Since the financial crisis of 2008, the banking industry has been challenged by economic uncertainty, new regulations, an onslaught of competition and an erosion of trust. Over time, some of these challenges have become ‘business as usual’, while there are new unknowns, such as the implications of Brexit for the UK and the European Union (EU) and the election of Donald Trump as President in the United States.

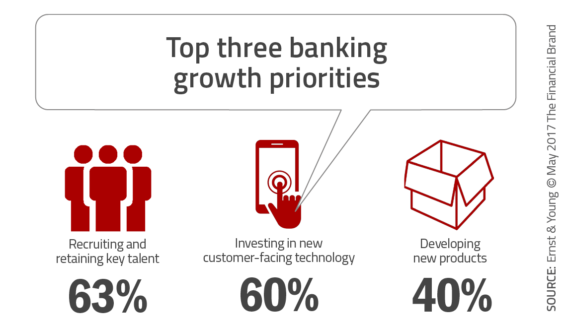

In a survey of almost 300 senior banking executives worldwide, EY found that only 11% of the respondents expected the financial performance of their banks to improve significantly over the next 12 months. The Global Banking Outlook 2017 found that, despite this lack of confidence (or maybe because of it), some 60% of banks see the need to invest in new customer-facing technologies and innovation in order to spur growth.

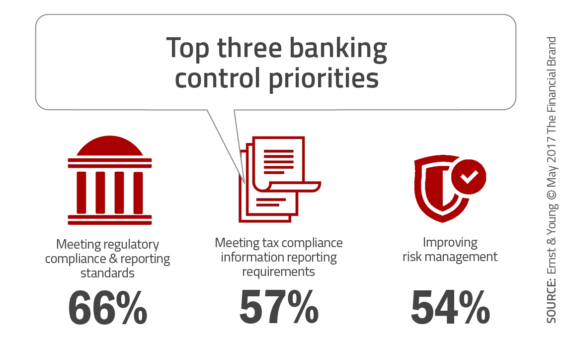

Still, most institutions are currently in a defensive mode, with managing reputational risk and meeting regulatory compliance and reporting standards being the top two strategic priorities. The two key growth agendas are recruiting and retaining talent (63%) and investing in new customer-facing technology (60%).

“Banks realize that they cannot wait for a return to normalcy to achieve meaningful profitability. The industry must innovate to grow or optimize their business so they can be more efficient while also meeting the needs of regulators.” says Dai Bedford, EY Global Banking & Capital Markets Advisory Leader.

Banks need to focus on improving five specific areas inside their organizations according to the EY study.

- Reshape – Banks will need to rethink current organizational structures and decide between four core business models: local boutique, regional champion, global boutique or universal superbank. Banks must identify their strengths and restructure operations accordingly.

- Control – Banks must strengthen their three lines of defense model for non-financial issues, strengthen their focus on vendor management and create simpler supply chains.

- Protect – Banks must rebuild trust and create the right organizational culture. They also need to minimize internal and external threats by replacing legacy IT architecture and using technology to improve protection. Finally, they need to train staff and embed cybersecurity in digital and Fintech agendas.

- Optimize – Banks need to drive further efficiencies by leveraging application program interfaces (APIs), new partnerships and advanced technologies that will improve the customer experience and streamline processes.

- Grow – To retain profitable growth, banks need to invest in advanced analytic technology to personalize offerings and improve experiences for targeted clients. This includes defining product portfolios for growth and defending geographic footprints.

1. Reshape

While some banks have gone through the process of defining the optimal business model they would like to work towards in the future, others are far less certain. EY stresses that now is the time to determine competitive advantages and focus the entire organization around one of four business models:

- Local Boutique – Small or mid-sized organizations focusing on a specific geographic, product and/or customer segment.

- Regional Champion – Built on local expertise and targeted customer base, these organizations span larger geographic areas and provide wider arrary of products and services.

- Global Boutique – Organization that provides limited services or products to global customer base.

- Universal Super Bank – One of a handful of mega-banks that are global in coverage and extensive in depth of services.

As part of the reshaping process, organizations will need to determine whether it is advisable to partner or acquire outside fintech organizations to provide the needed innovation. This process will potentially require reshaping the infrastructure, culture and distribution network.

2. Control

Regulations and compliance are not going away any time in the near future. In fact, global regulators are expected to increase scrutiny around consumer protection and non-financial risk in the years ahead. So, while organizations want to focus on a growth agenda that will increase revenue opportunities, compliance will continue to be a major focus for all financial organizations.

