Financial marketers attempting to improve customer experience find themselves in the midst of a perfect storm. On the one hand is the continuing impact of the COVID-19 pandemic and the ongoing social upheaval. On the other is the ongoing technological revolution on multiple fronts that can literally drown them in tidal waves of data.

At its best, the science of customer experience can improve the performance of products and services that consumers obtain from banks and credit unions. But it can also take an institution down multiple wrong paths.

Analysts at Forrester recently came together — virtually — for the company’s CX North America event to explore this multifaceted challenge at a time when some basics about CX are being reexamined for multiple reasons.

“Past experience is not a great guide to how consumers will respond today,” said James McCormick, Principal Analyst.

Never have so many data points and so many tools been at the disposal of financial marketers, but at the end of the day, CX and all that goes into it is not the goal.

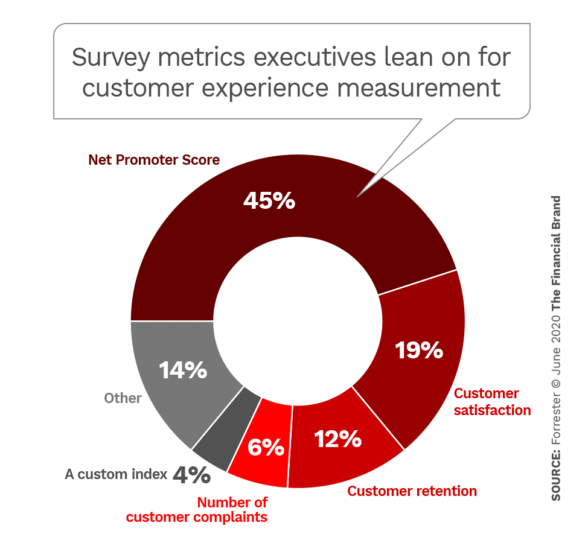

“The challenge is that none of the metrics about CX tell you whether good customer experience is helping your business fatten its wallet,” said T.J. Keitt, Principal Analyst.

Happy consumers can be a wonderful thing, but the annals of American business are strewn with companies that made people happy but are broke and gone. Keitt pointed to Borders, which featured pleasant coffee bars and a library-like atmosphere.

Bibliophiles loved Borders. It went out of business in 2011, clobbered by Amazon.

Thanks, But I’d Just As Soon You Didn’t Know Me All That Well

One of the core beliefs of the CX fraternity today is that people will happily surrender personal data because they think that doing so will enable them to have great service. Data provided and data observed — think Amazon — represent much of the raw material of CX personalization. However, there’s another side to it.

“We get so entranced by what we could do that we forget to stop and ask if there are things that we should not do,” said Melissa Parrish, Vice President and Group Director. While marketers work to gather more data with which to serve consumers, “customers tell us they want more anonymity.” She cited Forrester research that indicates that only 27% of U.S. adults online are willing to let retailers use their personal information to tailor their experiences.

Most, she continues, like some level of personalization, but this can be very individual. “You have to figure out what your customers want and be prepared to deliver that,” she explained. “There are people who don’t want you using their data at all and I suggest you take that seriously. Use that data to create a segment where you don’t personalize at all.”

This idea is foreign to many marketers, but Parrish said the Trader Joe’s grocery chain is an example, in that it doesn’t personalize at all. In fact the chain does very little marketing.

Read More: Personalization in Banking Can’t Be Disguised as Cross-Selling

Personalization and CX Research Must Move Beyond Traditional Surveys

A mainstay of defining CX for years has been the consumer survey, designed to tease out all sorts of things about consumers’ relationship with brands. However, “we are past the peak of survey effectiveness,” said Maxie Schmidt-Subramanian, Principal Analyst. “It’s time to kick the habit and learn new habits. Customers are starting to not respond to surveys.”

The analyst added that a sufficient number of people dislike and won’t take surveys that marketers must ask if those who still respond aren’t a skewed sample.

People are so busy that they often resent the typical 20-minute survey, said Jhumur Choudhury, Research Lead at ATB Financial, in Alberta, Canada. She believes that in persisting with this tool, “we aren’t being good customer relationship professionals — we aren’t demonstrating empathy as researchers.”

Choudhury said that as time went on she increasingly trimmed the use of long surveys.

One way is to shorten them drastically to cover only must-know queries, and to build in some open-ended questions to try to get at what is really on consumers’ minds. For example, in asking about customer satisfaction, if a consumer cites past unhappiness with employee service, the researcher would now ask, “Can you state an instance of that kind of behavior?”

