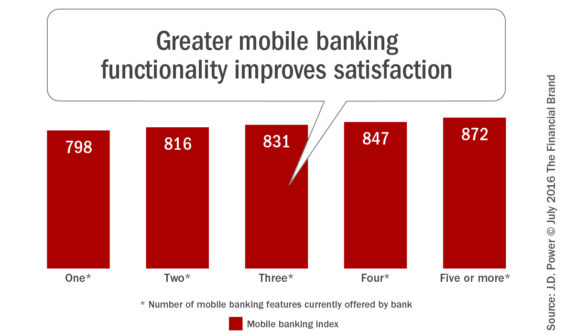

Since 2011, the usage rate of mobile banking apps has increased exponentially. Not only has mobile banking usage increased, but satisfaction with the mobile channel has also improved. In fact, mobile banking has surpassed all other channels and has become the most satisfying interaction channel, according to J.D. Power.

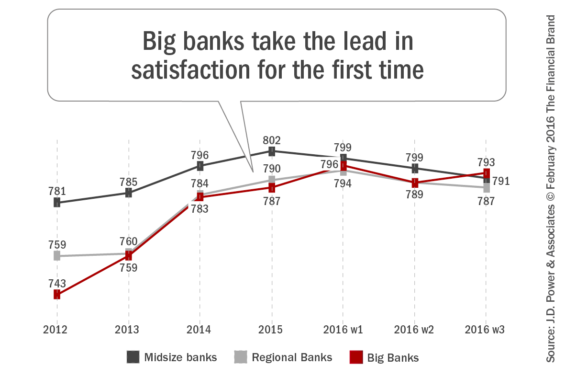

In line with this growth in mobile banking usage, the commitment to becoming a ‘digital bank’ is beginning to pay significant dividends in several key areas for some of the largest financial institutions. This was first seen in the J.D. Power 2016 U.S. Retail Banking Satisfaction Study, where the biggest banks had significantly improved in overall customer satisfaction, primarily due to digital offerings.

“The impact of the large banks’ (i.e., Bank of America, Chase, Wells Fargo) mobile banking strategies can best be seen by looking at bank satisfaction numbers among Millennials, stated Ron Shevlin, director of research at Cornerstone Advisors. “The large banks’ satisfaction scores increased by more than 50 points between 2012 and 2016, and is now slightly higher than the scores for both regional and mid-sized banks. Why? Increased investment in digital delivery by the largest banks has to be one important reason.”

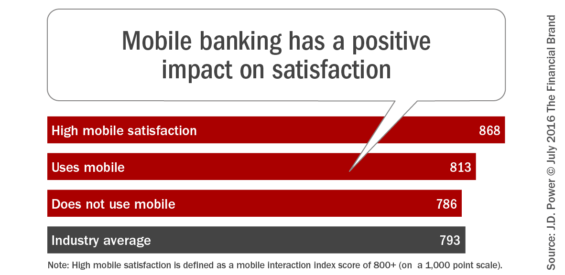

This is confirmed by the J.D. Power research that showed that there is an immediate lift in overall satisfaction when customers use mobile banking (+27 points on a 1,000-point scale), and this impact increases even more when banks provide their mobile banking customers with a highly satisfying experience (+82). According to J.D. Power, “The outlook for Big Banks remains positive, driven by their (big banks) ability to invest in customer-centric innovations (e.g., digital channels, analytics, and branch transformation), as well as their success in growing customer segments.”

Digital Investment Drives Mobile Usage

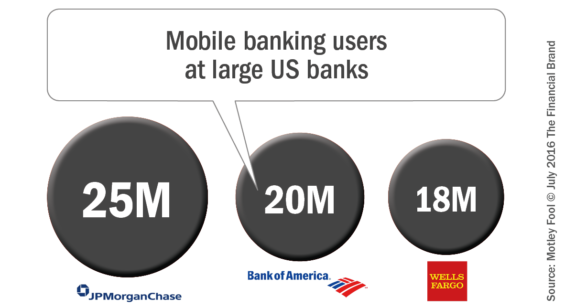

Recent disclosures of mobile banking use by the big banks provides a glimpse of the impact of digital investment on mobile use. Of the three largest U.S. banks, JPMorgan Chase leads the way with nearly 25 million active mobile customers as of the second quarter. That was up 18% compared with the same period last year. Bank of America had the second most active mobile users, with 20.2 million monthly active app users, with Wells Fargo reporting 18 million active users. (These numbers are aligned with the relative size of these banks’ balance sheets.)

