Once the banking industry spoke of the payments system as “theirs,” and resisted all attempts to muscle in on their turf. It didn’t work. Challengers to the industry’s dominance have grown to become mainstream rivals. Witness the ongoing boom in “buy now, pay later” payments and the growing impact of companies like PayPal that have turned its P2P app Venmo into a full-fledged retail payment instrument.

Increasingly the payments side of banking has had to get used to sharing the business with both rivals using new rails as well as competitors sharing industry rails.

Non-Stop Struggle:

Banking is playing an endless game of payments “Whack-A-Mole.” But in this game, no matter how hard you hit, the moles rarely go down. In fact, they multiply.

While the industry keeps striving to do its own innovating, countering outsiders’ forays sucks up energy. Competing in the BNPL space is no simple matter, for example, as we’ll examine — but it also introduces unanticipated means of making money from the trend.

“In many ways, 2022 will see a mash-up of preexisting innovations and technologies but delivered with a new sense of purpose, as their time (and usefulness) has finally come.”

— Forrester, Predictions 2022: Payments

1. The ‘P2P’ Wars Will Continue Unabated

To counter the original providers and use of P2P — which once was truly person-to-person payments — major banks came together to create Zelle and have had notable success in terms of adoption and transaction volume. However, Zelle so far doesn’t offer the consumer-to-business payment options that players like PayPal, Venmo and Block’s Cash App do. If banks offering Zelle were to add this use to it, they would be competing with payment forms they already offer. Trying to make money from Zelle as it exists is difficult.

“It’s kind of hard to walk back from ‘free’,” says Barry Baird, Head of Payments Capability and Delivery at TD Bank. This is one example, according to Baird, of the difficulty the industry faces in trying to capitalize on areas of success. “How do we do it in a way that’s a win for the customer and a win for the bank?”

A more negative pronouncement comes from Forrester, which, in a payments prediction report, states: “U.S. consumers are well served by fintechs, and the banks’ homegrown solution Zelle will struggle to build further market share. Market-dominating fintech rivals such as PayPal, PayPal’s Venmo, Apple Cash and Square’s Cash App continue to pump in features as part of integrated payment suites.”

Read More: Will ‘Chuck’ Give Smaller Banks an Edge in P2P Versus Venmo, Cash App and Zelle?

2. Despite All the New Stuff, Cards (and Cash) Roll On

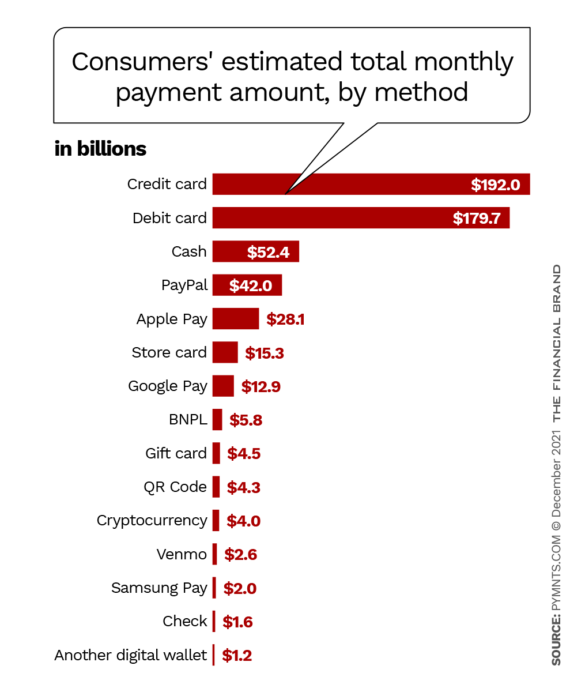

In November 2021 PYMNTS.COM surveyed nearly 3,600 consumers and found that while alternate payment methods are growing, debit and credit card transactions continue to dominate overall. And, amazingly, even in the wake of the pandemic, cash remains in third place.

Why is cash is ahead of mobile wallets? PYMNTS has found that consumers prefer contactless cards to mobile wallets. Another wrinkle is that buying groceries, a common payments need where mobile wallets might be normally be used has shifted online. PYMNTS found that one in four consumers are buying their groceries online now, so they need neither contactless card nor mobile wallet.

Calling the Shots:

The consumer ultimately is in charge of where payments will go, even when technology beckons.

