According to the 2015 J.D. Power Retail Banking Satisfaction Study, consumer satisfaction has reached the highest levels since the inception of the study ten years ago. However, there are significant storm clouds on the horizon. For instance:

- Differentiating service is more difficult than ever, with midsize institutions losing their long held edge over larger organizations. Interestingly, among Gen Z consumers (born after 1995), satisfaction is highest with big banks.

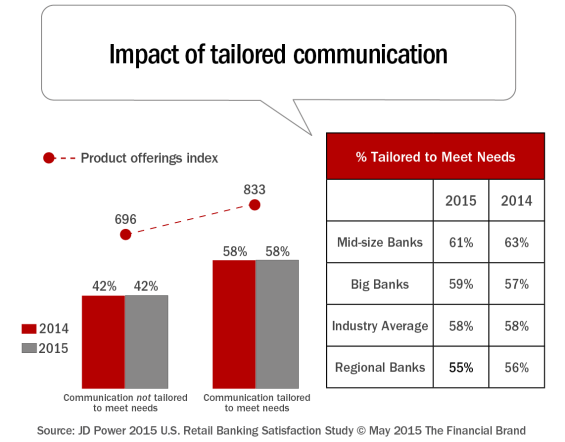

- Consumer satisfaction associated with digital channel functionality has declined from 2014.

- Virtual-only customers have lower rates of loyalty to their primary bank as well as lower retention and advocacy rates.

- More than two-thirds (68%) of virtual-only customers indicate they have not been contacted by their bank in the past year.

- There are fewer customers available for acquisition, with only 6% of customers switching banks in the past year and the majority of Gen Z customers selecting their first bank based on family history rather than by shopping.

These trends illustrate the importance of improving the customer experience from the moment the consumer opens a new account or expands a relationship. Developing a robust new customer onboarding process is the foundation of this strategy.

Expanding on the insights contained in the 59-page ‘Guide to Multichannel Onboarding in Banking’, here are five important ways to improve the results of your current or new onboarding process.

1. Conduct a Thorough Needs Assessment

If the new or existing customer is opening the new account in a branch, this may be the only time your team ever meets the new customer face-to-face. As online and mobile account opening processes have become more customer friendly, there may not be a 1:1 human engagement at all.

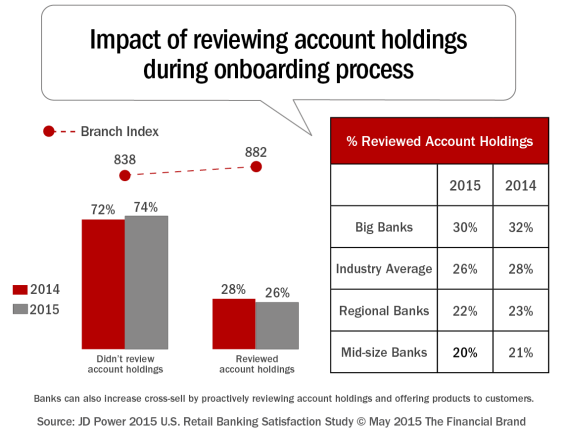

Whether in-person or through digital channels, the new account opening process is the best time to collect insights beyond the basics. For instance, J.D. Power & Associates research has found that reviewing current account holdings and performing a complete needs assessment can have a significant impact on consumer satisfaction as well as cross-sell results.

Unfortunately, despite the benefit of increasing satisfaction, only 26% of banks overall perform this rudimentary process, down from 28% in 2014. The research found that the biggest institutions do this task the most frequently, but still only 30% of the time.

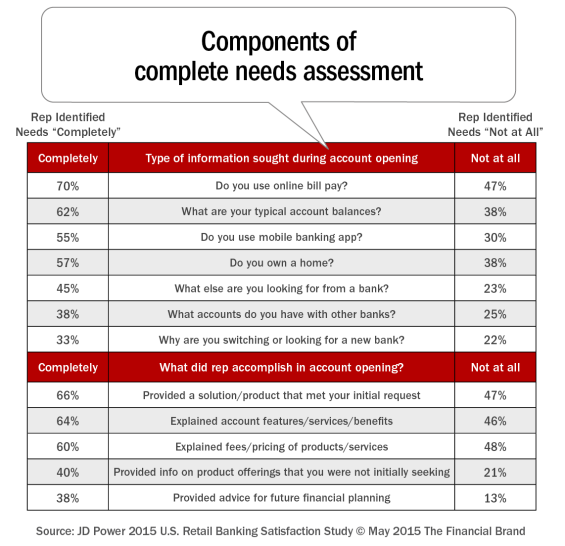

Organizations are much more likely to perform some level of needs identification, with consumers finding that over 50% of organizations did a ‘complete’ needs identification at account opening. This is important, since there is a 126 pt. increase in satisfaction between those organizations that do a partial needs assessment and those that fully assess needs.

