It is an accepted fact that the incremental cost of selling to current customers is generally much lower than to prospects. For this reason, many financial institutions have invested heavily in finding better ways to reach current households to increase wallet share.

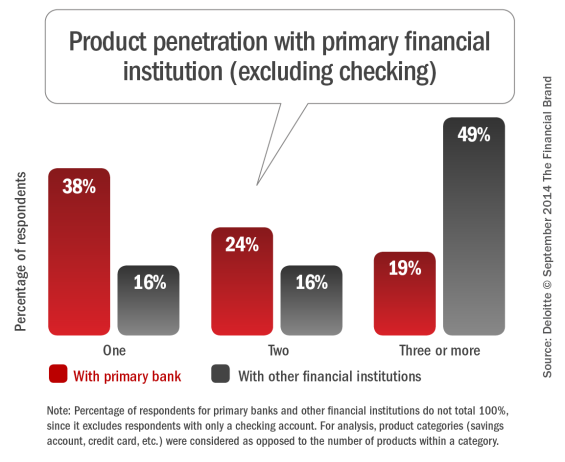

Unfortunately, most organizations are not realizing the full potential of cross-selling, either because of poor program development or simply missed opportunities. A Deloitte report entitled, ‘Kicking It Up a Notch: Taking Retail Bank Cross-Selling to the Next Level,’ supports the view that existing cross-selling programs may be ineffective: only 19 percent of retail bank customers owned three or more products in addition to a checking account with their primary bank, compared to 49 percent who have three or more products with other financial institutions.

So, the following questions remain: 1) Why have customers opted not to expand their product relationships with their primary financial institution despite years of extensive efforts? 2) Is there a need to re-assess and refine how organizations approach cross-selling efforts? 3) Are there segments institutions can target to capture higher wallet share?

Mobile Selling: The Missed Opportunity

One of the continued areas of missed opportunity for cross-selling current households as well as households searching for a new financial institution partner is through the mobile platform. With mobile devices becoming increasingly popular for browsing and purchasing products, banks and credit unions need to determine how to sell intelligently via the mobile channel.

According to the Mapa Research report, ‘Selling on Mobile: Using Browsers and Apps to Improve Acquisition and Retention,’ organizations are slowly beginning to connect with the mobile customer to sell products and services. Analyzing 35 institutions across 10 countries, Mapa found three alternative ways banks and credit unions reach mobile prospects and customers:

- Mobile optimized, adaptive or responsive sites to welcome mobile shoppers

- Selling within the mobile banking app: Pre login

- Selling within the mobile banking app: Post login

The key findings in the 68-page Mapa report included:

Banks are wary of not being too intrusive –Selling needs to be executed carefully on mobile devices, in particular due to the smaller screen size compared to desktop. It is clear that organizations do not want to interfere too much with customers carrying out their intended task or interrupt other processes. In the majority of institutions examined, the majority have taken a service-led approach.

Traditional approaches to selling prevail – Many of the approaches are similar to the somewhat passive sales approach used for online banking, using product sections, carousel banners and ‘Open an account’ messaging on the overview page. More progressive institutions are starting to use enhanced data to provide personalized (and in some cases pre-approved) offers and sales messages intelligently positioned within the app.

Contextual selling and marketing is an opportunity to intelligently become part of a consumer’s daily life. There is also the opportunity to connect with consumers on a social level using services such as Facebook, Skype, What’sApp and iBeacons.

Savings and ancillary services are the primary focus – Globally, savings account products and ancillary ‘go with’ services are the most frequently promoted and sold via mobile devices. In some cases, it is a matter of a one click application or it may even be included as part of setting up a savings goal within the app.

More complex products such as overdraft protection, investment products, personal loans and even mortgages are beginning to be sold via mobile. As more extensive data is being leveraged for mobile communication, the ability to effectively connect product sales with consumer needs will be improved.

Mobile Browser Sales Experience

Financial institutions have taken different approaches to the initial contact with mobile shoppers. According to Mapa, the vast majority of organizations researched provide either a responsive or mobile optimized website experience. Roughly a third have taken a servicing approach (with a focus on being a gateway to mobile banking login), while a third have a sales driven approach (with the focus on products offered and, on occasion, applications). The final third have taken a mixed approach with sales and servicing.

On the landing page, organizations are following the path usually used in online banking, with static or carousel banners to promote a product or service. These services usually include personal loans, credit cards and checking accounts or with the general message of ‘become a customer.’ Surprisingly, mobile application processes are scarce among the institutions reviewed. Banks in Australia (Commonwealth Bank, ANZ and Westpac) seemed to be the exception with each providing mobile applications for checking (current) accounts.