In fact, while EY found that financial institutions have made significant advances in risk management in the years since the financial crisis, there still needs to be a focus on risk management. This includes assessing vendor management risk, improving crisis management, investing in advanced analytics and managing balance sheets.

3. Protect

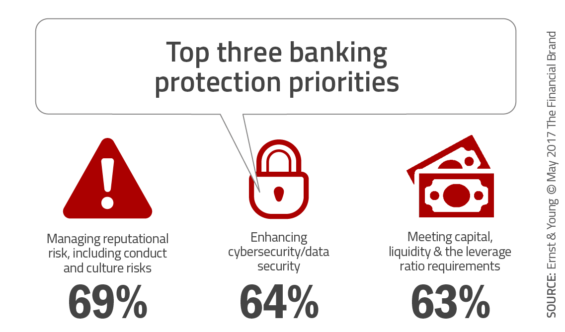

Unfortunately, there has been no shortage of banking scandals in the post-crisis era. The response has included hiring of additional compliance staff, implementing new codes of conduct and changing internal incentive structures. Despite this focus, increases in investment in cyber and data security are still needed in the majority of financial institutions according to EY.

To restore the trust of the public, additional systems must be put in place that prevent internal and external breaches. This task gets more difficult daily, as criminals seem to be a step ahead of the financial services industry. The EY survey found that, beyond managing reputational risk, a top priority is enhancing cybersecurity, which includes the hiring of a new skilled workforce, new training and investment in new regtech solutions.

4. Optimize

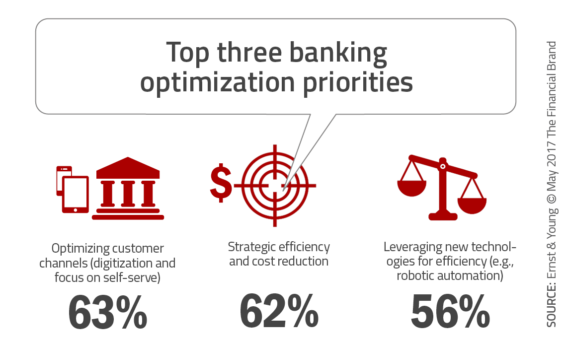

For the better part of a decade, banking organizations have focused on cost reductions. These included reducing staff, optimizing physical distribution footprint, controlling expenses and streamlining process. While these efforts resulted in a 6% reduction of expenses between 2011 and 2015, the savings were offset by a reduction in revenues of close to the same amount.

To continue the optimization process, financial institutions are continuing to focus on delivery channel optimization, reducing costs and expanding the use of new technologies, such as robotic process automation (RPA). Organizations are also working on ways to improve capital efficiency. At the end of the day, however, EY believes organizations must aggressively embrace new digital technologies.

Finally, other strategies that EY believes will improve optimization include the use of big data to improve modeling and targeting, replacing outdated core systems and investing in blockchain technology.

5. Grow

Just as uncertainty is not an excuse for inaction, the industry is now passing the point where it can blame external factors for the lack of growth or rely on them to drive growth,” says the EY report. It is time to invest in the technologies and staff that can drive innovation.

While traditional banks remain the preferred supplier of financial services for the majority of consumers, the advantages of trust and impact of complacency are beginning to fade for traditional banks. New fintech providers are catching the eye of digital-first Millennials and technological first movers that can eventually impact legacy organizations.

“New technologies are transforming business models and causing disruptions across the financial services value chain,” said Liew Nam Soon EY Asean Managing Partner, Financial Services. “Incumbents would need to move beyond conservative, incremental adjustments toward effectively implementing and executing bolder organization-wide innovation. Uncertainty in the market cannot be an excuse for inaction.”

Building for the Future

With limited opportunity for significant improvement in financial performance, and continued pressures from consumers, regulators and competitors, it is clear that doing more of the same is not a winning strategy. In fact, most organizations need to determine what business model they need to work towards and to commit the required financial and human resources to make the needed transition.

According to the EY study, banking organizations need to build a better ecosystem, not build a bigger bank. They need to reevaluate how they are organized, who they should serve, how products should be delivered and how to protect their organization internally and externally.

“The challenge to banking leaders is to be bold and move beyond incremental adjustments to broader transformations,” states the EY study. “Success will depend on the effectiveness of implementation and execution of innovation, as well as the quality of the ecosystem banks build with their partners.”