Credit cards may be losing some of their shine.

Long a favorite of consumers, satisfaction with — as well as usage of — credit cards has declined over the period of 2020 to 2021. Even the humble debit card surged ahead of credit cards this past year in terms of total dollar amount spent.

A combination of increased financial stress, lack of responsiveness and misaligned terms and rewards have created this perfect storm that led to a decline on consumer satisfaction with credit card issuers, according to the J.D. Power 2021 U.S. Credit Card Satisfaction Study. Meanwhile, spending on credit cards declined by 9% in 2020, according to a separate study from PULSE and Oliver Wyman.

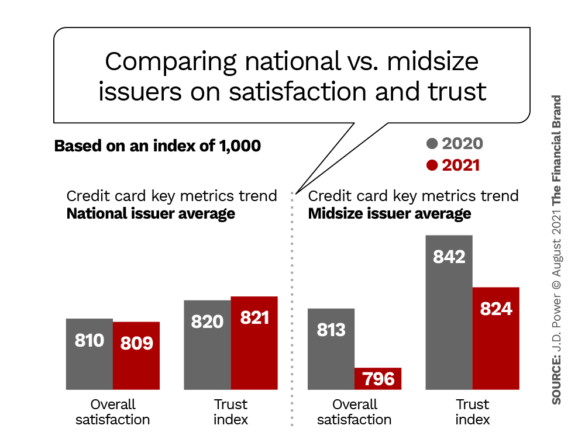

As with most of its satisfaction surveys, J.D. Power uses a 1,000-point scale with its annual credit card study. Overall satisfaction with credit card issuers fell to 805 from 811 the year previous. The decline is even more pronounced among midsize card issuers, among which scores declined by 17 points to 796.

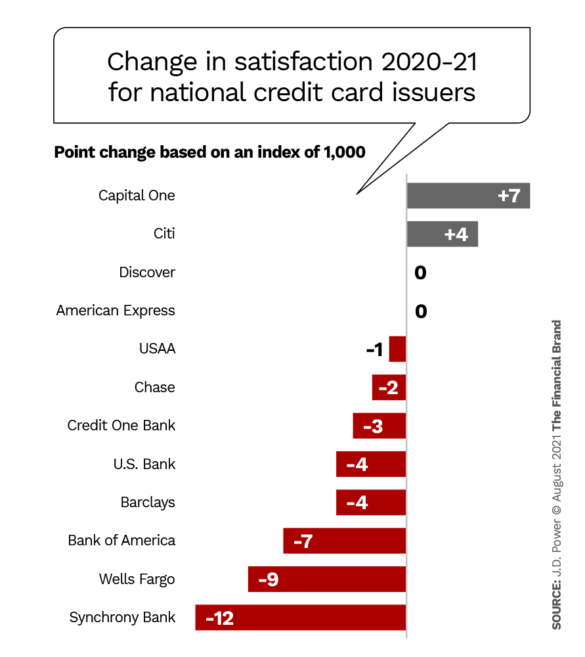

American Express ranked highest in customer satisfaction among national issuers included in the study, with a score of 838. Discover (837) ranked second and Capital One (815) ranked third. (USAA, at 860 would have ranked highest, but is not officially included because it only issues cards to consumers with a military connection.)

Among the midsize institutions, Goldman Sachs was the standout, with a score of 864. BB&T, Huntington and PNC rank second in a tie, each with a score of 817. (Navy Federal, would have just edged out Goldman with a score of 866, but like USAA, is not eligible for the ranking because of membership restrictions.)

Trending Down:

Overall consumer satisfaction with credit cards went down in 2020, led by midsize issuers, but Goldman Sachs was a standout.

“While there are some bright spots this year among individual issuers, the pandemic really broke a multi- year trend of improving satisfaction,” says John Cabell, Director of Banking and Payments Intelligence at J.D. Power. “The industry missed the mark on supporting customers’ changing needs when many were facing significant financial challenges. Whether through blunt actions, such as tightening credit limits at the very moment when customers were most reliant on their cards as a source of short-term funding, or through lack of customer service accessibility, credit card issuers experienced declines in overall satisfaction, trust, brand perception and Net Promoter scores this year.”

Read More:

- Millennials and Credit Cards: Separating Fact from Myth

- Credit Card Cash-Back Metrics Driving Retail Strategies

Headwinds for Regional Bank Issuers

Midsize issuers faced declines across a range of key metrics, including satisfaction with credit card terms and benefits. One reason for this, Cabell notes, could be lackluster communications.

“It probably depends on the issuer to some degree in terms of whether they have a real interest rate or fee problem or just a communication issue,” Cabell tells The Financial Brand. “There are certainly cases where the complexity of some terms and conditions was not communicated sufficiently or not understood by the consumer.”

Another area where midsize issuers lagged was in not adapting quickly enough to tailor rewards programs to new spending habits brought on by the pandemic in 2020 (more detail on this below).

Co-brands Did Better:

Generally speaking, retail co-branded cards, including the Apple Card, fared well during the pandemic.

One midsize issuer that bucked this trend was Goldman Sachs, which benefited from its partnership with Apple and the Apple Card. Goldman Sachs performed highest in the categories of benefits and services, communication, credit card terms, interaction, key moments and rewards, according to the survey.

“This is what we saw with other retail co-branded cards as well,” he says. “Consumers were still happily using their Sam’s Club card or Costco Card quite a bit, for example.”

Misalignment of Rewards Programs

A major concern for many issuers of all stripes was misalignment of rewards programs. The study found that misalignment between rewards programs and spending patterns had a measurable impact:

- An average of $756 in lower monthly spending.

- A 7 percentage-point greater likelihood of switching cards.

- A 4 percentage-point greater likelihood of citing a problem.

This misalignment was more common among the 53% of cardholders who struggle to pay bills and/or have no financial planning, J.D. Power states.

While larger issuers were generally quick to adapt their programs to new spending habits, midsized issuer segment banks lagged in revamping rewards, Cabell says, meaning that some cardholders got stuck with outdated cards.

“If you’re a consumer paying an annual fee on a travel rewards card, but not accumulating any points, that could leave a sour note,” he adds.

Key Takeaway:

Consumers who have the right rewards program tailored to their spending habits tend to be more engaged and spend more on that card.

Customers who use cards with rewards programs tailored to them tend to be more active. The study found that, on average, customers whose spending and usage does not align with their rewards card spend just $503 per month on their primary card, compared to $1,259 for those who are aligned with their card.

Fintechs: Both Friend and Foe

Consumers who linked their card to a mobile payment service (e.g. PayPal in-store or Apple Pay or another mobile wallets) generally expressed higher satisfaction, the study found. One-third of cardholders in 2021 are using a mobile payment service with their card. Satisfaction among these cardholders is up to 39 points higher for mobile interaction than among customers who use the issuer’s mobile services alone.

This is a bit of a double-edged sword, Cabell observes. While issuers can expect happier and more engaged customers when they link their card with a mobile wallet, there is also the risk that the consumer associates that satisfaction with Apple Pay, say, rather than the card itself contained in the wallet.

Further, he notes, it can create issues down the road if consumers compare the issuer’s own mobile app negatively with the experience they have with the mobile wallet.

“It’s certainly a fuzzy line there in terms of benefit versus competition,” Cabell concludes.