Another tactic, beyond cutting questions, is to re-script interactions so they are played out as customer conversations, not as rigid survey interviews. Choudhury said this doubled responses and resulted in more useful feedback. Beforehand, she said surveys often produced “rows and rows of unactionable data.”

Choudhury said research can also be made less painful for customers by taking advantage of syndicated research available in the market. This data can be used as a baseline, and custom research can then be confined to gathering the specific details only customers can provide about themselves. She said this has been especially helpful in conducting research among farmers, with syndicated studies forming a backdrop to fewer but focused questions from ATB.

“Supplement the purchased information with qualitative information,” she said.

Choudhury has also found that simply going to ATB’s financial centers and chatting with customers here and there yields many insights. “I’m just talking with them and observing them in their natural surroundings,” she explained, “not even with any particular research objective.”

In-depth queries can still be built with the cooperation of willing groups of customers. Choudhury says ATB has cultivated a customer advocate committee, of roughly 100 people, to put specific questions to.

And she also taps an often overlooked source: employees.

“Our front-line staff often knows so much about what our customers’ problems are,” said Choudhury, “but that knowledge often isn’t distilled up to the strategic level.”

Read More: How Banks & Credit Unions Can Turn Good Service Into Awesome CX

Finding Your ‘Fanbase’: What Creates and Maintains ‘Devotees’

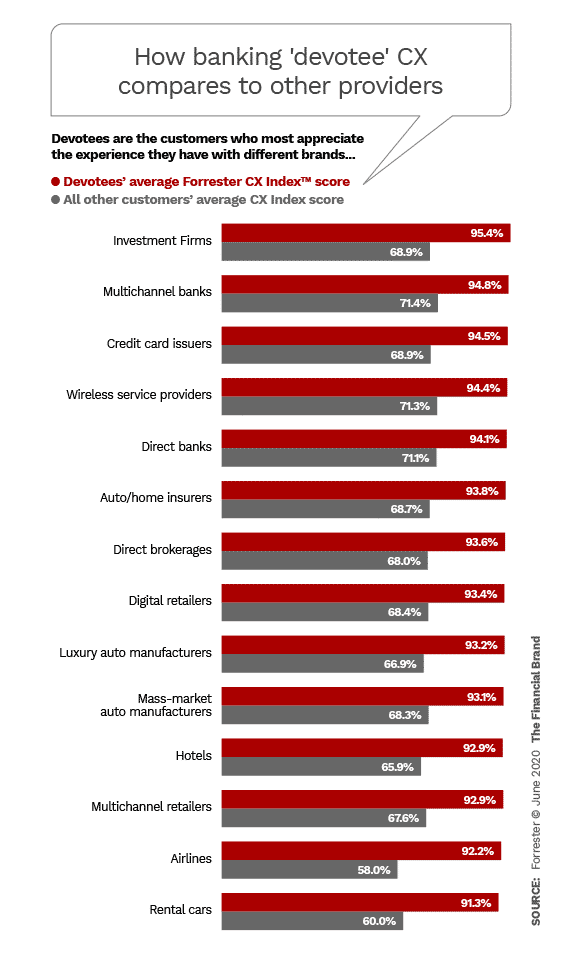

A key element of the popular Net Promoter Score is that it focuses on success leading to success. But even more generally, strong CX should have a multiplier effect, according to T.J. Keitt.

“If your customers buy into what you are doing, they should be buying more,” said Keitt, “and they should also be bringing you other customers.”

Keitt led the Forrester U.S. Customer Experience Index 2020. He noted that every industry has its share of fans of specific institutions. Some industries may see comparatively small impact from “devotees,” the firm calls them, but in other cases these consumers may make up a third or more of the industry customer base.

Keitt said devotees share these characteristics:

- They are willing to forgive you when you make an error — especially important as companies adapt to the “new normal.”

- They will pay a premium to be your customer.

- They will go out of their way to do business with you, even if it is convenient.

- They will consistently bring more business to you than others.

How do you develop devotees? Keitt recommended starting with these key questions:

- Does our business have a value proposition that creates devotion?

- Do we have the data assets that would reveal our devotees?

- What analytical skills do we have to uncover our customers’ devotion?

- Can our business ecosystem help us create more devotees?

Segmentation: You Can Only Use One Style at a Time

What is a Millennial? Other than the definition by range of birth years and some shared characteristics based on the time and environment in which they grew up, the Millennial generation consists of many different types of people.

