New consumer research confirms that the historic events of 2020 not only boosted digital banking use, but also dramatically accelerated the fragmentation of banking. Consumers are now far more willing to establish primary financial relationships (PFRs) with non-traditional and non-banking companies.

In a study of 2,000 credit union members and 1,000 other consumers commissioned by CO-OP Financial Services, Ernst & Young (EY) found fintechs to be the greatest cause of consumers’ willingness to bank with multiple providers. Fintech domination of consumers’ financial relationships is a prospect no community financial institution can take lightly.

What It Means:

The fast-moving fintech threat forces community institutions to revisit experience and loyalty strategies to ensure they are on-par with modern expectations.

How Digital Impacts the Competitive Balance

As consumers changed their daily habits to rely more on digital-first brands, EY found digital channels to be a preferred method of engagement for banking, categorizing 88% of the survey’s respondents as digitally engaged. 73% said they regularly interact with their banking provider online or through mobile, and nearly one-third (32%) visit a branch less than monthly.

The pandemic crisis forced even late-adopter generations to give newer, digital and remote forms of engagement a try with their favorite brands and service providers. It turns out they liked it. Older cohorts have shown the fastest growth in digital engagement over the past year.

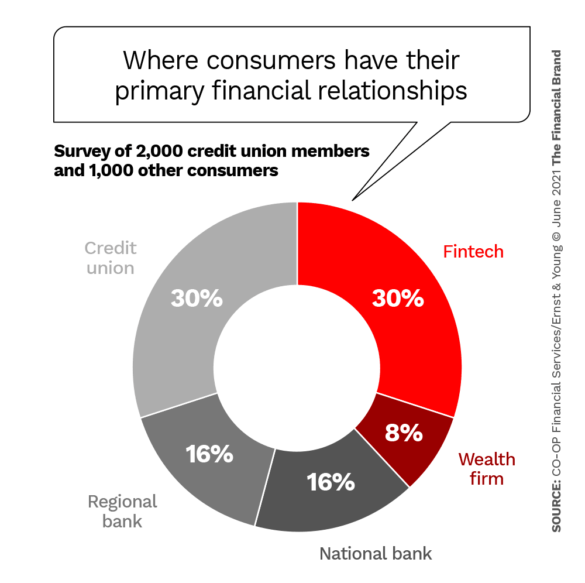

This helps explain why the Ernst & Young found fintechs owning a significant portion of the primary financial provider pie. Even though two-thirds of the sample were credit union members, 30% of all respondents reported having their PFR with a fintech, equal to the 30% who said their PFR was with a credit union. The remainder of the sample was split among national banks (16%), regional banks (16%) and wealth firms (8%).

Day-to-Day Experiences Now Drive Primary Status

To address fintech encroachment on customer relationships, EY recommends community financial institutions develop a holistic approach to the end-user experience by deploying what it calls needs-based segmentation. It’s an elevated way of advising financial institutions to know their consumer. It’s needed because the root cause of PFR has changed. Today, consumers are interacting more often with institutions that provide transactional services, like day-to-day payments, tailored specifically to their needs.

Traditional banking services like deposit accounts, and single-event loan products (i.e., auto loans, personal loans and mortgages) are largely passive and static in nature. By contrast, digitally enabled services — like payments, online services and mobile banking — encourage regular, high-frequency transactional activity. All that activity fosters an engaged relationship between the consumer and the financial institution.

Read More: How Big Do Credit Unions Have to Be to Survive?

To address this shift in PFR drivers, Ernst & Young suggests financial institutions focus less on the life-stage moments of their customers, as has been the customary approach for decades, and instead focus on lifestyle moments. Life-stage moments, like buying a first car or fixing up a house, are no longer enough to sustain a relationship for the long term. Financial products and services focused on lifestyle, or day-to-day banking transactions, however, can move customers from a passive to an active status more quickly and for a longer period.

The Challenge:

Traditional banking is passive and focused on single events. Institutions need to focus on digitally-enabled services often used daily.

Ernst & Young found payments and digital solutions to be two key areas of focus for establishing or strengthening a primary financial relationship. Modern solutions like contactless, P2P and mobile wallets enable credit unions and community banks to be involved in everyday lifestyle moments, not just the occasional life-stage ones.

Some Digital-Native Competitors Outscore Traditionals

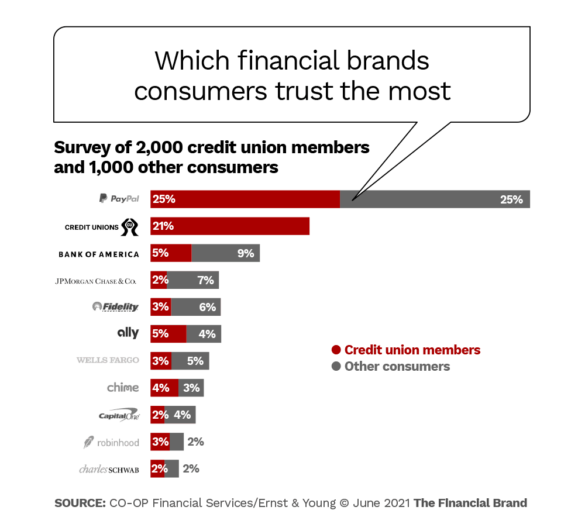

Active, daily engagement builds trust. Because of that, fintechs are pulling away from the mainstream financial services pack in the race to earn the trust of banking consumers.