![Impact_of_needs_identification[1]](https://thefinancialbrand.com/wp-content/uploads/2015/07/Impact_of_needs_identification1-565x445.png)

Asking relevant needs-based questions as part of the new account opening process improves satisfaction, serves as a differentiator compared to other organizations, and has the potential to build customer intimacy. The challenge is to balance the desire for collecting more insight either in person or through digital channels, with the need to simplify the entire account opening process for an enhanced customer experience.

A simplification strategy that is proving effective for some organizations is the integration of smartphone/tablet camera functionality to simplify the account opening and insight gathering process. By taking a picture of important documents such as a driver’s license, accuracy improves and account opening times are shortened.

In addition, iPads have allowed consumers to complete their own new account form. The rationale is that, while new accounts personnel are notoriously poor at collecting personal insight, most customers psychologically want to make sure all of their questions are answered.

Some of the questions that can be asked as part of a complete needs assessment (and the likelihood of them being asked) according to the J.D. Power & Associates study are shown below.

2. Offer Assistance with Financial Needs

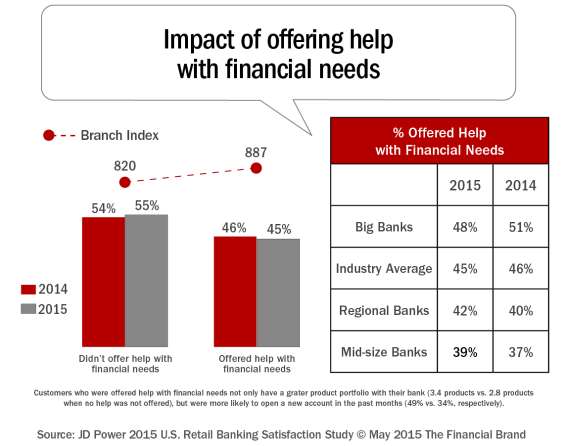

As mentioned, there are many ways to gather the insight needed to determine account holdings and financial needs. The biggest downside to this process is that trust can be broken if the customer believes the insight collected is not used for their benefit.

Alternatively, the upside of providing advice on the insight collected is both a greater level of satisfaction (67 pt. increase on the J.D. Power satisfaction index) and a greater share of wallet (3.4 products vs. 2.8 products). Unfortunately, as is the case with several of the key components of a successful onboarding process, fewer than 50% of organizations offer help with financial needs. Again, the larger institutions were the most likely to offer help, but less in 2015 than in 2014.

3. Follow-Up as Quickly as Possible

According to the Guide to Multichannel Onboarding in Banking report, “One of the key missions with an onboarding process is to get out of the starting blocks as quickly as possible so the customer realizes you appreciate their business.” While a great deal of insight can be collected as part of the new account opening process, it is usually difficult to leverage this insight in the first few days after account opening due to back office processes. The key is to balance what data can be used, with the importance of reaching the new customer as soon as possible.

Some institutions may only have access to the name of the customer or member, address and type of account opened initially. If this is the case, the potential to use a personalized note – handwritten and sent to the customer the same day they opened the account – may be the only option.

If your systems enable you to use insights such as a cell phone number or email address immediately, the impact of sending a simple SMS text or email a few minutes after the new customer leaves the office to thank them for their business is very impactful.

As shown below, the impact on customer satisfaction between reaching the new customer in 3 days vs. 4 days is rather significant. In addition, the benefit of having the initial communication come from the same person who opened the account is also high. With digital technology, this level of ‘personalization’ can be automated.

![Importance_of_speed_of_follow-up_in_onboarding_process[1]](https://thefinancialbrand.com/wp-content/uploads/2015/07/Importance_of_speed_of_follow-up_in_onboarding_process1-565x403.png)

With regard to marketing channel used, the benefit of an email or SMS is both speed and the ability to provide an embedded link to a personalized new customer introduction microsite or even a personalized welcome video (built for mobile consumption). This is where the use of account type data and even opening balance can be effective.

The objective of this immediate communication is to thank the customer as quickly and as personally as possible using the customer’s name, the type of account opened and what the customer may expect next. Imagine this as the combination of account opening ‘receipt’ combined with personalized ‘thank you.’

