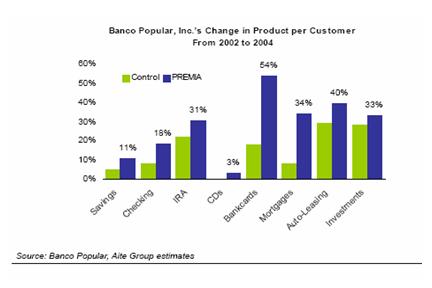

The Aite Group recently published an excellent report on reward/loyalty programs in financial services. I can’t share their analysis and forecasts here, but they did give me permission to share the following chart, which shows the impact that Banco Popular’s loyalty program, Premia, had on the depth of their customer relationships.

[Note: The point of comparison with the plan’s 250k members wasn’t just all other customers, but a control group with demographics similar to the plan participants. In addition to the product growth, attrition among Premia members was 4% versus 11% for the control group and 13% for all customers]

A couple of thoughts on this:

- In addition to the loyalty program, which rewarded members for their relationship across a range of products (not just credit or debit card), Banco Popular must be doing something else right — those are impressive cross-sell statistics even for the control group

- My bet is that plan members (and thus, the control group) skew towards younger adults, who are more likely to: 1) be in the market for credit cards and auto loans, and 2) consider doing business with one firm (us Crankys don’t like to put our eggs in one basket)

- There’s another benefit here: The impact on employees. Richard Davis, of US Bank, said in Banking Strategies: “…[our] program has grown into a full suite of rewards including cash, miles, or merchandise. For the first time, the employees, en masse, said, “I like this program. I’m finally giving something to my customers that they may want.”

Results like these, coupled with the loyalty program efforts of high-profile firms like Citigroup and Bank of America, point to increased deployment of cross-product loyalty programs within financial services. Smart firms, though, won’t just rely on a loyalty program to build long-lasting relationships. They’ll use loyalty programs to:

- Increase engagement. A loyalty program can be effective at creating economic loyalty. But to create emotional loyalty, customers need to be engaged with the bank in meaningful interactions. A loyalty program can be instrumental in creating these opportunities beyone simply balance checking and problem resolution.

- Glean customer insights. Doing market research is expensive and potentially time-consuming. Highly engaged loyalty program members will prove to be a timely (and cheap) source of customer behavioral data as well as attitudinal data.

- Compete. Large banks will face some internal organizational structure hurdles when trying to create cross-product reward programs. I expect to see a number of large and mid-sized credit unions to capitalize on this and aggressively pursue loyalty programs to compete with these firms in their marketplaces.