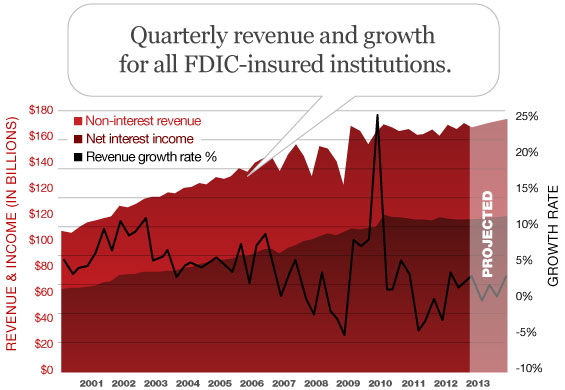

Overall banking industry revenue is at record levels, and is finally starting to growth modestly. Measured as revenue for all FDIC-insured depository institutions — industry revenue was over $172 billion for 3Q12, and will be higher for 4Q12 when the data come out. That exceeds the prior peak revenue of just under $172 billion in 1Q10.

What has kept revenue up for the industry as a whole has been a significantly larger balance sheet. Industry deposits are 28% higher than five years ago — due to Federal Reserve macroeconomic policy that pumped deposits into the system — while overall assets are 12% higher. This has allowed banks to earn spread revenue for a larger pool of earning assets.

However, while revenue is high, growth of industry revenue has been in short supply. Until recently, revenue had essentially been flat for the industry for several years — due to a combination of limited loan demand, low interest rates and regulatory “hits” to fee revenue. Industry loans on balance sheets have fallen 3% in the last five years (down 7%, if adjusting for an accounting affecting securitized credit card balances). Net interest margins have been drifting downward, awaiting a fuller economic recovery. And regulation has reduced consumer banking fees from credit cards, checking overdraft and debit interchange.

Recently we are finally starting to see some relief from the revenue drought. The second half of 2012 saw positive revenue growth — albeit in the very low single digits — arising largely from loan growth in some C&I, auto and other loan categories, and the resumption of modest retail fee growth. We see this trend continuing in 2013, and even expanding a little, and expect to see 2013 revenue growth in the low- to mid-single digit range.

The revenue drought has not affected all banks equally. Some banks are enjoying outsized revenue growth, especially those with large fee-generating businesses in mortgage origination, indirect auto, asset management, brokerage and insurance. Banks that do well will be those that can out-compete for lending in the growing areas of demand, deepen customer relationships and expand ancillary fee revenue businesses.

Lee Kyriacou is Managing Director with Novantas. Lee’s industry research, forecasts and opinions leverage twenty-plus years in consulting and banking to offer industry analysis and insights. His banking experience includes head of bank-wide financial planning and analysis, as well as strategy and M&A roles, at two top ten banks. Lee also has an banking business focus in consumer and wholesale payments and payments-related lending.