The inaugural FIS Consumer Banking PACE Index™ was created to provide an index based on 18 banking service attributes thought to be essential to developing relevance and trust with banking consumers. The index was designed to help financial institutions better understand both their customers’ key expectations and the delivery performance against these expectations.

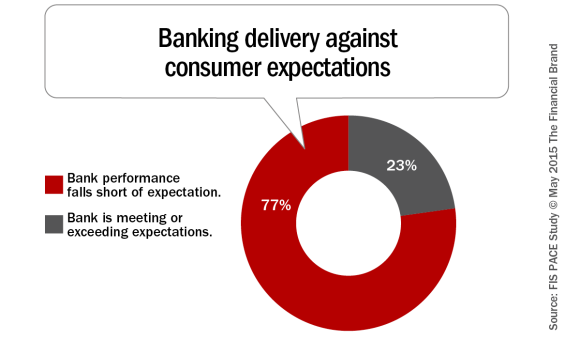

The index was built based on surveys conducted in nine countries with individuals who have a checking/current account or its equivalent with a financial institution. Results of the study show that, worldwide, while consumers say financial institutions excel at providing digital access and convenience, 77 percent of consumers do not believe banking meets expectations in basic banking areas such as fair and transparent pricing.

This suggests that while the financial industry as a whole is successfully delivering digital access solutions, there are significant opportunities to build a stronger foundation for consumer relationships. This can be achieved by more fully leveraging online, mobile and social platforms to integrate with consumers’ lives through insight-driven alerts, advisory services, planning tools and more.

“New providers and non-traditional financial institutions continue to make inroads, particularly amongst younger generations, who studies show will soon make up the majority of bank revenues,” said Anthony Jabbour, CEVP, Integrated Financial Solutions, FIS. “With these challengers poised to grab customers, financial institutions have the opportunity to lead with their strengths and re-define advisory services. Consumers value the banking relationship and banks have a significant opportunity to be viewed as more than a vehicle for transactional convenience, but rather a true focal point of consumers’ financial lives.”

Where Banking Is Falling Short of Expectations

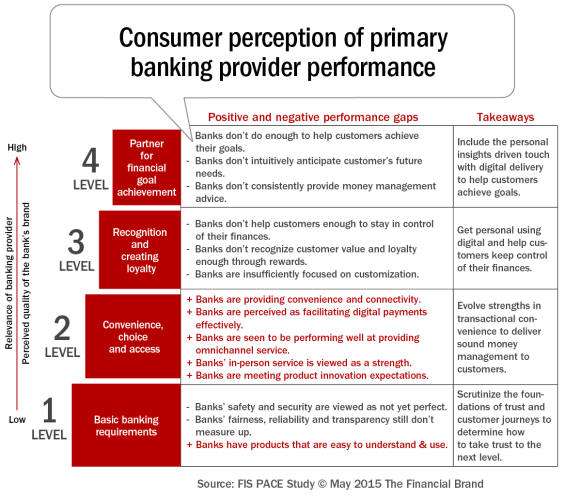

The attributes in the FIS PACE Index are clustered in four ascending bands of banking service relevance and quality. Level 1 attributes are recognized as essential, foundational requirements in today’s consumer banking environment (e.g., safety, security, fairness, reliability, transparency). Level 2 attributes are critical for successfully matching the current and future styles of banking competition required to attain and deepen customer relationships (e.g., being connected, omnichannel access, digital payments).

The index was generated in the following manner:

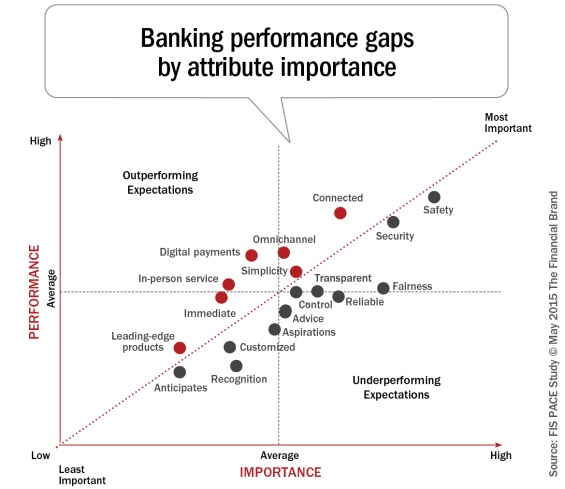

- The performance score for each attribute statement is subtracted from its importance score to yield a positive or negative figure (performance gap). For example, the global importance score for Safety was 85 and the global performance score was 81, resulting in a performance gap of -4.

- The index is compiled by weighting gaps between importance and performance for all attribute statements according to their importance, compiling the weighted gap scores across all statements and then centering those aggregated scores around 100 in order to create an index.

- An index of 100 indicates that performance matches importance overall.

- Indices below 100 indicate shortfalls on at least one dimension.

