At a time when the vast majority of interaction with online and mobile banking involves simplistic balance inquiries or funds transfer, expanding the number and variety of alerts can lead to a significantly higher level of engagement that can deepen the relationship with the customer.

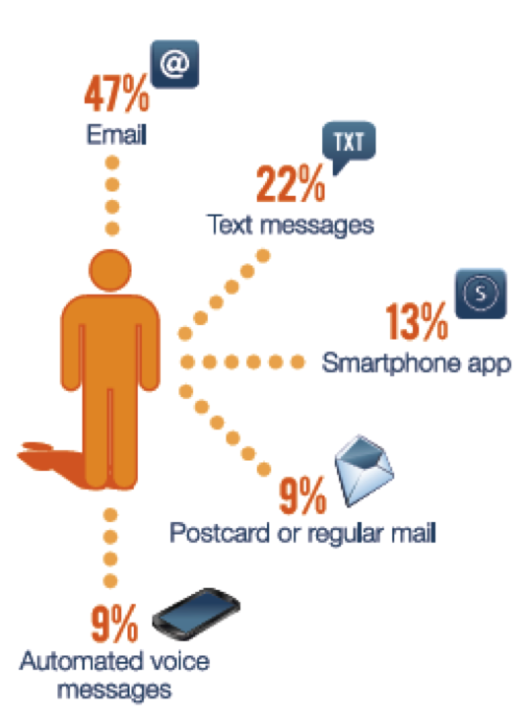

Varolii Corporation did research on mobile banking preferences entitled, Can You Bank On Your Banking App, which found that consumers differ significantly in the way they want to be contacted regarding their account. Some of these preferences may be correlated with the way in which they are currently being notified by their financial institution.

With such a wide variety of preferences, banks and credit unions must find a way to economically tie their alert system to a unified system of engagement that does not confuse the customer with too many notifications but still allow the customer a degree of customization. The key is to ensure that time-critical information is delivered to the customer in a manner that both informs and allows for immediate action.

“An enterprise alert strategy should include a wide variety of alerts distributed via multiple end points and devices,” says Jim Tobin, senior vice president and general manager, Mobile Solutions from Fiserv. “This will enable financial institutions to serve customers at different stages in their lives while keeping pace with regulatory demands.”

Types of Alerts

While the origin of alerts were to notify customers of overdrafts or potential fraud potential, the variety of alerts within downloadable applications has expanded significantly over the past 18 months resulting in an increase in engagement and a better potential customer experience. In the past, the majority of alerts have involved a one-directional flow of information from the bank to the customer. Examples include:

- Balance alerts: these could include overdraft or NSF alerts

- Scheduled alerts: could be balance or other insight delivered on a scheduled basis

- Event-based alerts: Could be based on a bill payment or potential fraudulent activity

While the majority of the above were usually done via email, the movement to using SMS channels opened the door for potential conversations between the bank and the customer. This expanded to ‘push’ notifications that allowed customers to instantly take action on an alert.

Push notifications enable customers to not only view an alert, but initiate a transaction in response to an alert within a secure app . . . in real time. For example, instead of simply getting notified that there is a low balance on an account, the alert can include a response option that allows for a transfer to be made using the mobile device. This deepens the engagement level, provides the customer more control and ultimately increases customer satisfaction.

As the use of smartphones continues to grow, push notifications are the expected level of engagement for ‘Customer 3.0’.

“With push notification, financial institutions have an opportunity to transform their existing alerts offering from a reactive, event-driven service to a proactive personal financial management (PFM) tool,” says Fiserv’s Tobin.

According to Fiserv, Push notification uniquely provide the ability for financial institutions to evaluate and measure alert programs. Unlike text and SMS, push notifications within the mobile banking app are not limited by carrier policy restrictions. For this reason, push notifications open the door for innovation and facilitate Enterprise Process Management (EPM) with the ability to measure the value of alerts.

Bottom line, an expanded alert strategy with the resultant engagement by customers can transform a one-way, static alert offering into a proactive personal financial management tool.

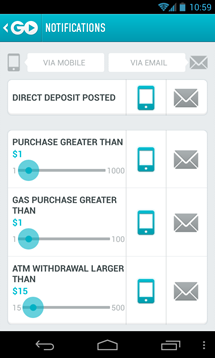

Not surprisingly, the new digital banks (Moven, GoBank and Simple) as well as several banks overseas have leveraged the power of mobile push alerts the most effectively. The options available and the ability to personalize the alert ‘experience’ can be seen below.

Monetizing Alerts

While most banks have been reluctant to charge a fee for almost anything historically, some institutions (most notably U.S. Bank and Regions Bank) have built a strategy around charging fees for ‘premium’ services.

In a report from Market Rates Insight entitled, Growth and Revenue Potential of Emerging Financial Services, evidence is provided that banks and credit unions are missing an opportunity to charge for services that go beyond basic. While not covering push notifications per se, this 168-page study covers 13 different emerging financial services, with insights into fee optimization, targeting, institutional differences and bundling options.