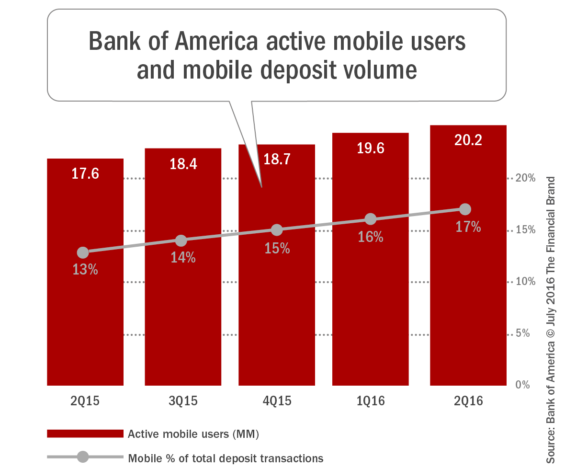

Usage continues to increase among all demographic segments. However, mobile banking is especially critical to customers in the Emerging Affluent segment, who are the heaviest users of mobile services overall and most likely to make mobile deposits. The impact on mobile deposits can be seen in the results of Bank of America, where mobile deposit growth mirrors mobile bank usage, and now represent 17% of all deposit transactions at the bank. This volume of mobile deposits is equivalent to 800 financial centers, with each mobile deposit costing Bank of America 90% less than an in-branch deposit.

Digital Investment Drives Channel Shift

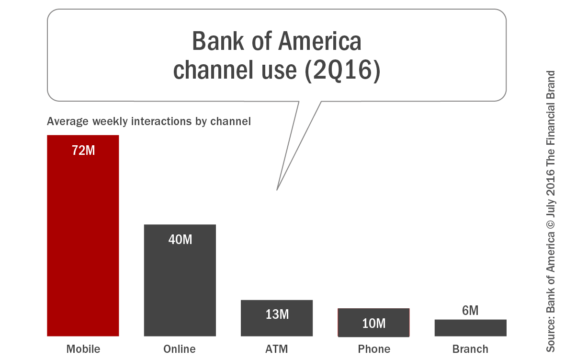

As more households download digital applications and use their mobile apps more frequently, it is transforming the way people think about banking. No longer is banking correlated with a ‘trip to the branch’. Increasingly, banking is done as a part of daily life. As can be seen from Bank of America’s most recent report on channel use, the bank’s mobile app is 12 times more popular than its branches. Consumers accessed its mobile app an average of 72 million times a week in the second quarter, compared with to average of only 6 million weekly visits to its physical branches.

Wells Fargo is seeing similar channel shift. “The mobile offerings are our fastest-growing channel now; 18 million of our 20 some million households now have used that and sometimes – most times – as their dominant channel,” explained Wells Fargo Chairman and CEO John Stumpf on the bank’s second-quarter conference call.

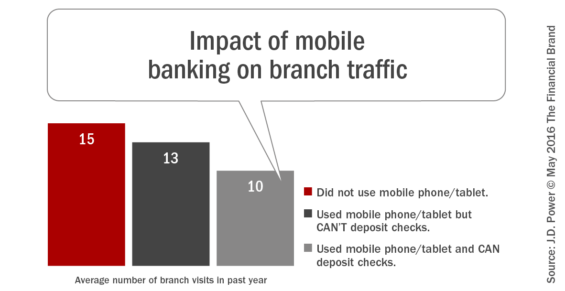

The shift in physical branch use because of mobile is not just a big bank phenomenon. J.D. Power found branch visits can be reduced by 33% if a customer is encouraged to use mobile banking and use their phone to deposit checks.

“Every statistic on branch activity and retail consumer revenue-in-branch is in decline right now, most in rapid decline, states Brett King, best-selling author, host of the Breaking Banks radio show and founder/CEO of Moven. “There’s no magical shift in customer behavior that’s likely to reverse that trend, if anything there’s evidence it’s accelerating. Given most retail banks are fully reliant on branch revenue for survival, this creates massive uncertainty.”

