It has been nearly a century since Henry Ford wrote “Any customer can have a car painted any color that he wants so long as it is black,” in My Life and Work.

At the time, 1922, the realities of mass production required a single product for all buyers. In the years since, U.S. consumers have increasingly been offered a flood of product choices in every area imaginable.

Banks, credit unions, and other financial services providers have hopped aboard this trend too. From any computer, consumers can apply for a credit card marketed to people who eat out frequently, purchase a cryptocurrency named after their favorite domestic animal, or make thousands of other more or less responsible financial product decisions.

The conventional wisdom holds that giving someone more options means their choices are better.

But are their choices really better? Or just hopelessly complicated?

Studies have found that “choice overload,” with accompanying feelings of anxiety and dissatisfaction, frequently appears around important decisions. Financial products are no exception, and if you offer accounts online your applicants may be struggling — and quitting — due to choice overload.

As an example, studies of 401(k) plans reported in the Journal of Financial Services Research have found that while wealth and income increased the odds of participating in a 401(k), increasing the number of mutual funds offered had a negative effect on participation.

“Increasing the number of options makes individuals not only less likely to invest but also more likely to pick conservative options…that over the long run lead to lower returns,” observed Alexander Chernev, Associate Professor at the Kellogg School of Management, Northwestern University, in a white paper for the Filene Research Institute.

Too Many Ways to Compare

The feeling of choice overload is particularly likely to appear when someone is offered a selection among products that all differ in several ways.

“Choice overload may be hard to measure, but financial institutions must take it seriously or risk losing business by exhausting potential customers.”

Chernev, who has done much research in this area, and other experts working with him have found in research in the Journal of Consumer Psychology that in addition to the problems created by offering many options, making a choice is even harder when those options can be compared in many different ways.

For example, when faced with accounts that offer special interest rate features, automated round-up savings, varied fees, and more, simply choosing the right account to apply for is a multi-faceted challenge for the typical applicant.

Choice overload may be hard to measure, but financial institutions must take it seriously or risk losing business by exhausting potential customers.

Read More: Financial Marketers Must Ditch ‘Bank Speak’ to Boost Usage of Mobile Banking Apps

Ways to Relieve ‘Choice Overload’

In some cases, choice overload can be addressed by improving the interface a consumer uses online or mobilely to review an institution’s offerings.

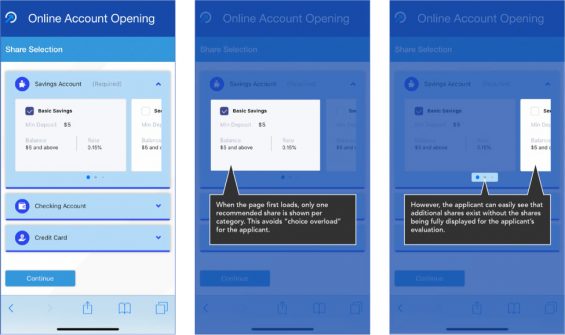

The interface approach reproduced below clearly separates account categories so that only a single kind of account (like checking or savings) needs to be considered at a time. It also reduces the total number of account options visible at a time.

Because only one account per category is visible on the mobile device, it is easy to highlight recommended accounts while still providing a natural swipe-based approach for viewing others. Such improvements can reduce the probability of abandonment. My firm has found such approaches can reduce this problem by as much as 33%.

Another way to reduce choice overload is reducing the amount of data used to compare accounts. Chernev and his fellow researchers found that using just one attribute when comparing items “is likely to be less cognitively taxing than choosing from a set of items described along multiple attributes.”

So, for example, if offering Certificates of Deposit, an institution can consider using only term and interest rate to distinguish the CDs being offered. This would mean, at least initially, skipping the specialty options such as the jumbo CDs, CDs with a one-time interest rate bump, and other complex variations on this basic account type. The researchers also report that “adding an inferior option that enhances the dominance of one of the existing options has been shown to increase the likelihood that a choice will be made.”

So, testing a deliberately inferior checking account is an interesting, if unorthodox, idea. (Of course, marketers must work out such experiments with the Compliance Department.)

