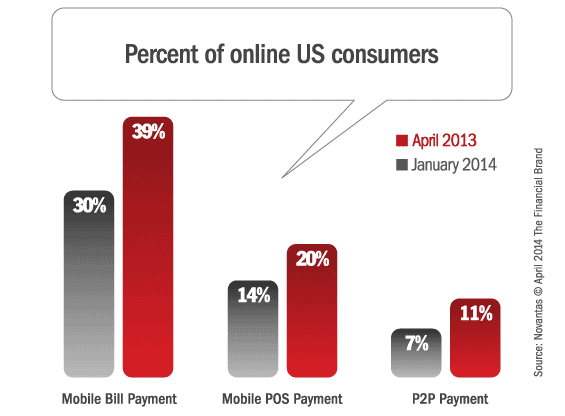

A recent survey on FindABetterBank indicates that more and more consumers are beginning to use their smartphones to make payments. Banks and credit should act now to avoid being left out or marginalized. Why? Aside from eroding interchange revenue, mobile payments will be disruptive because it disaggregates a major component of how consumers use their primary bank accounts.

The risk for banks and credit unions is that consumers will adopt and use third parties to make mobile payments. Already, many consumers that make mobile bill payments prefer to use billers’ mobile services over their bank or credit union. Over 2 million retail locations in the US can already accept PayPal mobile payments. How many of your customers already have accounts set-up with PayPal? Banks and credit unions need to adopt a strategy that will keep the primary bank account as the hub for payments.

Here are four ideas that will put your institutions in the middle of customers’ mobile payment transactions:

1. Offer expedited bill payments. Consumers prefer to use billers’ mobile services for payments because they want their payments to be credited right away. Expedited mobile bill pay is the best way to ensure customers will use their primary bank account. Remember, billers don’t charge fees to accept payments so charging fees will limit adoption and usage.

2. Partner with Mobile POS providers. Consumers can flip through their wallets and decide which account to link to their PayPal accounts or use to refill their Starbucks account. Develop a “top of the mobile wallet” marketing program to encourage customers to use your accounts for these mobile payments.

3. Tightly integrate P2P into mobile apps. Many banks and credit unions offer P2P services on PCs, but not on their mobile platforms. For many consumers, particularly young adults, P2P is more relevant on their mobile phones than PCs. This should be a major feature of your mobile app and promoted as such.

4. Encourage employees to “mobilize and evangelize.” Employees can be the most cost-effective ambassadors to encourage customers to adopt their institutions’ mobile services. But in many cases, employees don’t use their own institution as their primary bank and many of those who do, don’t use these technology services. Focusing on employees, particularly front-line employees in branches and at the contact center will have a big impact on customer adoption of these services.