Buy now, pay later (BNPL) offers are thriving on the discretionary consumer spending that was previously the domain of credit cards. According to research by Raddon, a Fiserv company, 28% of consumers have used a BNPL option within the past year.

Major announcements have been made by several players entering the BNPL space due to the lucrative financial opportunity it represents. For example, in July, Apple and Goldman Sachs announced their intent to launch Apple Pay Later. In August, Square announced its planned $29 billion acquisition of BNPL provider Afterpay. And Affirm — currently the No. 1 player in BNPL with over seven million active consumers conducting approximately 15 million monthly transactions — announced a strategic alliance with Amazon that will make its flexible payment solution available to Amazon customers at checkout. Even more recently, Mastercard threw its hat into the BNPL ring.

Rapid Uptake:

New research shows that almost three out of every ten people used a BNPL product in the last year.

It’s no understatement to say the profile of the BNPL payment choice is skyrocketing and payments industry behemoths are betting huge on its success.

The rise of high-profile BNPL payment options is certain to have an impact on credit card spending and the profitability of credit card programs – with negative consequences for traditional financial institutions that rely on revenue from credit lines and interchange.

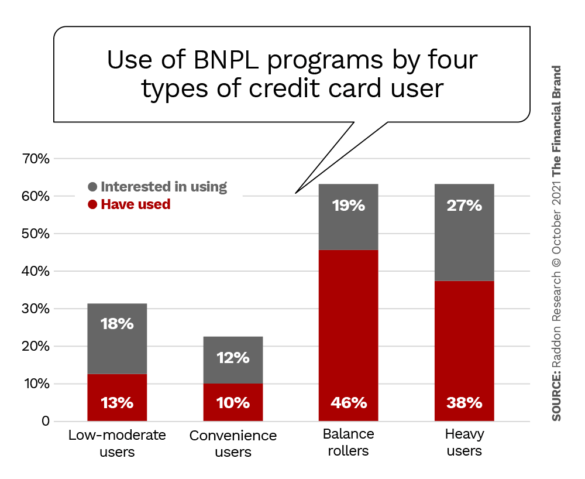

Raddon research indicates growing interest in BNPL payment options among all types of credit card users but particularly among users cherished by financial institutions: consumers who roll their monthly balances and deliver fee income, and power users who transact frequently and produce significant interchange income.

The consumer attraction to BNPL is easy to understand: it presents a low cost, or lower cost, way to acquire the goods they desire “in the moment.” Unfortunately for many shoppers, the BNPL option also feeds the temptation to spend more money than they would have otherwise, and the resulting purchases can strain finite financial resources and add stress to a consumer’s life.

Don’t Stand Idly By:

BNPL represents an opportunity for banks and credit unions to reassert the primary financial role they’ve worked hard to establish over decades to be a trusted financial partner and the lender of choice.

By implementing new digital offerings, you can provide seamless consumer payment journeys that provide cardholders with convenience and security, and elevate your credit card to top-of-wallet status for payment choices. Here are three options to consider:

1. Make Credit Cards Digitally Available

Many consumers are choosing buy now, pay later because it is the offer that’s extended at the time of purchase. Making credit cards just as easy to use provides you with an opportunity for your card to be chosen. To level the playing field and compete successfully, credit cards can be issued digitally and available to consumers to provision into their digital wallets immediately.

This quick process will give consumers instantaneous access to a new card and a simple way to use it at checkout. No longer will consumers need to search for a physical card or key in card details to pay manually. Saving these precious minutes by allowing a purchase with the touch of a fingerprint makes it easier for consumers to complete a purchase for an appealing merchant offer.

2. Provide a Secure, Information-Rich Environment

One of the main concerns consumers have about credit cards is their own usage and spending patterns. Providing cardholders with detailed insights regarding their spending and enriched transaction information makes it easier for them to understand their purchasing habits and empowers them to make informed buying decisions.

Spend insights need to be delivered with meaningful data, while also being simple enough for someone to understand at a glance. Providing high-level views that include relevant data like spend by category and spend by month will provide your cardholders with significant insight into where their dollars are going and the ability to measure month-to-month changes.

An enriched set of transaction information can make the difference between a panicked consumer who is worried about fraud and someone who is secure knowing that each purchase is one they’ve made. The transaction data needs to include actual merchant names, retail locations for physical purchases, the transaction amount, and purchase date.

The more details you’re able to provide, the better informed your consumer will be. Ideally, transaction details will include merchant contact information so consumers can self-serve with the ability to make any inquiries about their purchase directly.

3. Create Offers that Make it Easy for People to Say ‘Yes’

Many credit cards already offer the ability for cardholders to pay off larger purchases in planned installment payments. This capability provides the consumer with confidence that their debt will be paid quickly and often provides them with a lower interest rate – all while capturing the spend on your financial institution’s credit card.

Communication remains one of the key concerns for credit card issuers looking to be the payment method of choice. Buy now, pay later options show up at the point of sale, and financial institutions need to make sure their offers are at a consumer’s top of mind in this critical moment as well.

Get There First :

One reason BNPL programs are so popular is because they are at the first thing a consumer sees at the point of sale. Banks and credit unions can compete with these services by providing real-time contextual offers.

One way to make sure cardholders keep their credit card as a first-choice payment option is to provide location-based contextual offers via text or push messages. As your cardholder enters a furniture store, push an offer to their phone – “In the market for a new couch? Any purchase over $100 can be split into 6 monthly payments with a 0% interest rate.”

A message as simple as this reminds consumers that your card is available and a new credit line, like the ones provided by BNPL, is not necessary.

Another option is to provide clear communication about the availability of installment plans prior to purchases. Include information about the plans in your regular consumer-focused communications that you distribute and share – like emails, physical mailings, or ads – so cardholders know they can set up a payment plan post-purchase.

Compete – and Win

Buy Now, Pay Later might currently be the hottest thing in payments, but trends can cool quickly. In today’s world, the consumer payment experience is a significant factor in engendering trust and loyalty. You can successfully compete against BNPL and be the payment method of choice by creating and delivering a purchasing journey that engages and delights your credit cardholders.

Additional Resource: How to Elevate the Digital Experience for Cardholders