Read More: 18 of the Most Stunning Credit & Debit Card Designs in Banking

3. BNPL: The Payments Wild Card

It’s impossible to discuss threats to traditional payments providers without discussing buy now, pay later service. This is simultaneously a payment method and a form of financing — much like credit cards, actually.

Financial Product of the Decade?

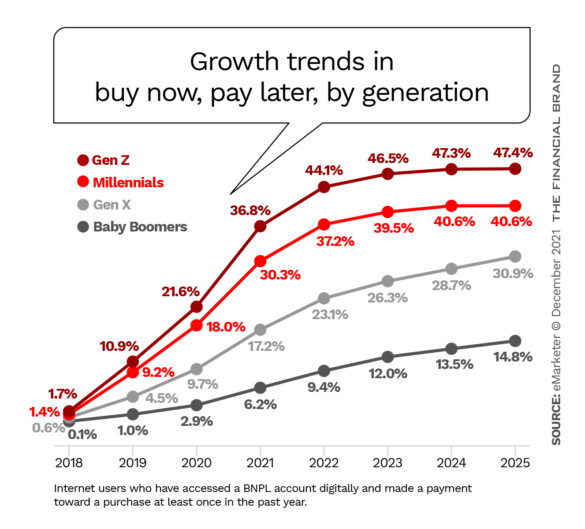

Insider Intelligence’s eMarketer projects that in 2022, one out of three American shoppers will buy something using some variation on BNPL.

While BNPL growth has been rapid, clearly this payment method has the greatest appeal to Millennials and Generation Z.

Significantly, and supportive of PYMNTS findings mentioned earlier, for all the growth, Insider Intelligence estimates that BNPL represents about 1% of U.S. retail ecommerce dollars.

That said, this revival of the sleepy old layaway plan of yore has gotten banking’s attention, especially as major players like Amazon and Walmart.com have added BNPL options. In early 2021 CBInsights projected global BNPL spending could hit or exceed $1 trillion, noting that total U.S. spending via credit, debit and prepaid card comes in around $8 trillion annually.

In 2022 banking will press harder with an aggressive comeback to BNPL, but there will be obstacles and sticking points. A wildcard for all players has been the stance of Biden banking regulators.

Betting had been on the Consumer Financial Protection Bureau taking action in 2022, but in mid-December 2021 CFPB opened a massive inquiry, asserting data-gathering authority, at the least, over five major BNPL providers: Affirm, Afterpay, Klarna, PayPal and Zip. The initial effort is an order to provide answers to a ten-page list of detailed questions about each company’s BNPL products and practices. This is worth exploration by would-be bank BNPL lenders. Three key concerns for CFPB are consumers’ accumulation of debt, especially to multiple providers; the possibility that BNPL providers are not “adequately evaluating what consumer protection laws apply to their products,” including lack of disclosures; and how the providers are harvesting data about borrowers and how they are monetizing that data.

The use of the detailed questionnaire and the assertion of authority under the open-ended jurisdiction granted to CFPB strongly resemble the bureau’s approach to six big techs in October 2021. There’s overlap, too. That group included PayPal and also Square (now Block), which is in the midst of acquiring Afterpay. In a statement CFPB indicated it would be cooperating with other federal and state regulators as well as agencies in Australia, the U.K., Sweden and Germany.

M&A is also in the BNPL forecast: “A handful of major banks will acquire BNPL players like Amount, Sezzle, or Spitlit to offer BNPL to their customers,” says Forrester.

Thus far, the acquisition to watch has been the pending deal for Block (formerly Square) to buy Affirm. Forrester adds that the BNPL companies will “focus their merchant-selling strategies on value-added services and alternative distribution networks.” Klarna’s efforts to go beyond negotiated BNPL deals with merchants to introduce the ability to buy with Klarna from any merchant could be a game-changer.

Just how a bank would dive in to compete with established independent players would depend on what it already does, according to Vivek Jetley, EVP and Head of Analytics at EXL. The company has been working with banking companies such as FNBO to implement BNPL.

“It’s a solution that’s in great demand right now and so every banking institution seems to want to get into the space,” says Jetley. “But it’s been our experience that most aren’t really ready. They haven’t thought through what it takes to get BNPL implemented.”

For example, for many institutions a sticking point is whether BNPL belongs on the bank’s card systems or its installment loan systems — or perhaps a new third system. A major BNPL program requires investment in ancillary functions, such as specialized collections. Because of the short-term nature of many payment plans, BNPL is a different creature than either cards or installment loans, says Jetley.

