It’s been a tough year for the ATM industry. The core function of these automated tellers has always been cash dispensing. But when cash suddenly becomes an alleged pandemic “disease vector” thanks to widely circulated, but mistaken, reports of a World Health Organization statement, it caused the ATM industry great angst, coming on top of a growing movement toward digital transactions.

Oddly enough, ATMs were the first popular form of digital banking. ATMs are “an inherently phygital device — part physical, part digital,” it states on the website of the ATM Industry Association, known as ATMIA.

A major initiative of the trade group, its “Next Gen Reinvention of the ATM” will take the machines even deeper into the digital realm, and points to a bright future for the ubiquitous devices. More on this below.

Fighting the ‘Cash Carries Coronavirus’ Claim

ATMIA, which includes many financial institutions as members, is working overtime to beat back the “anti-cash” rhetoric. Association CEO Mike Lee says the anti-cash campaign uses “blatant pseudo-science to “single out cash as a supposed transmission vector for coronavirus transmission,” as Credit Union Times reported.

In a blog on the ATMIA website, Ross Clark, author of the 2017 book “The War Against Cash” explains the primary source of the belief that cash carries the coronavirus:

“In March, a comment from a World Health Organization official, advising that people wash their hands after handling cash was mysteriously elevated into [the] claim that ‘dirty banknotes may be spreading the coronavirus’ — as one newspaper put it. The WHO was later moved to disown the comments. Virologists have been largely dismissive of the idea that we are catching coronavirus from cash, emphasizing that a far more likely route of transmission between people is via airborne water droplets.” Bolstering the concern at the time of the WHO comment were reports that Chinese banking officials were subjecting banknotes to heat as a precaution.

An earlier article in The Financial Brand noted numerous studies that show cash is dirty, but in ways other than as a coronavirus carrier. In addition, mobile phone screens, as well as the touchscreens and buttons of ATMs or any similar device, are recognized as germ carriers generally. That fact, too, was singled out in the earlier stages of the pandemic. While some of the concern over coronavirus surface contamination has since diminished, ATM makers have taken notice.

NCR, for example, announced the availability of a new anti-microbial coating that can be applied to existing ATM touchscreens, keypads, handsets, card readers, cash and receipt slots, facias and privacy shields — of any machine, not just theirs. The coating must be reapplied after six months, according to NCR.

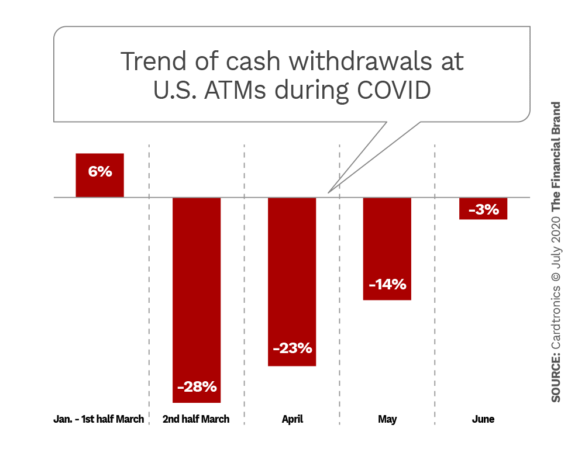

After a rush of cash withdrawals early in March as the COVID-10 crisis first began ramping up in the U.S., the fears about cash contagion combined with government-mandated closings of stores and restaurants caused ATM cash withdrawals worldwide to plummet (as much as 60% in the U.K.). In the U.S., fewer consumers stopped withdrawing cash and have been quicker to return to the habit, as Cardtronics data show.

Cardtronics, which operates 285,000 ATMs worldwide including 55,000 in the Allpoint Network in the U.S., says one sign that cash usage remains strong is that since the beginning of June “total cash dispensed at our U.S. ATMs on a same-unit basis is up nearly 10% versus June the last year.” Locations outside the top 20 metro areas in the U.S. were doing better than the biggest markets, the company states.

NCR reports that new patterns of cash withdrawals have been formed that financial institutions should take into consideration when forecasting their cash needs. For example, the company is getting reports of reduced transaction frequencies, but increased withdrawal values. Cashing out stimulus payment cards may have impacted this.

