandemic to reconstruct existing workflows for their employees to better suit each team member. For instance, Atom Bank, a U.K. neobank, introduced a four-day working week at the start of November. The idea is that employees work 34 hours over four days — instead of 37.5 over five days — and get either Monday or Friday off. Contracted employee salaries won’t change.

CEO Mark Mullen explains that the five-day work week was first introduced by Henry Ford during the Great Depression, a system that Mullen finds unnecessary in the 21st century. “We now know that many jobs can be done as efficiently and productively from peoples’ own homes as from the office,” he said in a statement. “While we appreciate a four-day working week will not be right for all workplaces, the move to working from home has proved that working practices that may have seemed years away can be introduced rapidly.”

Innovation Where It Matters:

If your employees are telling you they’re burnt out, changing up when and how people work can help. Atom Bank has introduced a four-day work week while other financial institutions have integrated work-from-home into their permanent strategy.

On the other hand, South Carolina Federal Credit Union has fully adopted the work-from-home lifestyle and takes innovative approaches to keep remote employees happy and feel like they are still at home with the rest of the employees.

“We want them to belong,” Chief Strategy Officer Troy Hall told CUManagement, “so we make an extra effort to include our remote staff in communication, micro-learning activities, daily huddles, Zoom lunches and trivia games.” The culture of an organization, Hall says, “is not determined by whether people are under the same roof — it’s how people are treated under whatever roof they’re under.”

Similarly, Humanidei’s Nowacki says Canvas Credit Union has done a great job creating an environment where people feel comfortable from wherever they work.

The credit union’s executive teams continue to be more than happy to allow their headquarter employees to work from home.

“We are not in a rush to get people back here. It’s working well and has been a huge opportunity for us to learn, grow and do things differently,” Tansley Stearns, Canvas Credit Union Chief People and Strategy Officer, tells The Financial Brand.

Consider Incentives and Pay Raises. Increasing the pay scale is almost expected by the industry now as some of the largest players, including Bank of America, raise their minimum wages. Randolph-Brooks Federal Credit Union in Texas — with $14.6 billion in assets — raised their minimum wage to $18 per hour, well above the state’s minimum of $7.25. In Michigan, where the minimum wage is $9.65, Michigan Legacy Credit Union (with $269 million in assets) raised its hourly rate to $16.

While salaries are crucial, how employees are informed about how and how much they’re paid is just as important, says Tanya Jansen, Co-Founder of cloud compensation software provider beqom. The firm conducted a 2021 survey of employees and found 61% are more likely to apply if the salary is included in the posting.

However, Jansen insists that keeping the pay process transparent even after employees are hired is just as important.

“Not only will it create a sense of fairness and eliminate any uncertainty around how compensation is determined, but it can also help create trust between employees and their employers,” she says. “Additionally, pay transparency at a strategic level can help eliminate unconscious bias by providing parameters for pay, and institute fair pay across all genders, races, ages, etc. Building trust, value and fairness will all help retain top talent at an organization, especially during current labor shortages.”