Given the number of recent high-profile security breaches, it’s not surprising that safety and security top the list of what’s important to banked consumers. Unlike many other attributes, which vary in importance according to population segment, safety and security are universal concerns. Delivering on those attributes therefore represents the price of basic entry for being in the banking business.

Also ranked as important were the attributes of fairness, reliability and transparency – that affect the very foundations of building a trusted relationship between customers and their banking service providers. Unfortunately, beyond providing reasonably easy to understand products and services, banking organizations fall short on the majority of these most basic (and important) requirements.

Banking also fell well short of expectation on both the Level 3 and Level 4 attributes. Among the research findings:

Financial organizations don’t help customers stay in control of their finances. Customers place above average importance on personal financial control as a factor that empowers them. Globally, banks fall short of enabling control.

Financial organizations don’t recognize customer value through rewards. There is a wide gap between consumer expectations and bank performance in the area of recognition for bringing personal business to the bank.

Banks are insufficiently focused on customization. Although most consumers indicate low demand for customized banking products, banks are still seen to be falling short in the area of tailoring products to individual profiles and needs.

Banks don’t do enough to help customers achieve their financial goals. Consumers have modest expectations for obtaining financial advice to help them manage their money or achieve the goals that are important to their lives. Unfortunately, banks are falling short of meeting even these modest expectations.

Banks don’t intuitively anticipate consumer customers’ future needs. Currently, consumers have low expectations that banks will actively support anticipating their future needs. Even with the bar set low, banks are not delivering in this area either.

It’s Not All Bad News

As mentioned, the banking industry appears to be meeting expectations around access and convenience. But, that is not to say that the industry shouldn’t evolve relationships beyond providing transactional convenience. They can and should extend to facilitating sound money management and financial goal attainment.

The research found that the industry does relatively well with Level 2 attributes:

Banks are providing convenience. In fact, they are exceeding consumer expectations for delivering a convenient

banking experience.

Banks are providing connectivity. Overall, consumers rate banks as performing above expectations for enabling their

connectivity, including anywhere, anytime access through online and mobile banking.

Banks are perceived as facilitating digital payments effectively. Overall, consumers rate banks as performing

significantly above expectations in digital payment options for financial transactions. This area is in fact the biggest positive performance differential among all attributes surveyed. (This positive gap may change, however, as expectations increase with the expansion of mobile payment capabilities).

Banks are seen to be performing well at providing omnichannel service. Most consumers believe that banks provide consistent account information across all the possible points of contact with the banking provider.

Banks are meeting product innovation expectations. A small portion of consumers place high levels of importance on offering more leading-edge products than other financial institutions as a differentiating factor between banks. While most consumers simply require market-parity product performance, consumers positively ranked banks’ performance around product innovation.

Risks and Opportunities

According to FIS, there is great opportunity for banks to enhance the new consumer buyer. Nearly two-thirds of the 18 attributes measured in the study showed negative trends in perceived banking industry performance. According to the findings,

only a quarter of today’s banked customers are likely to grant their banks permission to pursue high-value relationship based

customer journeys.

Of particular concern is that satisfaction levels rise with age, implying growing shortfalls in satisfaction in the future,

as younger customers become increasingly important and more influential. Younger, higher-earning, tech-savvy consumers who have greater potential to engage in high-value bank relationships have expressed concern with banks and are consequently more likely to consider offers from alternative financial services providers. This is consistent with other studies that have found an increasingly dissatisfied segment among digital banking consumers.

By analyzing the factors leading to the shortfalls in customer satisfaction, these are the specific areas where the banking industry has the opportunity to improve in order to retain customers (especially the most attractive profiles) and grow value include:

Fix the foundations of trust. Customer requirements around fairness, reliability and transparency will not subside. To truly satisfy customers, banking providers need to look beyond today’s orthodoxies, examining new customer-centric means of overcoming these challenges. A greater focus on simplifying customer communications is required. But a lasting solution calls for studying the key aspects of trust building through the customer journey – e.g., account opening, applying for different types of loans and credit – to identify where trust breaks down.

Move beyond the transaction. It is important to evolve relationships beyond providing transactional convenience, extending to facilitating sound money management and financial goal attainment.

Make digital contextual. Establish a rich advisory relationship with the growing numbers of customers who prefer to engage digitally. Use online, mobile and social platforms to deliver better information, alerts, advisory services and planning tools that are deeply integrated into customers’ lives.

Streamline operations. Banks must streamline and optimize the front and back offices to deliver low- and no-touch commoditized processes to provide the highest quality, with the highest security, and at the lowest achievable cost.

Research Methodology

The FIS Consumer Banking PACE Index™ tracked how financial institutions performed against customer expectations in nine different countries: the United States, United Kingdom, Brazil, Canada, France, Germany, India, Netherlands and Thailand, using data compiled from more than 9,000 banking consumers. Commissioned by FIS, the study was conducted by TNS.