Read More: Retail Banking Without Branches: 7 Critical Elements of the New Reality

Part of a Modern Digital Banking Strategy

Although ATMs are still primarily used for cash withdrawals, the reality is that the machines have evolved greatly in recent years. They sit at the intersection of digital and physical and can be both “in the branch” and function “as the branch,” states Juergen Kisters, VP of Banking Marketing at Diebold Nixdorf in a Payments Journal blog. Their technology now is similar to a smartphone, more app-based and open-sourced, he states, enabling developers to write programs to be used on ATMs.

As a result, the more modern ATMs can track consumer data, like a mobile phone, at the same time they conduct cash-based transactions, like a teller.

ATMIA’s Next Gen ATM project, begun in late 2018, has several hundred participants, the organization states. “Next Gen is basically a way to move the ATM into a mobile environment,” Donna Embry, SVP Global Payments Strategy at Tennessee-based Evolve Bank & Trust told Mobile Payments Today. “As banks and consumer switch to online and mobile channels, this project enables ATMs to adapt to that changing environment.” Embry has been actively involved in the project.

The ability of consumers to use mobile wallets and contactless cards to “pre-stage” or initiate ATM transactions (broadly referred to as “cardless ATMs”) means the ATM experience is becoming less seamless than when it was entirely card-based, Embry explains. It’s much like the early days of ATMs when consumers had to find a machine that accepted a particular debit card or network. The Next Gen program aims to ensure the cardless ATM experience is seamless, she states. But a significant additional benefit is that because the program is app-based, it will enable a much wider array of banking services to be easily added to ATMs, such as currency conversion, gift card purchases, or cryptocurrency, without requiring software upgrades.

“Next Gen will turn the ATM into more of a self-service machine for all of the financial services and payment needs for the consumer,” Embry states.

This dovetails well with the impact of the coronavirus on branch banking. Banks and credit unions are slowly and carefully reopening branches to in-person traffic, but many observers and banking executives believe branch limitations of one sort another will remain for an indefinite period. More advanced ATMs, once they are more widely deployed, can help offset the limitations.

“From ID checks for loan applications to customer service video chats, the ATM of the future is set to help bridge the gap left by the closure of many full-service bank branches,” Matt Phillips, VP and Head of Financial Services for Diebold Nixdorf in the U.K. and Ireland, told the PA News Agency.

Although the ATMIA Next Gen project will take several years to be fully implemented, according to Embry, various ATM manufacturers already have advanced models that can be equipped with fingerprint scanners and NFC readers, as well as being able to handle automated (envelope-free) deposits of cash and checks and cash recycling capabilities. The latter two capabilities are increasingly becoming a basic requirement for any bank or credit union ordering new machines.

Interest in Cardless ATMs Growing

According to Mastercard, 78% of consumers would rather use a cardless ATM solution than carry a physical card, PaySpace Magazine reports. That survey was conducted pre-COVID-19, so the main reason cited for the preference was convenience. Safety concerns related to the coronavirus may well have further increased the interest in cardless. The PaySpace article lays out some of the basics of cardless ATM technology, noting that it is currently being used by Bank of America, Wells Fargo, Chase, Capital One and Fifth Third Bank.

Reflecting Embry’s point about seamless acceptance, the type of cardless ATM technology now in use varies by institution. Some use a scanner to read unique QR-codes, others require a verification code sent by SMS, while the most sophisticated ones can authenticate users by facial features or palm scan, according to PaySpace. Mobile wallets can also be used when the ATM is equipped for NFC reception.

Spain’s CaixaBank has used facial recognition technology on about 20 ATMs since early 2019. The biometric authentication capability lets consumers withdraw cash without a PIN. In June, the bank announced it is adding another 100 machines equipped with facial recognition, ComputerWeekly reports.

“In the current context of COVID-19, this project is particularly relevant given that it enables us to reduce the physical contact of customers with ATM surfaces,” says CaixaBank CEO Gonzalo Gortázar. “This measure comes in addition to using contactless cards, which contributes to promoting safe terminal use.”

Some cardless ATM applications allow person-to-person sharing. A consumer can send a one-time code to another person’s mobile phone allowing the other person to withdraw a certain amount of cash from the sender’s account.

One cautionary note: Banks or credit unions that implement cardless ATM capability will need to regularly warn users against fraud attempts. Phishing scams already are targeting these newer technologies.