There are about 365 million open credit card accounts in America, one million for every day of the year, according to the American Bankers Association. That’s more credit cards than there are people (328.2 million).

While that number may seem astronomical, credit cards appear to be faltering in consumer popularity, according to a survey of more than 1,000 U.S. consumers by global fintech for account-to-account payment company GoCardless.

In their place the debit card, along with alternative forms of payment such as Buy Now, Pay Later plans, are appealing strongly to consumers (especially among younger generations), the data show. P2P payments via Venmo, Zelle and Square Cash are another fast-growing payment option.

GoCardless cites the pandemic as a main driver of credit card depreciation, saying it “dampened the enthusiasm” for the popular card product. Respondents to GoCardless’ survey — conducted in June and July of 2021 — say they use their credit cards less because of financial concerns. That suggests the pronounced negative impact on credit card use in the early stages of the Covid pandemic may have produced long-term effects.

Almost half (46%) admit they’re wary of slipping into debt, one quarter (25%) say they worry about not paying off the monthly balance in full and another quarter say they’re even worried about making the minimum payment.

“The pandemic put people in tough positions financially, and that likely accelerated the move away from credit cards,” said Hiroki Takeuchi, Co-Founder and CEO of GoCardless in a statement, adding “this is part of a larger trend, particularly among young Americans.”

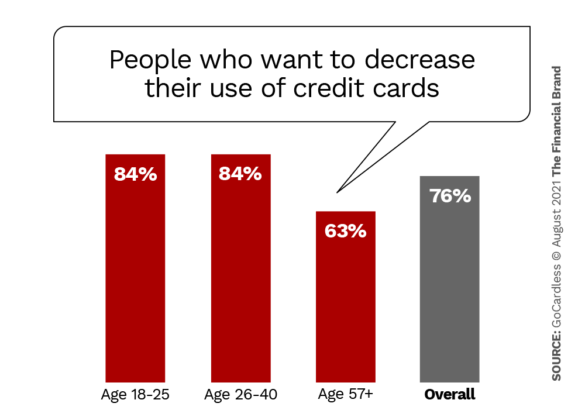

But, just how many people are trying to wean their credit card out of their wallets? GoCardless estimates more than three out of every four Americans want to decrease their credit card usage.

Financial institutions are already offering replacements for the average credit card. In addition to P2P options, several are launching reward checking accounts, which allow customers to make purchases from their primary banking account, while earning higher-than-average returns.

San Diego-based Axos Bank, for instance, offers a three-tier reward checking account, exchanging the poster child of credit card rewards — cashback — with a higher APY. Customers can get an interest payout of anywhere from 0.4666% to 1.25% (as of Aug. 1, 2021).

Read More:

- How Smaller Institutions Can Grab Credit Card Business Back from Megabanks

- Wells Fargo Launches Fresh Attack on Credit Card Market

- Cranky Business Customers Sound Off on Credit Card Features & Apps

A Generational Attitude Shift

Siamac Rezaiezadeh, Director of Product Marketing at GoCardless, tells The Financial Brand that while credit card use may decrease in the coming years, the industry certainly won’t die out overnight.

Nonetheless, card issuers shouldn’t ignore the glaring signs suggesting it could happen, especially as the next generations of banking customers continue to redirect how payments are made.

“The number of 18- to 24-year-olds who say they will use a credit card to pay for services like Uber or buy products on Amazon is less than half that of Gen X’ers,” Rezaiezadeh explains. “Credit cards will become much less relevant within a generation, if not sooner.”

It’s no surprise that Gen Z is at the forefront of the movement away from credit cards. Rezaiezadeh maintains they and Millennials alike grew up during a global financial crisis, observed multiple data breaches as the banking world shifted to a digital approach. Then, the pandemic struck.

“It’s been a transformational 10+ years,” he adds. “And it’s starting to show. It’s clear that the pandemic has dampened American enthusiasm for credit cards.”

Takeuchi agrees, going so far as to predict that credit cards will be obsolete in a generation or two.

( Read More: Millennials and Credit Cards: Separating Fact from Myth )

Terrified of the debt that Millennials say they suffocated from, Gen Z is determined to stay in the black.

As a result of the pandemic, 76% of 18- to 24-year-olds say they’re less likely to pull out their credit card, followed closely by 74% of 25- to 40-year-olds, GoCardless reports.

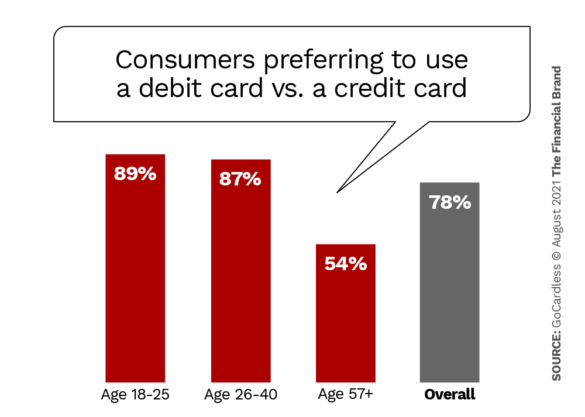

Interestingly enough, these two generations are not only comfortable with relying on their debit card over their credit card, but they also have a piqued interest in non-interest installment apps, such as those provided by Affirm and Klarna.