Showing his audience a range of photographs of Millennials in many different forms of dress and activities, Brandon Purcell, Principal Analyst, made the point that for many purposes traditional customer group segmentation won’t fly anymore. Each person among the photos may have grown up in the same general period, but there is much more about them that defines them than that alone.

Segmenting consumers by demographics and behavior is more traditional, Purcell noted, and it generates plenty of data — but much of the data is static. The sources include sales, customer chats, big data sources, lead generation, social testing and more — but it is sliced and diced based on age and related factors.

Another means of segmenting prospects and customers is by their attitudes, emotions, beliefs and values on a given matter — psychographic data that transcends consumers’ age alone.

Where Purcell believes marketers err is trying to overlay attitudinal segmentation on top of demographic segmentation, hoping to come up with personas to define potential marketing groups to target. This is done in an effort to personalize marketers’ approaches to individuals, he said. A key reason this melding of approaches is challenging is that organizations don’t have full attitudinal data on each consumer, which yields an incomplete picture when brands are trying to match that to traditional segmentation data.

Purcell said one financial firm he knew of — an insurance company — tried this dual approach. The intent had been to segment people by their insurance needs. Purcell said the company’s segmentation team created a set of customer types after a long spell of focus groups and surveys. The team presented the concept to company leaders. Then one asked how many of the firm’s current customers fell into each group.

No one could say. Almost a year was spent attempting to find an answer, but in the end the best that the team could devise was a model for predicting behavior. It was right in only one out of three test cases.

The entire project was shut down.

Attitudinal research can help identify people who could be reached with certain appeals for a product or service based on what they are looking for from the product. Purcell spoke of efforts to sell tea to young people and said research found two dominant groups: people who saw tea as an energy boosting beverage and those to whom how the tea was raised and sold made the greatest difference. Lipton markets black tea as “Natural Energy” in K-cup pods, while Twinings sells fair trade tea that is raised sustainably. Each serves its niche.

Traditional segmentation tends to support a mindset of driving consumer behavior, Purcell explained, while personalization is designed to improve results, ultimately, by improving the customer experience.

Segmentation marketing approaches tend to be measured by factors like customer satisfaction rates, conversion rates and retention rates — all quantitative measures. By contrast, personalization concerns “the overall interaction you are having with the customer,” said Purcell. “It’s from the outside in: What is the customer trying to achieve with us as a brand?”

Read More: Banking Needs 360-Degree View of Customer Journey

Using Data Effectively May Be More Than Your Brain Can Take

The great thing about increasing digitization of commerce, including banking, is that so much more is measurable. The scary thing about it is that so much is measurable.

“Data is being generated too fast to manage,” said McCormick, “and it’s only going to get worse.”

The age of digital marketing is about two decades old, now, said Jim Nail, Principal Analyst, and the idea of using it to market to the right person in the right place at the right time — a key form of personalization — has achieved the status of a meme. However, Nail continued, “we are still struggling with some pretty basic data management issues.”

In fact, so difficult can it be to pull together data to form a good conclusion, said McCormick, that the frequent result is “a dog’s breakfast,” instead of a set of useful insights. The pair suggested four practices to improve this situation.

1. Automate your data feeds.

In this era trying to tap data manually makes no sense, according to Nail. APIs — application programming interfaces — can be used to route raw data into more useful forms and places. Nail acknowledged that a risk exists of data being misrouted. However, he said machine learning and artificial intelligence can be used to spot anomalies and then fix them.

2. Eliminate blind spots by connecting data.

McCormick says fresh marketing concepts can flop for reasons that have nothing to do with the idea itself. Instead, delivery may be an issue, but marketers won’t know it unless they have a full picture.

“Measure content, context and performance,” said McCormick. “You can’t afford to lose customers by being blind to sub-optimal experience delivery.” A malfunctioning or hyper-slow mobile app, emails that continually get blocked and similar factors must all be correlated before correct conclusions can be drawn.

3. Identify and optimize leading indicator metrics.

Nail suggested that some reverse engineering can help, in the sense of looking at successes, and then working backward to see what characteristics were seen early on. Behaviors that consistently correlate with desired outcomes can be tracked early. These could include downloading certain types of content or engaging with a chatbot at a specific point.

4. Experiment to learn what to do in these crazy times.

COVID-19, social upheaval, electoral politics of a new order, none of this makes for business as usual.

So McCormick said not to be afraid to try new things, testing as you go.