Digital Investment Increases Customer Acquisition and Cross-Sales

Investment in digital channels, specifically the mobile channel, is also impacting the ability to grow a bank’s customer base. Banks and credit unions with the most user-friendly and functional online and mobile platforms have a significant competitive advantage when it comes to attracting, retaining and satisfying customers.

Bank of America was ranked No. 1 in both mobile banking functionality and digital sales functionality by Forrester, with the other two largest banks (as well as USAA) consistently outperforming most rivals in the marketplace. The improved functionality has a direct impact on customer satisfaction and improved differentiation in the marketplace, according to Accenture.

Based on 2Q16 earnings reports, the investment in digital channels has allowed the largest banks to outperform the industry in growth of retail checking accounts. For instance, Chase Bank reported YOY customer growth of 2 million households, with average deposits increasing by 10%. For Bank of America, average deposits grew 8%, with their digital sales increasing by 12% YOY (representing 18% of total sales). Finally, at Wells Fargo, consumer checking accounts increased by 4.7% YOY. Much of this growth is attributed to the availability of top-rated digital apps.

Beyond direct sales and cross-selling of services, Bank of America is making headway with integrating physical channels with digital delivery. According to their most recent earnings report, the use of the bank’s digital appointment application has increased by more than 140% since the same period last year, allowing for a truly optichannel™ experience. They have also introduced 2,800 cardless-enabled ATMs this year.

Digital Investment Reduces Costs

According to an Accenture report, banks employ approximately 514,000 tellers and pay them an average yearly wage of $25,760. Additionally, there’s the high cost associated with building and maintaining branches, which usually allocate up to 50% of their space to teller-related activities. Because of these expenses, it’s up to 95% cheaper for a bank to process a deposit digitally than through a teller, and online and mobile payments cost 65% less than payment by a paper check.

The bottom line is that mobile banking can free up valuable labor and branch space, which can have a significant impact on the bank’s balance sheet. These cost savings come at a time when banking is saddled with increased costs related to regulatory requirements and when low interest rates are impacting a banks’ ability to grow their top lines.

According to the most recent investor reports, Bank of America’s non-interest expense of $13.5 billion is 3% less than it was a year ago and is the lowest since the fourth quarter of 2008. The bank also has 6,000 fewer full-time equivalent employees than last year, which has led to increased efficiency. Bank of America is also replacing paper statements with electronic statements, and is converting several back office platforms to less labor intensive digital platforms.

Digital Investment is Changing the Future of Banking

As can be seen, the largest US banks as well as other standout organizations in the industry are investing in, and successfully deploying, digital strategies that can attract new customers, improve sales, cut costs and improve consumer experiences. The rest of the industry needs to learn from these organizations … quickly. How do other industry observers view the future?

According to Accenture, “The key for any organizations is to start with the customer. Develop and refine a clear migration strategy. And introduce simple digital solutions that customers want and can control.”

As was said in the J.D. Power research, “Without significant focus on digital investments, regional and midsize banks risk deterioration of financial metrics – higher attrition, less share of wallet, and lower levels of future repurchase.” They continued, “Midsize banks are the most at risk, as regulatory costs have made it difficult for them to invest in strategies to compete with larger institutions.”

Brett King adds, “If you’re a retail bank today, the objectives should be super simple. Deliver extraordinary daily engagement via mobile, leading to stronger relationships and increased revenue. If an organization still requires a signature on a piece of paper to onboard a customer, or if the customer can’t open a new account on a mobile device, then you’re screwed. Mobile isn’t the future – it’s now. ”

Finally, Chris Skinner, chief executive of Finanser Ltd. and author of the book, Digital Bank: Strategies to Launch or Become a Digital Bank, provided this observation in a digital interview, “The large US banks have all moved rapidly to ensure that first internet banking and now mobile is a consumer’s primary access to information. This will mean a shift from physical service to digital relationships. How the big banks make that shift without alienating customers who want physical delivery may be a challenge.”

Skinner continued, “Meantime banks like Bancorp, CBW Bank and Radius Bank are all making headway in finding alternative niches that give them volume and value. The bottom line is that you’re either a megabank with digital reach or a niche bank with focus. If you’re not in either of those two camps, you won’t survive.