Millennials are the most ethnically and culturally diverse generation in US history, with varying financial needs and a multichannel method of researching and accessing financial services. As a result of their age, they are experiencing many life changes as they move from education, to employment, to marriage, to starting a family.

As these changes occur, Millennials are regularly changing their financial goals, attitudes and requirements from their financial institution. Each of these life events provide opportunities for banks and credit unions to engage the Gen Y segment with the hope of beginning the process of cultivating a long-lasting relationship.

For example, according to a study by Experian, seven percent of Millennials expect to buy their first home in the next year, with 16% expecting to get a better job – both of which are double the rate of total adults. These expected life events provide marketers unique opportunities to begin or grow relationships with this young generation before they have established relationships elsewhere.

![life_events_millennials[2]](https://thefinancialbrand.com/wp-content/uploads/2014/10/life_events_millennials2-565x471.png)

Representing 30% of the population and covering a 16-year age range, Millennials are an extremely broad swath of consumers. With such size and diversity, financial marketers need to avoid assuming these young consumers are a single, homogenous, relatively low value group. Instead, smart marketers should target this segment on the key qualities that set certain sub-segments apart.

Read More: Smartphones Changing The Way Millennials Bank

The Power of the Millennial Graduate

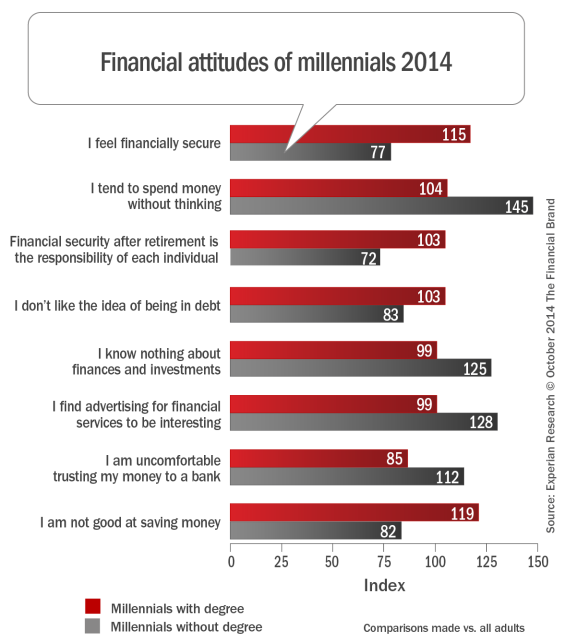

While the Millennial base as a whole has lower income and more modest financial needs, college-graduated Millennials yield a much different profile than their non-graduated counterparts. According to Experian, this sub-segment is more likely to be focused on growing their families, investing in their current homes and moving up the career ladder – all significant lifestage triggers for financial institutions trying to meet customer acquisition goals. They also have nearly double the income of the non-graduated segment at $52,700.

College-educated Millennials are success-oriented, yet more driven by career and financial security than their non-graduated peers. These educated consumers tend to have financial attitudes similar to the general population in terms of their their financial planning, attitude toward debt and their interest in financial marketing.

When it comes to financial services, graduate Millennials should be a core target for acquisition, not only because their future earnings justify the cost of winning their business but because the majority also have a savings account (59%) and almost half (40%) already have investments. They are also more likely than then average adult to have a 401K.

![Investments_owned_millennials[1]](https://thefinancialbrand.com/wp-content/uploads/2014/10/Investments_owned_millennials1-565x602.png)

According to the Experian research, while both non-graduate and graduate Millennials are more likely to have educational debt, the post graduate segment is 3.4X more likely to carry this form of debt. Because of the income that accompanies full-time employment, however, they are also more likely to have a mortgage loan (32%) and car loan (35%) than both their non-graduate peers and the adult public as a whole. Illustrating the financial maturity of the graduate Millennial, they are also 35% less likely to carry credit card debt.

![Loan_use_millennials[1]](https://thefinancialbrand.com/wp-content/uploads/2014/10/Loan_use_millennials1-565x507.png)

Read More: 9 Insights For Lasting Banking Relationships with Millennials

Taking Advantage of the Millennial Opportunity

As expected, the best way to reach Millennials is through digital channels. Thirty-five hours of a Millennial’s average week is devoted to digital channels, equaling more than 50% of overall media usage based on the Experian research. More specifically, the mobile channel is the center of the Millennial world, with this segment open to brand and marketing efforts on their phone.

For financial marketers, this does not mean other channels should be ignored (since a multichannel will almost always outperform a solo channel effort), but a mobile-first strategy will be needed to reach this segment.

When you acquire the Millennial consumer, these households will also access their account on their mobile device. In fact, Experian found that 40% of all consumers who use finance apps or visit mobile finance websites in a typical month are Millennials, which is disproportionate to the their 30% of the overall adult population. In other words, a branch strategy is not important to the younger consumer.

Read More: Millennials Find Banks Irrelevant