4. Follow-Up with New Customer Frequently

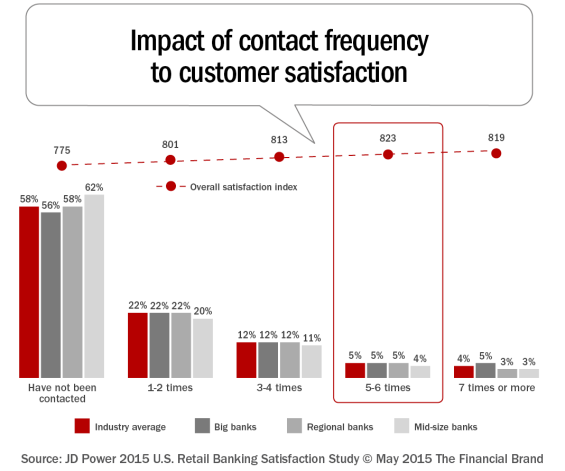

An ongoing misconception by financial institutions is that customers don’t want to get a lot of messages after opening a new account. As has been shown by J.D. Power & Associates research in the past, customer satisfaction and cross-sell success both improve as the number of contacts are increased up to 5-6 times, and is still effective if the customer is communicated with as many as seven or more times.

Despite the impact of multiple communications, the majority of consumers still do not recall being contacted by their financial institution, with only one in five indicating their bank or credit union connected 1-2 times. This represents lost potential good will, sales and revenue.

What most banks and credit unions also forget is that not every communication sent to the new customer is read or even delivered, even when the organization has done their best to make the communication both personalized and relevant. Therefore, the optimal number of messages scheduled could be even higher than the J.D. Power study suggests.

5. Personalize the Communication

Of all of the ways to improve the overall onboarding process, the most important driver of enhanced customer satisfaction is applying customer-level insight to customer communications. Beyond simple name and account type data, the communication should reflect the actions each customer taken and the insight that has been shared during the onboarding period.

The goal is to mine the customer insight to generate automated needs-based messages that are consumer (as opposed to profile) specific. This allows real-time adjustment to a customer’s profile based on purchase behavior, remembering the importance of ‘engagement before selling.’

Just as important as remembering the demographics and product ownership of the customer, it is important to build a communication channel strategy for each customer based on the channels they use and respond to the best. By leveraging data from all sources, content can be developed based on needs, channels and devices.

As opposed to moving immediately to cross-selling new services, the majority of early communication should focus on logical ‘go with’ services, such as direct deposit, bill pay, alert notifications, online and mobile banking, mobile deposit capture, loyalty/rewards program and actual usage of the account. Once trust is established with highly personalized communication, the relationship can be expanded using additional insight captured.

The onboarding process should begin with traditional communication channels, such as direct mail, email, statement inserts, etc. and quickly leverage other channels such as SMS messaging/alerts, ATM messaging, social media, call center, etc.

Bottom Line Impact of Successful Onboarding

As stated in the ‘Guide to Multichannel Onboarding in Banking,’ the negative impact of an attired customer is $400 based on the sunk cost of acquisition and the revenue potential of a new customer. With attrition rates of new customers still hovering between 25% and 40% at most institutions, the financial cost of lost customers is staggering.

As we look at the recent findings from J.D. Power and Associates, we get an even clearer picture of the value of satisfaction improvement that can be achieved early in the customer’s relationship. According to J.D. Power, improving customer satisfaction by as little as 50 points can equate to a $24 million increase in revenue per 500,000 customers. Put differently, a 50 point increase in satisfaction per customer can equate to a 6% increase in revenue.

An improved customer experience and customer satisfaction is core component of bottom-line growth. However, continually changing customer preferences, needs, and expectations create a challenge for banks in determining how to increase customer satisfaction. Onboarding is not only the best way to establish a great first impression, but one of the most economical (and impactful) ways to impact satisfaction.

It is still amazing that so many institutions have yet to develop a way to say ‘thank you’ to their new customers.

About the J.D. Power Retail Banking Satisfaction Study

The 2015 J.D. Power Retail Banking Satisfaction Study is the longest-running and most in-depth survey of the retail banking industry, with more than 80,000 consumers evaluating various aspects of their banking experience. The study measures satisfaction in six factors (listed in alphabetical order): account information; channel activities; facility; fees; problem resolution; and product offerings.

Channel activities include six subfactors (listed in alphabetical order): ATM; branch; call center; IVR; mobile; and website. Banks are ranked based on overall customer satisfaction in each of the following regions: California, Florida, Mid-Atlantic, Midwest, New England, North Central, Northwest, South Central, Southeast, Southwest and Texas. Satisfaction is measured on a 1,000-point scale.