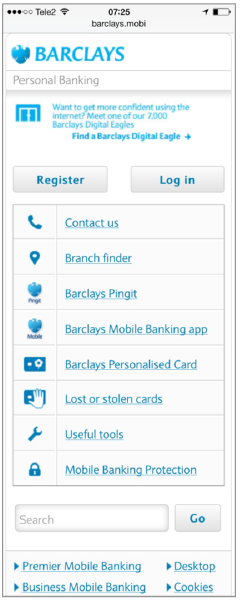

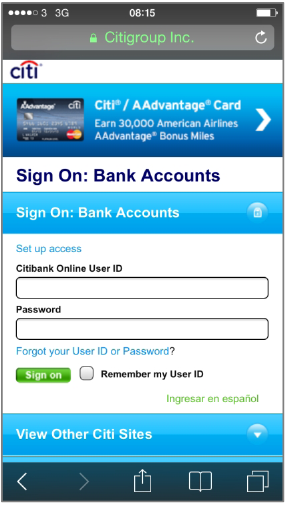

The examples below show how some organizations provide only a gateway to mobile banking login through their browser application. Rather than providing any sales message – which could interfere with logging in – these organizations stick to the basics. There is definitely a lost opportunity in these cases.

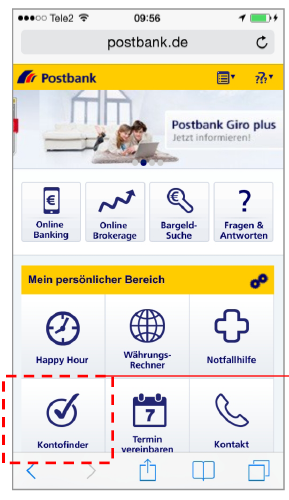

The use of interactive content to assist in finding the right product is rare. Postbank is an exception, providing a link to an account finder tool on the landing page with the use of questions to determine the best account package.

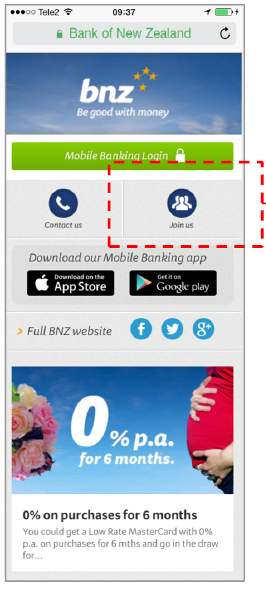

Bank of New Zealand provides a prominent ’Join us’ icon on the mobile site landing page which directs visitors to download the mobile app. While no specific product is promoted at this stage, this may be geared to shoppers who already are fully engaged in the shopping process. A ‘click to call’ link is provided on the ’Join us’ page to provide support. In addition, visitors are directed to the full BNZ website if they want to learn more about joining.

Pre Login Mobile App Sales Experience

Somewhat surprisingly, the majority of the banks researched by Mapa did not provide any sales messages at all prior to login. Of the approximately one-third that did have a sales message, all used either static or carousel banners to promote their products and services. Most directed customers to browser pages integrated within the app.

Some banks had a dedicated section featuring a list of products or offers which lead to individual product description pages. As with the mobile browsing examples, mobile product application capabilities are scarce, with ‘brochureware on mobile’ being the overriding strategy. Some organizations are beginning to encourage savings on the pre-login page.

SEB Bank in Sweden provides the opportunity to apply for a credit card (and other products) directly on the landing page before login. The link takes visitors to the mobile web page where the application can be done over two pages. (first step illustrated below where personal details needs to be entered). This approach would be highly effective when combined with a digital retargeting program based on the visitor’s previous browsing history.

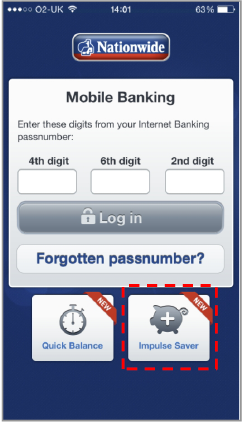

Nationwide in the U.K. recently launched an Impulse Saver feature to their mobile banking app that allows the customer to transfer a set amount from their checking account to their savings account, without having to login. Customers opt-in to the feature within the secure site, selecting the accounts to be used and the amount to be transferred.

A pre login feature such as this can help to increase savings deposits by giving users an opportunity to save as much as they want and as often as they want to without a regular commitment according to Mapa.