Read More: Crafting Amazon-Like Banking Experiences Easier Said Than Done

When You’ve Got a Menu Over-Stuffed with Choices

Over time, banks and credit unions can accumulate a large collection of possible account types. Factors leading to such “inventories” include options incorporated in the course of mergers, and, today, even mergers on mergers.

If your institution currently offers a large number of different account types, housecleaning — which can be a good idea — may be tempting. However, you don’t necessarily have to discontinue many of them to avoid choice overload.

Try Some Personalization. Create personalized offerings so that prospective members or customers see a limited set of accounts based on their particular needs. Thus small business owners, students, and others could see choices narrowed after they tell the institution something about themselves.

Chernev states that such personalization enables “companies to offer smaller assortments while reducing some of the negative consequences of restricting consumer choice.”

Create Account Bundles.Bundling your offerings together can help simplify them. Offering a small number of combined checking/savings account bundles, for example, may be easier for consumers to choose among than comparing savings accounts, and then comparing checking accounts, in two different, possibly frustrating, steps.

These sorts of changes lend themselves to experimentation because no product types need to be closed or modified. This can be accomplished by setting up multiple account-opening experiences and running A/B tests to see how well personalization or bundling work for your institution.

Co-Applicant Process Needs Work

Choice issues leading to mental overload are not limited to deciding what kind of account to open. My firm’s analysis shows that a major point at which a choice can lead to a negative result is when, as part of the application process, a financial institution offers the ability to add a co-applicant.

We find that 77% of applicants who have entered their own personal info into an application complete the process of opening an account. However, for those who add a co-applicant directly after that point, the completion rate drops to 50%.

The change in completion rate is not caused simply by making the process longer — when applicants choose to add a beneficiary, lengthening the application process, 83% of them complete the process. Clearly, co-applicants — a credit consideration — represent a unique challenge.

How can an institution resolve the co-applicant problem without totally removing joint accounts from the application?

Some more in-depth reconfiguration may be a good bet. If your online account application allows your to re-configure workflows, consider changing at which point co-applicants provide their info. For example, what if you could onboard the primary applicant before offering the ability to create a joint account? If the primary applicant has to complete their application entirely before the co-applicant starts, the issues with co-applicant abandonment should not stall that primary applicant from joining your institution.

More Stumbling Blocks Can Sidetrack Account Opening

Account selection and adding a co-applicant are just two of the numerous choices consumers must make while applying for accounts, and potential new relationships can be discouraged when consumers encounter other pitfalls that cause them to abandon their enrollments.

Some causes can be compliance related. For example, when an applicant is asked “Are you subject to IRS Backup Withholding?” there’s likely to be a high level of uncertainty. (“What does ‘backup withholding’ mean?” “If money’s withheld from my paycheck, is that ‘backup withholding’?”).

The implication that legalities are involved can tip the balance towards abandonment. Even though that backup withholding questions seems to be a simple yes-or-no matter, it’s not an easy choice — and given tax compliance requirements, not one that financial institutions can avoid.

Since you’ve likely got to ask compliance-related questions like this one, how can you make them less bothersome? Consider providing guidance about how to decide how to answer the question.

For IRS backup withholding, a note like “If the IRS hasn’t directly contacted you about unpaid taxes, this does not apply,” can help ensure this question doesn’t cause confusion and worry. And in required areas with many options — one example might be credit union membership eligibility — consider marking one way of being eligible as “most common.” This can help point applicants in the right direction.

Read More: Make It Simple: Credit Card Marketing Confuses Consumerse

Ask Questions Now So Consumers Have Fewer Later

However you choose to avoid choice overload, make sure to rigorously test your proposed solutions. Hoping for the best is a poor substitute. Consider:

- Can you tell how many people quit while interacting with your IRS backup withholding question?

- Do you know what percent of applicants drop out while looking over account choices?

- And if you have this information easily at hand, can you run A/B tests to make sure your changes are indeed helping people open more accounts?

Much as we may love lots of choice in the cookie aisle, giving consumers too many options in financial services isn’t necessarily a good thing. But if your bank or credit union is already offering a huge range of alternatives, proceed carefully. Changes take time, and no financial institution can afford guesswork that might lead in the wrong direction.