At a time when U.S. consumers are increasingly becoming comfortable with branchless banking and alternative financial providers, is there room for alternative digital-only banks with zero name recognition? Recent announcements by Germany-based N26 and U.K.-based Monzo that they will be entering the highly competitive U.S. in the next few months will provide a good test of the viability of foreign-based banking competition.

Despite European experiences that proved that a challenger bank can generate interest and users with the help of significant funding and well-done marketing, can this success be duplicated in a market that is oversaturated with banks and credit unions? Further, can new entrants provide significant differentiation from the U.S.-based digital-only banks or mobile offerings from legacy banking organizations?

Read More:

N26 Invites 100,000 Wait-Listed U.S. Consumers To Open Accounts

According to N26, there will be a staged rollout beginning immediately, with the 100,000 people on the U.S. wait list being invited to sign up and have full access to the product. Any interested consumer can sign up using their mobile device in under five minutes.

There are no account maintenance fees nor minimum balances required. The account is the same as a traditional checking account, with ACH payments, routing and account numbers. N26 says they will automatically reimburse 3rd party ATM fees.

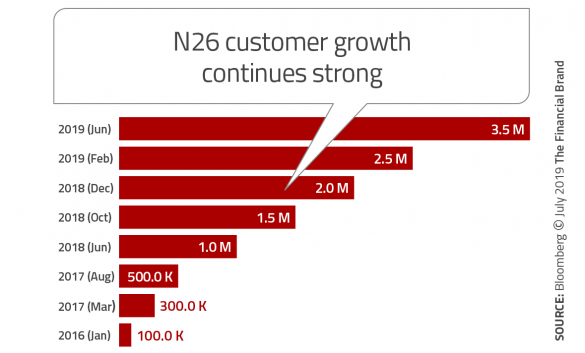

Since the 2015 European product launch, N26 has generated 3.5 million customers in 24 European markets. Currently, the N26 app is generating over 10,000 new users daily based primarily on word of mouth. The N26 app continues to be very highly rated by consumers.

Similar to many well-designed mobile banking apps, account activity is displayed within the app in real time, with individual transactions instantly categorized. Customers can also set daily spending limits, and lock and unlock their debit card within the app.

Also, similar to most digital-only challengers in the U.S., N26 has avoided a cumbersome banking license process by partnering with a FDIC-insured financial institution based on the U.S. In this case, Axos Bank will be the white-label partner for N26.

One of the benefits targeted to the highly mobile European customer is that there are no foreign transaction fees when making purchases internationally. This is not as strong a differentiator for an American consumer who travels far less often internationally.

The N26 account also has a unique feature (Spaces), where sub-accounts can be created similar to the way consumers used to use envelopes for special financial goals. Transfers between the account and Spaces can be initiated within the app or be automated by the customer.

N26 is also planning expansion beyond their basic account in the U.S. The company says that it plans to roll out two premium plans — N26 Metal and N26 Black in coming months.

“The U.S. launch is a major milestone for N26 to change banking globally and reach more than 50 million customers in the coming years,” says Valentin Stalf, Co-Founder and CEO, N26. “We know that millions of people around the world and particularly in the U.S. are still paying hidden and exorbitant fees and are frustrated by poor banking experiences. N26 will radically change the way Americans bank as it has for so many people throughout Europe.”

To support the expansion into the US, N26 has raised more than $500 million from outside investors, including U.S.-based firms Insight Venture Partners and Peter Thiel’s Valar Ventures.

Is Monzo the ‘Bank of the Future’?

Referring to itself as the “bank of the future,” Monzo has also begun marketing efforts in the U.S., hoping to disrupt the traditional banks and credit unions in a way similar to what they have done in the U.K. Valued at more than $1 billion, Monzo has a mobile-only customer base in the U.K. of 2.2 million customers.

Similar to N26, Monzo has grown quickly because of functionality that is best delivered on a digital-only platform. For instance, the immediacy of transaction verification and posting, simple ways to track and manage spending, and easy ways to send money and split bills with other Monzo users. There is even the opportunity to set up smaller, goal specific “saving pots” of money, as is offered by N26.

While one of the differentiators of the N26 account is the elimination of international transaction fees, Monzo is probably best known for their exceptional customer service and community engagement events where questions are answered face-to-face. According to sources, Monzo is planning similar events in Los Angeles, New York City and San Francisco as part of its scaled introduction.

Monzo will also have contactless debit cards, which is a much bigger deal in the U.K., where 64% of cards are contactless (according to AT Kearney). Despite the ease of use and benefits to the consumer, less than 5% of U.S. cards are “tap to pay.” A potential hurdle initially may be that Monzo is not ready to support Apple Pay or Google Pay (this is offered in the U.K.).

Similar to N26, Monzo will not have a U.S. banking license initially. It is partnering with Sutton Bank to provide deposit insurance. However, Monzo CEO Tom Blomfield indicates the challenger bank wants its own banking charter. The bank also does not offer lending solutions at this time, while it does offer services like insurance in the U.K. Because of the different regulations around Open Banking in the U.S., it is not yet know what additional services may be offered by Monzo.

Should U.S. Banks Be Scared?

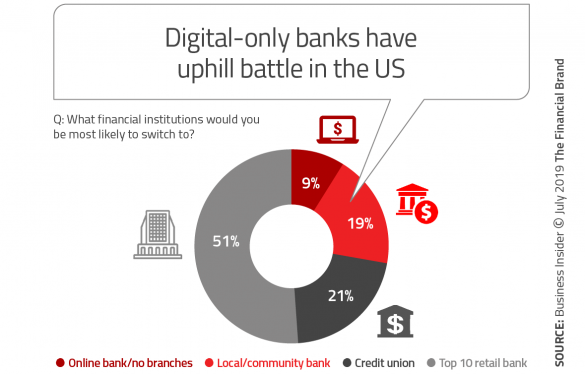

It is far too early to determine if N26, Monzo or any of the fintech banks from other countries can duplicate the growth rates they have achieved on their home turf. In countries where these challenger banks first set up shop, the competition is nowhere as expansive as it is in the U.S. Not only are there banks and credit unions of all sizes in the U.S., but there are also digital-only banks such as Chime and Varo Money, big tech players like Amazon, and specialty digital players like PayPal all vying for market share..

In other words, winning in the U.S. will not only require a highly differentiated product, but far more financial resources than was required to generate growth overseas. There is also the reality that U.S. banks will not be complacent if any of the new entrants build a following – Chase, Wells Fargo, Bank of America and many regional banks have far deeper pockets than the new challengers.

But, the biggest challenge will most likely come from the U.S. consumer. Despite saying they don’t “love” their bank, they have shown an amazing level of complacency towards moving their primary checking account. For the most part, this level of loyalty is actually a matter of trust. Most customers still trust the bank or credit union they do business with.

In fact, even in Europe, it is believed that much of the growth achieved by the challenger banks has not been at the expense of the legacy financial institutions, but instead being associated with the establishment of secondary accounts.

That said, legacy financial institutions cannot afford to take these new digital-only banking threats lightly. If U.S. banks and credit unions do not continue to develop new digital solutions, they risk the potential loss of more consumers beyond what has already been lost to digital payment, loan, investment and credit card organizations.

In other words, legacy financial institutions could still be the big losers. On the other hand, it is hard to imagine a scenario where the consumer doesn’t become the big winner, with lower costs, expanded options, new solutions and increased innovation.