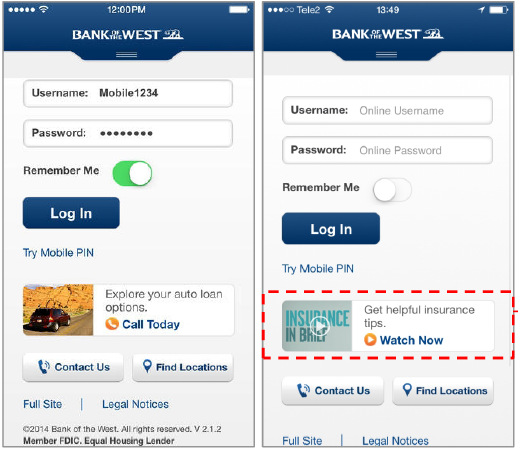

Bank of the West has introduced a dynamic messaging program to deliver tailored offers and content pre-login. They have used both links to get helpful product tips via video as well as tap-to-call options. With video content becoming a more form of content on mobile devices, short-form video can be a great sales opportunity.

Post Login Mobile App Sales Experience

Despite researching dozens of leading financial institutions globally, Mapa found that the majority of the banks still do not provide sales messages within their mobile app. Similar to pre login examples, banners are the typical choice for communicating sales messages.

Of those that do try to provide sales messages, some are as general as an ‘Open a New Account’ tile. Unfortunately, very few provide a link to a mobile application page within the app login area. According to the research, savings account are clearly the most frequently promoted product, while also being the most popular product among banks to develop an application journey for.

Instant account opening is available with some providers, but is far from being the standard. Other product applications occurring with a small number of providers include checking (current) accounts and credit cards. In the last 12 months a small number of banks have also introduced mobile applications for non-conventional products such as overdraft protection, investments and even personal loans and mortgages.

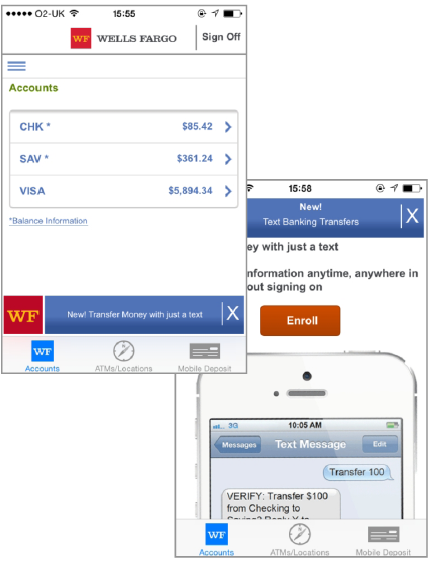

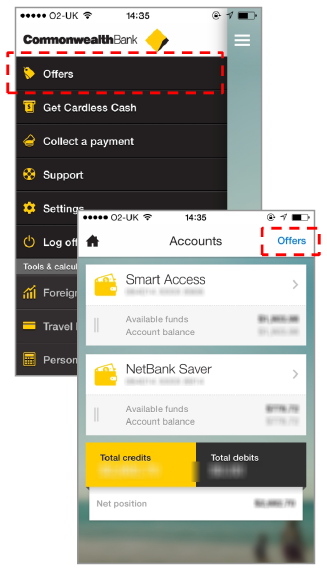

The key to promoting products and services within the secure banking space is to not distract the customer from the initial intended banking task. Many banks have done this by utilizing space within the account summary screen. For instance, Wells Fargo uses a promotional sticky banner on its account summary screen to promote a service that can be easily turned off by a click thereby making it less annoying to less interested customers. Commonwealth Bank (AUS) uses a subtle sales technique with a link ‘Offers’ at the top right of their account summary screen and within their nested navigation.

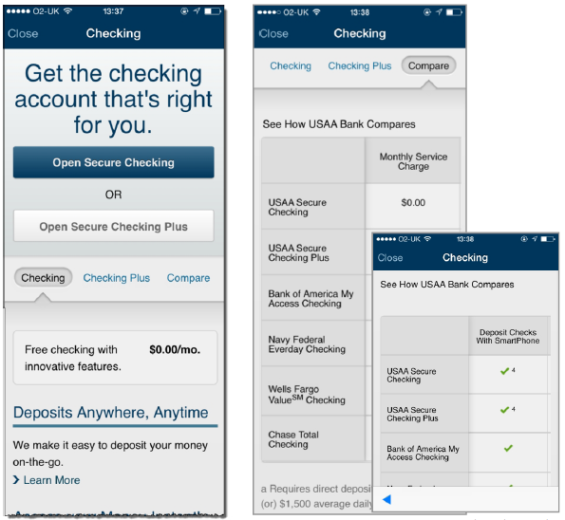

Being one of the early pioneers of selling via the mobile device, USAA leverages a very clean product description pages with product benefits clearly listed and segmented by product type. The page also has a product comparison tab letting customers get a quick comparative overview of benefits and costs assisting them to make a more informed decision.