One of the services they do cover is the ability to charge for identity theft notifications which could be one of the many push notifications offered by a financial institution. According to the research, 82% of the households surveyed said they were likely to use identity theft alerts, with an average acceptable monthly fee of $4.07. The level of acceptance and perceived value of the service was not impacted significantly by either type of institution or type of customer (while women did value the alert slightly more than men).

According to Dr. Dan Geller from Market Rates Insight, “Staying informed through alerts is highly desired and valued by consumers. Nearly nine of ten banking customers want identity theft alerts, and nearly eight of ten banking customers desire low balance alerts.”

While I realize the value of an identity theft alert is definitely more than a basic alert, I believe there are alerts that the customer could receive that could be charged for as part of a bundle. For instance, the ability to charge a small monthly fee (let’s say $2.00) for the following expanded set of alerts could be tested:

- Credit card or checking account low threshold alert

- Upcoming bill (within 2 days) where available funds are not sufficient

- Large recurring bill notification (15 day notice) for mortgage, rent, car payment, tax bill, etc.

- Customized personal notification (owe a friend, non-financial promise made)

- Location-based alerts possible because of mobile GPS (new location alerts, travel alerts)

- Integrated personal calendar

Developing an Enterprise Alert Strategy

According to Fiserv, an enterprise alert strategy should include two way information flow and should be seamlessly integrated with all banking channels to support information access and management reporting. It should be both easy to enroll for and easy for the customer to make changes to preferences or to opt-out.

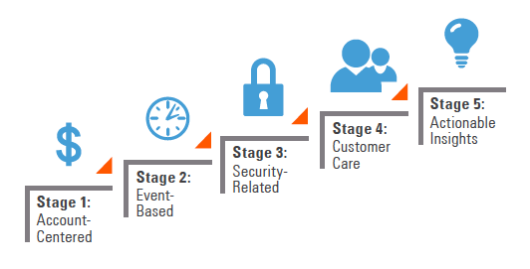

Since the potential for a broad-based alert strategy can be difficult to implement, Fiserv recommends a phased approach with different stages to implementation including:

- Step 1: Account-centered alerts that are specific to account activity (low balance, direct deposit, large debits)

- Step 2: Event-based alerts that indicate when an event may prompt a follow-up action (bill payment due, P2P request)

- Step 3: Security-related alerts that notify the customer when accounts may be compromised (international charges, password change)

- Step 4: Customer care information that can be initiated by the customer or the financial institution (CD maturing, lease up for renewal)

- Step 5: Actionable insights that provide financial management tips and guidance based on the customer’s activity (changes in financial activity compared to historical data)

While it may be difficult for some banks or credit unions to reach the final stage of implementation, digitally savvy and mobile-first ‘Customer 3.0’ expects this level of partnership from their financial institution. While providing such an array of alerts may seem like we could bombard the customer with communication, today’s alert strategy keeps the customer in control of what they want to see and what they don’t find important. The key element is providing choice.

Marketing of Alerts

Unfortunately, the adage “If you build it, they will come.” doesn’t usually apply with mobile banking applications. In other words, just because you have a robust, interactive alert capability doesn’t mean that customers will take advantage of this opportunity (assuming they can find the option on their online and/or mobile banking site.

Banks and credit unions should focus early efforts on those customers most likely to want and use alerts actively (low hanging fruit). These would most likely be those customers who already are using online and/or mobile banking actively and would best understand the benefits of customizable alerts.

Messaging within the online and mobile banking platforms is the least expensive and most effective way to begin. Fiserv suggests segmenting the target audience by digital personas to determine which alert(s) would be most valuable for each segment.

Beyond messaging within the online and mobile banking sites, other effective ways to communicate the benefits and use of alerts include:

- Frontline staff: leveraging the referral power of customer-facing personnel

- Email: a series of email communication regarding alerts with direct links to preference pages on the customer’s online banking site (Don’t forget the power of engaging offline customers as well)

- Ad campaign: Because of the innovative nature of robust alerts, ad campaigns have been used as a way to acquire new mobile-first customers

- Branch and ATM signage: While branch traffic is less than in the past, branch and ATM signage is still effective at raising the awareness of customers who may or may not use online or mobile banking

- ATM receipts: One of easiest ways is the use of QR codes on ATM receipts to encourage both the sign-up for mobile banking but the selection of alert preferences. Linking to the alert marketing page of a bank, these receipts are an inexpensive way to reach mobile customers and prospects.

Banks and credit unions have a unique opportunity to expand the functionality and engagement of both online and mobile banking by developing an enterprise approach to alerts that satisfies customer needs, addresses regulatory issues and can generate revenue. Since the implementation of a robust alert strategy is still in formative stages, financial institutions have a unique opportunity to develop both a standard (free) set of alerts along with premium (fee-based) alerts that customers value and are willing to pay for.

This is a great time for banks to step up to the plate to provide a service customers will value and to generate needed fees at the same time. The question is . . . will we give another innovative set of services away for free?