Noted Harvard professor and the foremost authority on competitive strategy, Michael Porter, is quoted as a saying, “The essence of strategy is choosing what NOT to do.” He further explains, “A firm’s relative position within its industry determines whether a firm’s profitability is above or below the industry average. The fundamental basis of above-average profitability in the long run is sustainable competitive advantage. There are two basic types of competitive advantage a firm can possess: low cost or differentiation.”

These lessons are more true in a digital economy than ever before and are the keys to success for a financial services industry that is facing new competitors, a more demanding consumer and a transformation of the products and services that have been the bedrock upon which the industry was built.

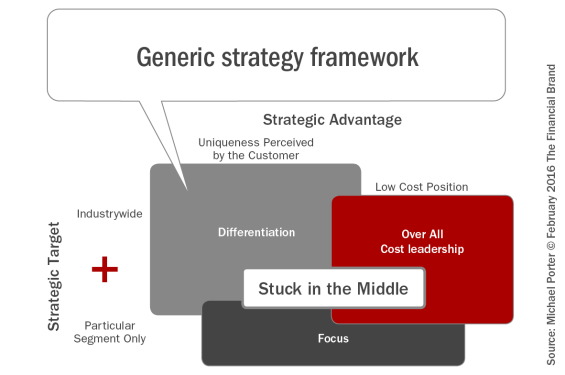

The Power of Focus

The focus strategy concentrates on a narrow segment and within that segment seeks to achieve either a cost advantage or differentiation. For example, following the differentiation focus strategy, Betterment – the largest automated investing service – clearly has a strong advantage by focusing on a narrow segment.

Everything becomes easier when your strategy is narrowly focused on a single market segment. Your people are aligned more clearly. You can present a brand story to the market that is clearer, more succinct, and digestible. The user experience you provide can be laser-focused on intuitively addressing the user need (and as a result, the market need).

The app economy is a great example of the customer increasingly becoming more inclined to buy best-of-breed from the focused specialist instead of the industry generalist. It’s akin to a rollback of the Wal-Mart one-stop shop phenomenon back to the day of single-domain sources. Instead of customers buying multiple mediocre financial services from a mega supplier, customers are buying services from individual specialty purveyors – much like our grandparents going to a bakery, butcher shop, and produce market instead of to a Wal-Mart.

The framework created by the app stores and ecosystems of the devices themselves have paved the way for a nimbler new entrant to quickly gain advantage. Customers are increasingly more comfortable with having the flexibility to choose an array of hand-selected financial services and then bundling them with account aggregation tools from companies like Mint.

Putting the Differentiation Focus Strategy to Work

At a financial services marketer forum recently, industry giants such as Schwab, TIAA-CREF, Franklin Templeton, Wells Fargo and others, were grappling with how their organizations can keep up, compete with new entrants, and leverage their positions for an advantage. The challenge of innovation inside of large financial services companies is substantial. So, how do the big guys compete with the nimble upstarts that have a smaller problem domain and the ability to focus solely on delivering the best possible customer experience?

To effectively compete with new entrants via a focus strategy, traditional financial services firms must:

Adjust the Org Chart

- Create completely autonomous divisions with littleor no connection to the management structure of the mothership brand

- Make the reporting structure high enough in the organization so as to eliminate turf battles

Separate Physical Space

- Physically remove the department(s) from the corporate environment

- Allow departments to create their own culture (e.g., no need to wear a tie, follow existing work from home policies)

Fund it Like a Startup

- Be Darwinian, allowing new divisions to compete directly with those that are already established, let the strongest survive

Run it Like a Startup:

- Move now – Have a bias for action over inaction

- Scale rapidly – Betterment had $1 billion under management a year ago – today it’s over $3 billion

- If you wait, the market opportunity will be gone

There has never been a better time for incumbents to spin up new divisions to attack their existing markets in new ways. Customer loyalty is low, especially as it relates to the recipients of the greatest wealth transfer ever to the millennials and Gen Y. These emerging affluent consumers are building loyalties in a completely new way and brand names have less to do with perceived preference than ever before. The bedrock financial services brands simply do not carry the same brand equity as they did in previous generations – even less so after the financial crisis.

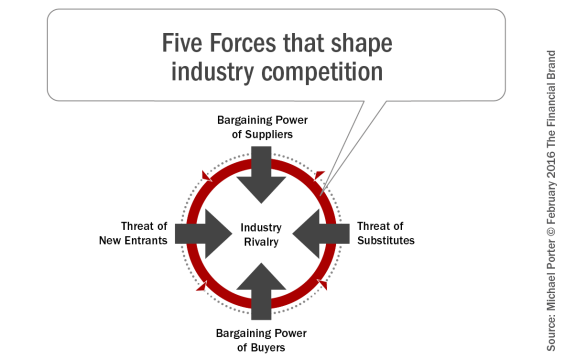

Switching costs are at an all-time low. In the face of the impending greatest generational transfer of wealth from boomers to millennials, it is critical that financial services brands become relevant to the consumer. Access to distribution of apps and services has never been easier with digital. Bargaining power of customers is high and those of suppliers are low. Threat of substitutes is high.

The time is now for traditional financial institutions to shift to innovation in their incumbent product categories. By creating new departments with singular focus, the big guys can capture market share that otherwise would go to the disruptor.

Disruptive services that are connected to the existing core brand have the potential to open up numerous new avenues for differentiation and value-added services. These services will also enable providers to tailor offerings to narrower segments of the market, and customize sets of services for individual customers – supporting differentiation and bringing equity to the core brand.

When considered in the context of Porter’s two types of strategic advantage – low cost and differentiation, it is clear that the market place is an inflection point with regards to the next phase digital transformation.

For the last fifteen years of financial services, digital technology has been characterized by cost cutting and expense reduction strategies – Porter’s Low Cost Strategy. Technologies and platforms have been largely evolutionary with regards to innovation. For example, most online banking platforms changed little in the last ten years.

As more and more of the customer experience was derived from the digital vs. the in-branch experience, the low cost delivery strategy of antiquated platforms and poorly conceived user experiences left customers feeling uncared for. This is why new entrants like Betterment have been so successful and have had such quick growth. They offer exceptional user experiences knowing that for them, the experience is the brand. The entrenched low cost strategy embraced by financial institutions enabled lack of innovation and complacency – a perfect recipe for new entrants.

Today we stand at a tipping point — the app economy favors the narrow specialist. Broad-target financial services firms can enable new, separate and independent divisions to thrive by following a focus strategy lead by great user experience.