Even once a bank gets underway, the challenge will be whether the volume is good volume or not. Jetley says the population using BNPL typically skews to lower FICO scores.

“At some point when credit losses come back to normal levels, I think you will see credit risk exposure for BNPL running higher.”

— Vivek Jetley, EXL

How far the boom in BNPL could go is also being questioned. TD Bank’s Baird says his institution has been weighing how much growth potential there is for newcomers — or whether it may be “a wave that will crest and then begin to recede a bit.” The CFPB probe is another factor that newcomers will be watching closely.

4. It’s A Wallet! It’s a Platform! It’s Super App!

The direction of many financial services and even some ecommerce services has been fragmentation, leaving the overall management to the consumer.

“Clearly, customers are drawn to the idea of a one-stop shop, which gathers up and organizes the best features of all their apps — like an operating system for their life,” states the JPMorgan Chase white paper, “Payments Are Eating the World.” The super app fulfills this desire, the white paper explains, bringing together both lifestyle and financial services functions, granting access and the ability to pay for many things people buy, with ease. The paper points out that this serves the needs of merchants too, giving them access to an audience and sparing some of the cost of acquiring customers.

Almost paradoxically, the Insider Intelligence report maintains that “super apps can solve a problem that consumers of all ages wrestle with: choice overload.” The paper notes Deloitte research that one out of three consumers feels they are drowning amid the multiple devices and subscriptions they maintain.

Insider Intelligence suggests that PayPal, Revolut or Block, through Square and its Cash App Pay service, could launch the first true U.S. super app in 2022. The paper says the first two have already got the financial part down, and what they need to do is increase the commerce part, pulling more choices under the app’s umbrella. Block/Square has the advantage of the huge Square seller base, but PayPal’s recent deal to add Venmo to payment options on Amazon in 2022 represents a “super app via partnership” strategy.

Super Apps Ramp Up:

Forrester predicts that 2022 will end with at least 20 bank, retail and telco super apps “duking it out” for supremacy.

67% of respondents to a survey by PYMNTS.com want a super app for managing all their digital activities.

“Consumers want to consolidate their digital experiences into a single interface,” the study states. The publication indicates ten functions that could all conceivably take place within a super app: payments, banking, travel, communication, everyday living, obtaining food, shopping, working, entertainment and health.

(Read More: PayPal Wants To Become The Banking World’s Next ‘Super App’)

5. Embedded Payments (Spending You Hardly Feel)

It is said that the men of the British Royal Family have no pockets in their trousers, because they don’t carry money. (We don’t know if they have payment apps on their smartphones.) The idea is that all that dealing in money gets handled by minions.

Embedded finance is something like auto-minions for everyone. More and more purchases are and will be billed and paid automatically, says TD Bank’s Baird, from share-ride charges to buying gasoline. The payment instrument may be your phone, a transponder in your car, or a chip embedded somewhere.

This is actually a subset built around increasing connectiveness of automobiles, with data flowing back and forth all the time, according to research by McKinsey. Payments for tolls have already become painless and invisible. The ability to orchestrate insurance payments through the vehicle itself — with potential for variability based on measured driver behavior — can now all be in the background as well.

The impetus to add more embedded payments will grow as connectivity improves. In a fireside chat during a Citibank analysts conference, Craig Vosburg, Chief Product Officer at Mastercard, said that more and more devices from vehicles to appliances will be rolled in.

“When you combine that with the power of something like 5G technology that’s being introduced around the world, the number of connected devices and the ability to effectively establish an internet session between any of these devices creates the ability for all of them to transact,” says Vosburg.

One danger with all this convenience is leaving the consumer completely out of things, Baird points out, especially if embedded finance may at some point involve a credit transaction.

“You want to make sure there’s some purposeful checkpoints with the customer, some ‘speed bumps’ to understand the terms as they are entering into a transaction,” says Baird. He says this is especially of concern with people who came of age during the financial crisis. “They are already fearful about what credit spending can look like.”

6. Real Time Payments Keep Grinding Forward

Faster payments, real-time payments — is the American consumer asking for that?

The Clearing House’s Real Time Payments program already pulls in “70% of U.S. demand deposit accounts (DDAs), and the network currently reaches 61% of U.S. DDAs,” according to the program website. Meanwhile, the Federal Reserve’s FedNow program continues to work towards full implementation in 2023, a year ahead of original plans. FedNow Service, currently being tested by a number of financial institutions, would enable individuals and businesses to transfer funds in seconds.