As the “new normal” takes hold post-pandemic, well-established fintechs like PayPal, as well as direct banks like Ally and neobanks like Chime are picking up market share and are now in the vanguard of the nation’s most trusted financial brands.

In a striking example, Ernst & Young found that PayPal ranked as the most trusted brand for 25% of credit union members. Credit unions landed in second place among their own members at 21%.

Data from Filene Research Institute shows a similar lack of engagement among credit union members —with just 20% saying they consider their credit union to hold their primary financial relationship.

The EY research uncovered that credit union members have significantly fewer lifestyle products with their institution versus with a fintech provider.

Weak Spot:

Credit union members turn to fintechs more often for most types of digital payments than they do to their own credit union.

Among current credit union members, just 34% have contactless payments with their credit union, while 45% have it with a fintech provider. Similarly, 31% of members use P2P payments with their credit union, while 44% use P2P payments from a fintech provider. Just 29% use their credit union’s mobile wallet as compared with 43% that use a fintech’s wallet service.

Read More: The Future of Payments is Fast, Seamless, Safe and Embedded

Losing engagement to fintechs is about much more than a loss of business. Credit unions and other community financial institutions have a strategic imperative to guide consumers to long-term financial wellness. Fintechs and other digital brands are detracting from that mission by providing the popular, in-demand transactional experiences modern consumers clamor for. Not only does this set up purpose-driven, human-centric financial institutions for loss of business, it may even set up consumers for the development of harmful financial habits.

A 3-Part Approach to Competing with Digital Brands

Though the above facts are stark, community financial institutions are far from out of the race. They have strong advantages, including a reputation for outstanding personal service, trusted advice and data security. Ernst & Young recommends community institutions leverage these advantages while launching new PFR-earning experiences via a three-pronged approach. Payments consistently rises to the top as a key strategy to advance each of the three approaches.

1. Lifestyle enablement

EY proposes a multi-dimensional strategy that considers both demographic segmentation (i.e., gender, age, wealth tier, marital status, geography) coupled with needs-based segmentation that incorporates life events, lifestyles and a mix of solutions that address both.

By adjusting product mixes to offer desirable lifestyle banking features — such as seamless digital payments — community institutions can retain, capture and recapture PFR across a broad swath of current and prospective customers.

As an example, by offering a high-valued digital banking feature like free real-time cash back rewards, or by offering both a high-valued feature and a standard feature for free, EY expects community banks and credit unions can grow relationships with existing customers by as much as 24%. What’s more, they can grow PFR with customers who consider a fintech their primary provider by as much as 28%.

2. Pathway to relationship primacy

As discussed above, consumers have bifurcated their PFR between a primary deposit/savings institution and a primary transactional interface. Whereas community financial institutions are in a strong position in deposit/savings (ranked #1 for loans, savings and checking in the survey), fintechs have achieved the top slot in transactional relationships.

Payments products like contactless, P2P and mobile wallets are at the heart of these transactional relationships, driving multiple engagements every day. In fact, payments represent 80% of a consumer’s interaction with their financial institution.

What’s Needed:

Community financial institutions will have to accelerate investment in digital capabilities, while being intentional about bridging the gap between digital and non-digital channels.

3. Digital ecosystem acceleration

Users of a fintech’s payment products stay in the firm’s ecosystem, engage with the provider’s other products and services and actively use social media to share their stories and experiences.

Banking customers should not have to leave traditional financial institutions to meet their financial needs. To avoid that, community institutions must move closer to becoming the hub of their customers’ entire financial lives. The goal: to offer a seamless, hyper-personalized experience in being able to access payments, mortgage and loan applications, wealth advisory services, insurance and personal financial management from one trusted source.

The Need to Partner Is Imperative

Through needs-based segmentation, community financial institutions can attack niche markets by introducing new, convenient features that wrap around existing products and services. This will enable credit unions and banks to compete with the largest, most trusted digital brands inside and outside of financial services. However, given the fact that community financial institutions often have limited resources and budgets, they may not be able to achieve the level of transformation needed — or do it quickly enough — on their own.

The key lies in a new partnership model, which may include collaborating with different solutions providers to offer a range of services based on the specific life stage and lifestyle needs of particular segments. Banks and credit unions also need to be confident and comfortable in a fintech’s understanding of the institution’s culture, philosophy and commitment to human-centric service.

But financial institutions should not let the complexity of partnering with fintechs slow them down, EY contends. They need to start now. If the industry gets better at meeting the consumers where they are, by deeply understanding them and delivering digital payment solutions that are baked into their daily lives, consumers will use more of the financial institutions’ services. In turn, the financial institutions will be better able to help consumers achieve their financial goals.

Becoming a Compelling Alternative to Digital-Native Brands

To re-attain PFR status with existing customers, as well as attract new relationships, community financial institutions must do three things: Mix financial wellness and payments strategies, 2. leverage their in-person service supremacy, building on the personal touch, and 3. offer superior digital services, especially in those day-to-day financial transaction areas. The result of this strategy will be to capture more active, engaged relationships, placing community financial institutions squarely at the center of their customers’ daily financial lives.

As a meaningful bonus, the strategy will draw more people closer to providers who know what it takes to achieve financial wellness and have a strategic imperative to deliver it to their customers.