Every once in a while, a consumer study is released whose findings are…well, let’s just say “hard to believe.” One of those studies crossed my desk this week.

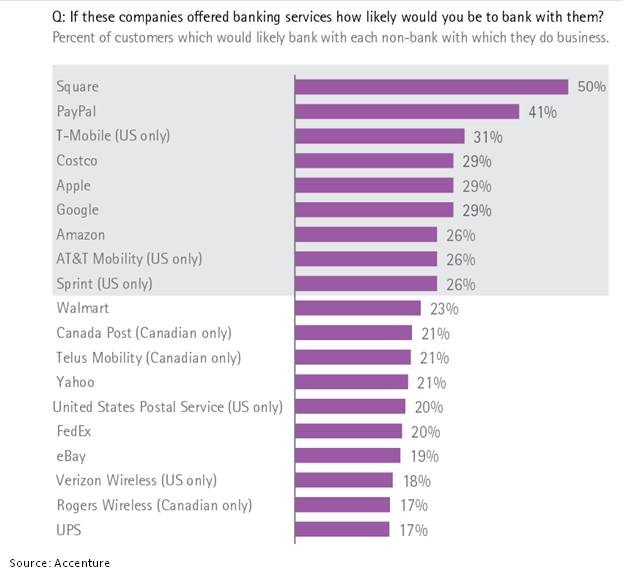

A survey of 3,800 Americans and Canadians revealed that 50% of respondents said that they would be likely to bank with Square if the company offered banking services.

My take: No way (or there are a helluva lot of Canadians willing to bank with non-banks).

My take: No way (or there are a helluva lot of Canadians willing to bank with non-banks).

***

In a comScore study done about two years ago (November 2012), just 8% of consumers studied said they had heard of Square Wallet (which, granted is not the same as knowing about the company), and just 2% had used it.

In a Q2 2013 study conducted by Aite Group, consumers were asked how well they thought various companies would do at providing mobile shopping features and capabilities (including data privacy, data security, relevance of offers, quality of payment advice, and overall experience). Regarding Square, roughly eight of ten respondents said they didn’t know how Square would do on each of these features. Of those that did have an opinion, about a quarter thought Square would not do a good job at providing these capabilities.

So, as of two years ago, few consumers had heard of Square, and, more recently, the vast majority of consumers had no idea how well Square would do at providing mobile shopping services. But 50% of consumers would be likely to bank with Square if it offered banking services? Yeah, right.

***

The 41% number associated with PayPal seems suspect, as well.

A Bloomberg article titled The Kids Aren’t Into PayPal as Apple Rules Mobile reported:

“If you’re below 30, PayPal’s not relevant,” Gene Munster, an analyst at Piper Jaffray Cos., said in an interview. While PayPal may be a go-to for secure eCommerce transactions online, Davis Meiering, an undergraduate student at NYU, said it’s not what he turns to on his phone, whether it’s for payments between friends or in stores. “I don’t use the PayPal app on my phone,” Meiering, 20, said. Arielle Gurin, a 22-year-old student at the University of Maryland, says PayPal is “outdated already.” “I know you have to have it for like EBay, or you can use it for Amazon,” she said. “But I feel like it’s not big anymore.”

But 41% of North Americans would be “likely” to bank with PayPal if it offered banking services? Yeah, right.

***

It seems like everywhere I turn, pundits are warning banks that non-banks–in particular, “technology” companies like Apple, Google, and Amazon–are going to get into banking and steal business away. Rarely do we hear, however, about the threat from firms like Costco, who garnered as many mentions as Apple and Google, and slightly more than Amazon (who I’ve always considered to be the bigger threat).

***

Perhaps most amazing to me is that nearly one in five Americans said that they would be likely to bank with Verizon Wireless (at least, according to the Accenture study). The only thing I can conclude from that is that one in five Americans suffer from severe brain damage. VZW is the most incompetent company on this planet.

***

The study would seem to be good news for the US Postal Service, who was mentioned by one in five Americans as a provider they’d be likely to bank if it offered banking services (which has been proposed). The USPS can’t run its core business profitably, so getting into banking would be a brilliant move (I’m hoping you smell the sarcasm emanating from the screen).

***

For as long as I’ve been doing consumer research in financial services, consumers (younger ones, in particular) have always said that they would consider, or even be likely to use, non-bank providers for their banking needs. Fifteen years ago, it was Microsoft and Sony at the top of the list, today it’s Square and PayPal. Nearly any company that is highly-regarded by its customers will be seen by those customers as possible candidates to provide products and services that aren’t part of the company’s core set of services.

So why don’t these surveys ask “how likely are you to buy a car from Costco if they made or sold cars?” or “how likely are you to get a smartphone from PayPal if it made one?” The inference, when asking “how likely are you to bank with ___ if they offered banking services?”, is that it’s somehow easy for all these non-bank companies to get into banking, or likely that they’ll do so.

But if so many people are seemingly willing to bank with non-banks, why don’t Simple and GoBank have millions of customers already? And if so few Amazon customers are getting a smartphone from Amazon, why would a quarter of all Americans be so willing to bank with the company?

Bottom line: People will tell market researchers anything. When you put a laundry list of companies in front of people, and ask hypothetical questions with no boundaries or constraints, the results won’t be very reliable.

What if the researchers asked: If CostCo were to offer banking services, at the same or higher cost as what existing banks charge today, how likely would you be to bank with CostCo? Do you think nearly three in 10 North Americans would have said “likely” or “very likely”? Maybe they would have, I don’t know.

I imagine that the purpose of these studies is to strike fear into the heart of bankers that someone not on their radar is going to steal their business, and….and do what? Employ the consultants and tech vendors who do these studies to develop strategies and deploy new technologies?

If that strategy works, then I hope blog posts like this don’t stop anyone from publishing studies about the non-bank threat. But I do hope posts like this get you to think a little more critically about the results getting published.