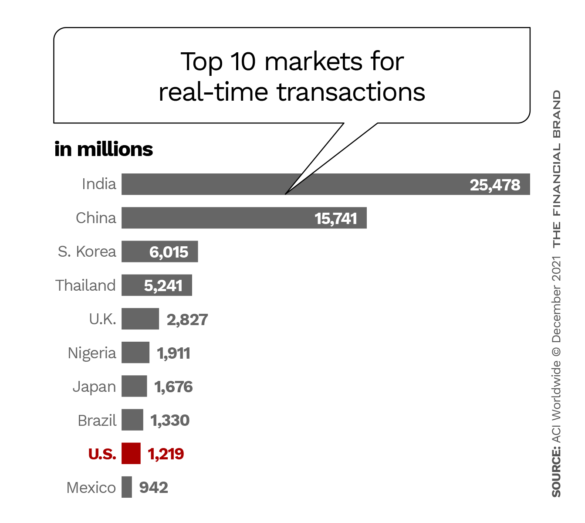

The U.S. is substantially behind a good part of the world on this front, with India actually leading the way, according to research by ACI Worldwide.

Ironically, TD Bank’s Baird says many consumers think they have had real-time payments all along, not appreciating the difference between delivery of payment instructions via instruments versus actual settlement.

“Today, the settlement is not instant, but the customer never cared about settlement anyway,” says Baird. “In fact, I might argue that the customer kind of doesn’t mind if there’s float.”

Baird sees much more opportunity in the U.S. on the commercial side.

“The business side is where things are much slower and they do care about whether a payment comes in now or 24 hours from now, because it actually makes a significant difference when I’m moving multiple commas’ worth of money around,” says Baird.

Baird sees the ability of new systems to carry additional data to be a less-discussed strength that financial institutions can tap for both consumer and business payments services.

“You can put invoices in with a payment request, and the recipient can open it, review it, and pay it all in one place and time,” says Baird. “We’ve never had that capability on standard payment rails.”

Down the road new patterns in payments will emerge. The JPMorgan Chase white paper suggests that the rise in gig and contract worker ranks has created a strata that likes to be paid asap.

“Creators and gig workers want to be paid instantly. This means daily or even hourly payroll could become a reality. In such a world, daily mortgage payments or tax payments wouldn’t be inconceivable either.”

— From “Payments Are Eating the World,” from JPMorgan Chase

7. Mastercard and Visa: Bloodied But Unbeaten

With the announcement that Amazon made in late 2021 that it would stop accepting Visa payments in the U.K., some took this as a sign that the authority and centrality of the two payments giants was beginning to erode. Add in BNPL and its relationship to credit card spending and borrowing and it would seem there’s trouble for the two companies.

But, as said earlier in this article, payments streams don’t stick to their own lanes anymore. In an analysis of the fortunes of the two companies, Sanjay Sakhrani, Managing Director at Keefe, Bruyette & Woods, suggests that the risk to the companies is overstated.

Debit cards are the most common way BNPL installments are repaid, he points out. They account for 70% of repayments. In addition, he says, a typical pay-in-four plan means four repayment transactions via debit or credit versus one purchase transactions.

Sakhrani also pointed to the benefits that open banking will bring to both companies, including capture of new spending flows and enabling of “multi-rail money movement.”

During the Citibank analyst conference Vasant Prabhu, Visa’s CFO, pointed out that the pandemic’s encouragement of digital payments continues to push up volume for Visa and for issuers.

“It’s not just consumers getting used to it, but it’s about infrastructure getting better,” said Prabhu. “It’s about merchants getting better at ecommerce and about even face-to-face merchants upgrading the way that they accept digital payments.

As open banking becomes the norm, this will open more rails to organizations like Visa. “Our job is to enable money movement of all types,” says Prabhu. “We want to help you move your money and we’re agnostic about the rails we use.

“In the past five years we’ve gone from serving just consumer payments to P2P to B2C to all kinds of B2B. It’s all incremental and open banking is one way that is facilitated.”

— Vasant Prabhu, Visa

Both card companies are partnering more and more with fintechs, as well.

“There’s a whole range of new technologies and technology enablers that we work with across the ecosystems that are making card acceptance available more broadly to a wider range of businesses through new technologies that are lower cost than traditional acceptance technologies,” says Mastercard’s Vosburg