Imagine a sub-prime consumer who wants to pay off their credit card bills, because their interest rates hover somewhere between 15% and 21%. They want to take out a personal loan with better repayment plans to pay off their existing debt.

Are people more likely to go to a bank or credit union, when they’re researching their options, or are they going to be more intrigued by the fintech offering loans entirely online?

The latter looks like a nicer option. And it’s what’s been happening. Fintechs have been snatching up market shares left and right from traditional banks and credit unions. Fintechs claimed 49.4% of the unsecured personal loan market in March 2019, up from 22.4% four years before, according to Experian.

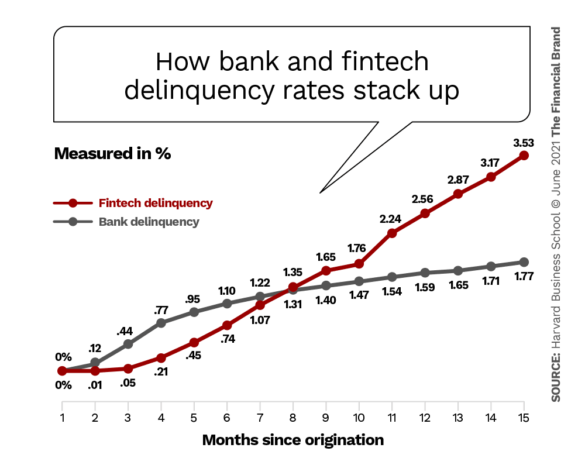

The level of delinquencies, however, is much higher on these non-traditional loans, with fintechs reporting a 3.53% delinquency rate 15 months after loans are originated, almost double the traditional provider rate of 1.77%, according to a recent study by two business school professors.

The study — “Fintech Borrowers: Lax-Screening or Cream-Skimming” — conducted by Marco Di Maggio from the Harvard Business School and Vincent Yao from Georgia State University, was first published in 2018and updated in late 2020. What they found isn’t a pretty sight for fintech lenders.

For one, the co-authors found borrowers with high interest rates on their fintech loans are nearly 40% more likely to be delinquent and their credit scores decline more than a bank or credit union loan — an average decrease of 12 points instead of 0.9 points — and their total debt increases by over $8,000 after a single year.

According to Di Maggio and Yao, fintechs could be pursuing target audiences with subprime credit scores and poor credit histories because they recognize these consumers cannot get comparable loans from a traditional banking provider. However, there is not yet enough data to support the theory these nonbank lenders are actively marketing to subprime consumers.

This is not exclusively a U.S. problem. Leading fintechs in India reported doubling delinquency rates between August 2019 and 2020, according to a TransUnion CIBIL report.

“The delinquency picture is complicated and will take time to emerge due to the lagged effect of financial conditions, relief programs supported by lenders, and shifts in the payment priorities” of Indian consumers, the TransUnion report adds.

Di Maggio and Yao sourced their data from a credit bureau who supplied them with information on unsecured personal loans — a fintech favorite. The two looked into a sample of the more than 200 million consumer credit files and evaluated borrowers’ by gender, age, marital and college graduate status, in addition to whether consumers were borrowing from a traditional provider or a fintech.

Di Maggio says he cannot disclose what credit bureau he worked with to pull data on fintech default rates. The data — given to Di Maggio as anonymous consumers — allowed the authors to match people with different kinds of loans and determine which loans were originated by what type of lender.

Read More:

- Traditional Lenders Losing More Ground As Fintech Loan Share Surges

- How Banks & Credit Unions Can Regain Ground Lost to Fintech Lenders

- Notably Quotable: Fintech Friends or Banking Foes?

The Data That Made Waves

To dig deeper into the paper, The Financial Brand spoke to Di Maggio who says he decided to pursue the topic when he realized a profound absence of information around fintech default rates.

“I researched the academic literature, looked at it [and found] it was sort of a tough question to address,” he explains, adding it’s not common or easy to find the data to support what he and his co-author hypothesized. It’s still a fairly new conversation and the data is not yet plentiful, even though fintech loans are exponentially nabbing space in the lending market.

The bulk of what Di Maggio focuses on is personal fintech loans, which is primarily used for the consolidation of existing debt. He considers it the “riskiest segment” because, even though borrowers may use portions of the personal loans to pay off their outstanding bills, not all of the funds are always going toward the intended purpose.

The Vicious Cycle:

People are only using a part of the debt consolidation loan they took out to pay off their debts. Instead they’re using significant parts of the loan to make new purchases.

And the problem has grown drastically, he says, because people with card debt often keep the cards after paying them off and then run up the balance again.

“The worst outcome is happening because if $40,000 was not sustainable before, now you end up six months down the line with $80,000,” Di Maggio says. “Also, borrowers’ outcomes worsen in the months following the fintech loan origination compared to similar individuals borrowing from non-fintech lenders.” It’s a classic weak point of debt consolidation loans. Fintechs just made the process much easier.

Di Maggio’s findings are still making waves in the financial industry. When he first presented his research at a conference with a fintech audiences, people were angry.

“We had people from LendingClub, people from TransUnion very upset,” he says, joking that he challenged them to find data to prove him wrong. Two years later, he says they have yet to come to him with alternate data.

It’s Not All Sunshine and Roses

Fintech lending has its advantages, of course, which could be why so many consumers are shifting away from the conventional providers. People can more easily get loans if they have subprime credit scores and the fintech lenders will look at other forms of personal data to supply credit worthiness requirements.

There’s also much less oversight. While banking regulators threaten to write-up banks and credit unions with compliance violations, fintechs have no federal supervision, although the Consumer Financial Protection Bureau does have oversight of some practices.

“Some observers argue that fintech lenders might be able to operate where the banks do not find it profitable,” Di Maggio and his co-author wrote in the paper, noting fintech lenders also have lower fixed costs than those of traditional lenders, because the nonbanks have no branches.

And these advantages don’t escape the attention of traditional banking providers. Banks and credit unions, even if they don’t want to admit it publicly, are growing more concerned with the growing swarm of competitors.

They Might Be Gaining On You:

Almost nine out of ten financial institutions are also worried that fintech lending will overtake their own lending, according to PWC.

It may be a relief then to existing providers to know they may not have as much to worry about as they think. According to Di Maggio and Yao, fintech lending may not be all it’s cracked up to be and traditional banking providers still have an edge over the challengers. They have a better track record with attracting consumers who are able to pay back their debt. And the regulations once assumed to hinder traditional banking providers may be what saves them.

“I think lending and the digital banks are less of a threat than, for instance, what’s happening to the payment system,” Di Maggio maintains, citing Stripe and similar digital payment specialist, which he thinks pose significantly higher risk to banks than LendingClub.