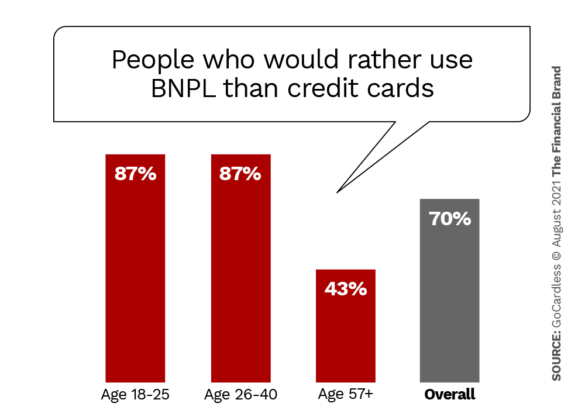

“The figures are higher among the next generations of shoppers — indicating a permanent shift in consumer preferences as Gen Z and Millennials increase their purchasing power in the coming years,” the GoCardless report states. “In addition to harboring a distinct dislike for credit cards, both cohorts revealed a striking preference for new forms of payment, including Buy Now Pay Later (BNPL).”

There’s Another Side Of The Coin

Not all experts believe that current trends point to a phaseout of the venerable credit card. For instance, the numbers referenced above could simply be results of pandemic scares.

In a November 2020 blog, Ron Shevlin, Managing Director of Fintech Research at Cornerstone Advisors, wrote that “Reports of credit cards’ death (or decline) are greatly exaggerated. Again.” He says that credit card use will rebound due to three factors: economic recovery, credit card rewards and the impact of credit builder cards.

“According to Cornerstone Advisors’ most recent study, two-thirds of Millennials now have at least one credit card, and 40% have two or more. So much for being stigmatized,” states the outspoken Shevlin.

Richard Crone, CEO of Crone Consulting, told The Financial Brand in an interview for an earlier article that he believes “many purveyors of checking accounts are under the delusion that debit has overtaken credit for Millennials and Gen Z and will continue to do so.”

That is not the case, Crone maintains.

Products such as the Apple Card, “given its growth rate and capabilities and the actual numbers” clearly demonstrates how credit cards could very soon eclipse debit cards again as the preferred payments choice, states the payments consultant.

( Read More: Is Apple’s New Credit Card The Next Big Thing in Banking? )

Big Picture:

The Covid-19 pandemic changed how people bank and pay. However, the credit card might still have a bright future, even among the youngest generations.

Credit Card Usage: Down Then Up

So, maybe people aren’t losing interest in the credit cards themselves. It could be instead that people are leaning away from high credit card balances.

In November 2020, for instance, Experian reported that credit card balances in 2020 dropped for the first time in eight years, along with falling rates of credit debt.

The decline, however, was from a very high point. Over the course of the eight years prior to the pandemic, credit card debt was growing with no end in sight. It reached a record-high in 2019 of $829 billion, wrote Stefan Lembo Stolba, Data Analytics and Content Marketing at Experian Consumer Services.

However, 2020 quickly burst the bubble on that momentum. Balances fell by 9%, Stolba continues, “bringing total U.S. outstanding credit card debt to $756 billion, the lowest point since 2017.”

As the federal government funneled stimulus checks and offered financial assistance to consumers through unemployment programs. Some people used them to pay down their credit card balances and keep them low during the pandemic.

Things have already changed. Capital One, for example, reported that its credit card volume was up 25% in the second quarter of 2021 — not from 2020’s depressed levels, but from 2019, according to The Wall Street Journal. In time, there’s a good chance — if consumers continue to spend — that balances will soar once again. Not yet, however. Capital One’s average Q2 card balance was down 10% from the same period in 2019.

Food For Thought:

Good news: People may go right back to their pre-pandemic credit card habits. Bad news: there could be large groups of consumers who will continue paying off their credit card balances in full for years to come.

Lastly, it’s important to note as well that an instilled fear of debt is not the sole reason people broke away from the credit card. NerdWallet revealed in a June 2021 report that some credit card issuers reduced the credit limits of many of their cardholders in 2020.

Because of this, over one in three American cardholders (35%) say they plan to use their credit cards less. Another 23% also say they are going to reserve more money in savings in the future, just in case their credit limit is decreased again.

“If your credit limit gets cut, that eats into your emergency reserves,” Sara Rathner, a credit card expert at Nerdwallet, said in the report. “It’s ultimately more reliable to have a supply of cash savings on hand.”