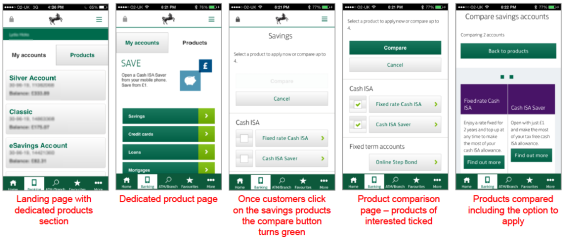

One of the best examples found of selling via the mobile app was with the Lloyd’s Bank products section promoting savings plans. What stood out with this app is an optimised account comparison tool. Customers can compare up to four savings accounts with easy to use links. Customers can easily complete the sales journey by applying directly for selected accounts.

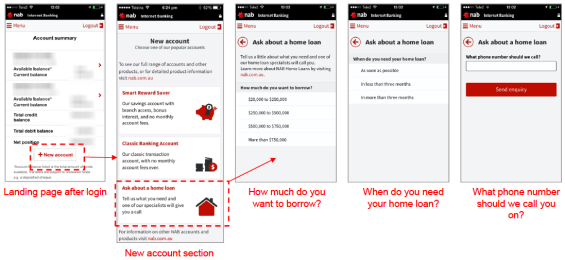

NAB in Australia uses a ‘Add New Account’ section on their login page. As part of the ‘New account’ section, customers can request a call back in order to speak to a specialist about home loans. As part of the process, customers are asked how much they want to borrow and when they need the loan. While not quite a click-to-call functionality, this mobile process may be effective for picking up leads and then diverting them to an appropriate channel for extended dialogue.

Blueprint for Mobile Sales Success

Not all financial institutions are at the same place in their mobile development journey. While some organizations are just trying to provide the basics for their customers and members, others are well down the path or providing advanced mobile features that can combine the best of product offers with contextual delivery.

Using the mobile device and mobile banking platform for sales does not need to be difficult. With more and more consumers using mobile devices for their everyday banking, this channel must be leveraged to maximize the value of relationships. Ignoring this channel leads to lost sales and a less impactful consumer experience.

According the the excellent Mapa research that provides more than 30 examples of how financial institutions sell on mobile, the following are the keys to mobile banking sales success:

- Personalize offerings and leverage contextual engagement: A growing number of banks are introducing access to discounts and cash back programs directly tied to retailers. Bank of America and Lloyds Bank (UK) both provide offers via mobile devices based on their network of retailers and purchase activity. Some banks even provide offers selected and presented based on customers’ current location.

- Leverage social media as part of a digital sales strategy: Social integration for sales via the mobile device are definitely rare. USAA is probably the best example, providing customer ratings as part of landing pages. Discover enables customers to refer friends through the mobile banking app and gain a cash back bonus as a result. Simple and PNC Virtual Wallet even allow customers to provide video reviews.

- Selling from the consumer perspective: Commonwealth Bank in Australia provides a ’Can’-section, taking a consumer’s perspective highlighting a number of typical scenarios like ‘Buying a Car,’ ‘Buying a Home,’ Saving,’ and ‘Moving.’ As navigation is not always intuitive, USAA provides the option of voice commands as part of their app.

- Exploit cross channel integration: Consumers usually don’t start and end a buying process on a single delivery platform. To meet consumer needs, it is important that an application or buying process begun on a mobile device can continue on a tablet, desktop computer or branch without needing to restart the process.

- Embrace sales innovation: There are new opportunities to communicate with consumers being introduced daily. From new mobile platforms like Google Glass, smart watches and iBeacons, each provides a new way to reach and provide solutions to consumers. Westpac in New Zealand continues to be one of the innovators in sales, testing different channel for reaching the consumer.

The Mapa ‘Selling on Mobile’ Report

Mapa Research has followed the changes in how financial institutions sell via the mobile device for the last few years. Besides providing a 68 page view and analysis of the overall marketplace, Mapa also reviewed the growth in mobile selling in April of 2013.

Their findings include in-depth insight as well as examples from the secure area of a number of innovative banks across the globe.

The analysis starts by looking at the mobile browser experience and in particular how banks are using this for ‘welcoming’ potential customers. The focus is on becoming a customer by opening up a current account. Mapa also examines if and how banks utilize the sales opportunity as part of apps – split into pre and post login. Finally, they provide a look ahead and highlight a selection of potential sales (mobile in particular) related opportunities for banks.

A 14-page summary of the more expansive report is available.